Bloom's Big Lie

Hidden China Supply Chain, Dubious Deals, and Aggressive Accounting Threaten a $70 Billion AI Growth Story.

Based on Hunterbrook Media’s reporting, at the time of publication Hunterbrook Capital is short $BE including derivatives and long a basket of comparable securities, as well as long $NB including derivatives and short a basket of comparable securities. Positions will change. This article is not investment advice or a recommendation to buy, sell, or hold any security. See full disclosures on our website.

By: Till Daldrup, Dhruv Patel, Jean Wang, Blake Spendley, Sam Koppelman

Editor: Vikas Kumar

Bloom Energy is one of the AI boom’s biggest winners. $BE is up about 2,000% in two years. Its valuation peaked around $100 billion. The vision: fuel cells powering AI data centers years faster than the electric grid, with Bloom saying it can scale from about a gigawatt of deployments in 2026 to 5 gigawatts annually. It’s a compelling pitch, especially in a world where power from legacy players, including turbine manufacturers, is backlogged.

That growth story rests on a supply chain claim that Bloom’s CEO has made at least five times since February 2025, on earnings calls, to Semafor, on a podcast — and onstage with The Wall Street Journal last month. The promise: Bloom has “no China supply chain” and is “not dependent on China for scandium,” the rare earth at the core of each Bloom fuel cell. Bloom’s claim matters because Beijing now requires an export license for every shipment of scandium leaving China. If Bloom depends on Chinese scandium, China holds an off-switch on Bloom — and on the American data centers that may one day use its power.

The problem: Bloom is, in fact, reliant on C5 Chinese scandium, according to global trade data, Chinese corporate filings, satellite imagery, and Hunterbrook’s messages with Bloom’s suppliers in China. Hunterbrook traced four separate China-linked routes into Bloom’s supply chain — scandium oxide shipped directly to its Delaware plant, plus scandium-bearing ceramics and powders flowing through intermediaries in Thailand, Japan, and South Korea. A sales representative of Hunan Oriental Scandium — which claims over 50% of the global market for fuel-cell-grade scandium oxide — told Hunterbrook: “We are also BE’s largest supplier of scandium.” Asked how the material reaches U.S. customers under Beijing’s controls: “Not exported directly.” Hunan Oriental was featured at Bloom’s May supplier conference as one of three Chinese scandium-linked suppliers. One received Bloom’s “Impact Supplier Award.”

Show Me the Scandium: Even with supply from China, the scandium math fails. Hunterbrook’s supply-demand model — built from government filings, Bloom’s patents, industry data, and peer-reviewed studies — shows Bloom alone needs roughly 220 tons of scandium oxide to meet Wall Street’s 5 GW expectations. But that’s against total projected global supply of only about 240 tons versus total global demand of about 310 tons, including supply locked up by customers like Lockheed Martin (for the F-35 fighter jet). Bloom already claims to be the largest scandium consumer in the world. On the numbers, the production ramp underpinning Bloom’s valuation appears physically and commercially unattainable — with essentially all Wall Street models of Bloom’s production implying a scandium shortage by 2028 based on Hunterbrook’s model.

The demand side of the story is also not what it appears. In 4Q25, 74% of Bloom’s revenue — $574 million of $778 million — came from joint ventures Bloom part-owns with Brookfield. Bloom’s own footnotes concede these customers “may be a project-finance affiliate rather than the ultimate end user.” What Bloom’s recent revenue growth shows is that Brookfield will finance Bloom’s production, not that a meaningful customer base has adopted Bloom’s fuel cells. And it appears Bloom has been recognizing revenue well before its fuel cells have actually been deployed.

The Brookfield partnership’s initial promise, a European AI factory site to be named “before the end of the year,” does not seem to have been fulfilled. The designated anchor tenant for its unbuilt AI project is Radiant, Brookfield’s own captive cloud company, which has no publicly named CEO or disclosed customers. The Brookfield fund backing Radiant is anchored in part by Nvidia, whose chips the factories will house. Even by the standards of AI roundtripping — which can be positive sum — the deal looks especially circular.

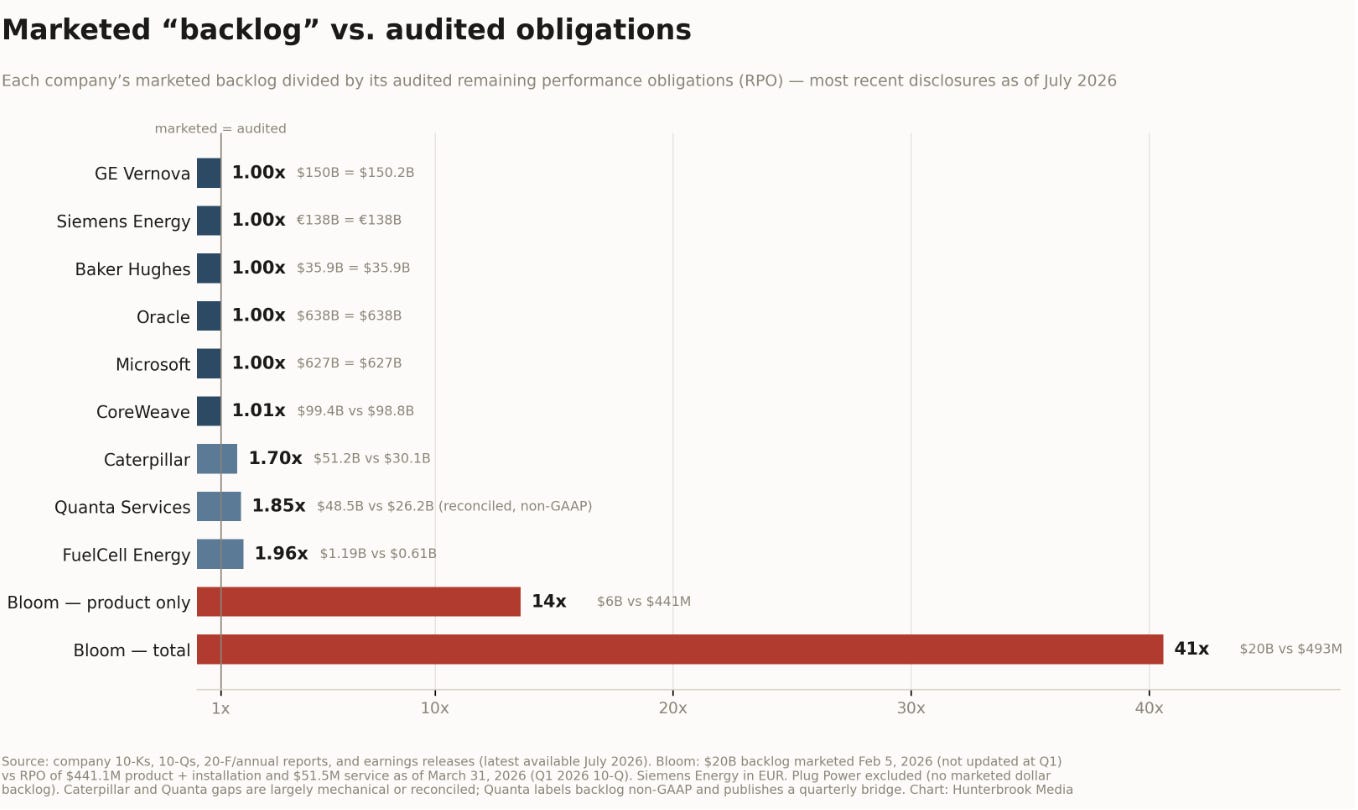

Bloom markets an unaudited $20 billion “backlog” of orders. Its remaining performance obligations (RPO) — the analog to backlog that its auditor reviews — total $492.6 million as of March 31. That’s roughly 2.5% of the backlog. Among 10 peers Hunterbrook analyzed, including GE Vernova, Oracle, Microsoft, and CoreWeave, the widest comparable gap between backlog and RPO was about 2x. Bloom’s is over 40x, in part because it includes ongoing servicing revenue customers are not obligated to pay and tax credits the government has not agreed to grant.

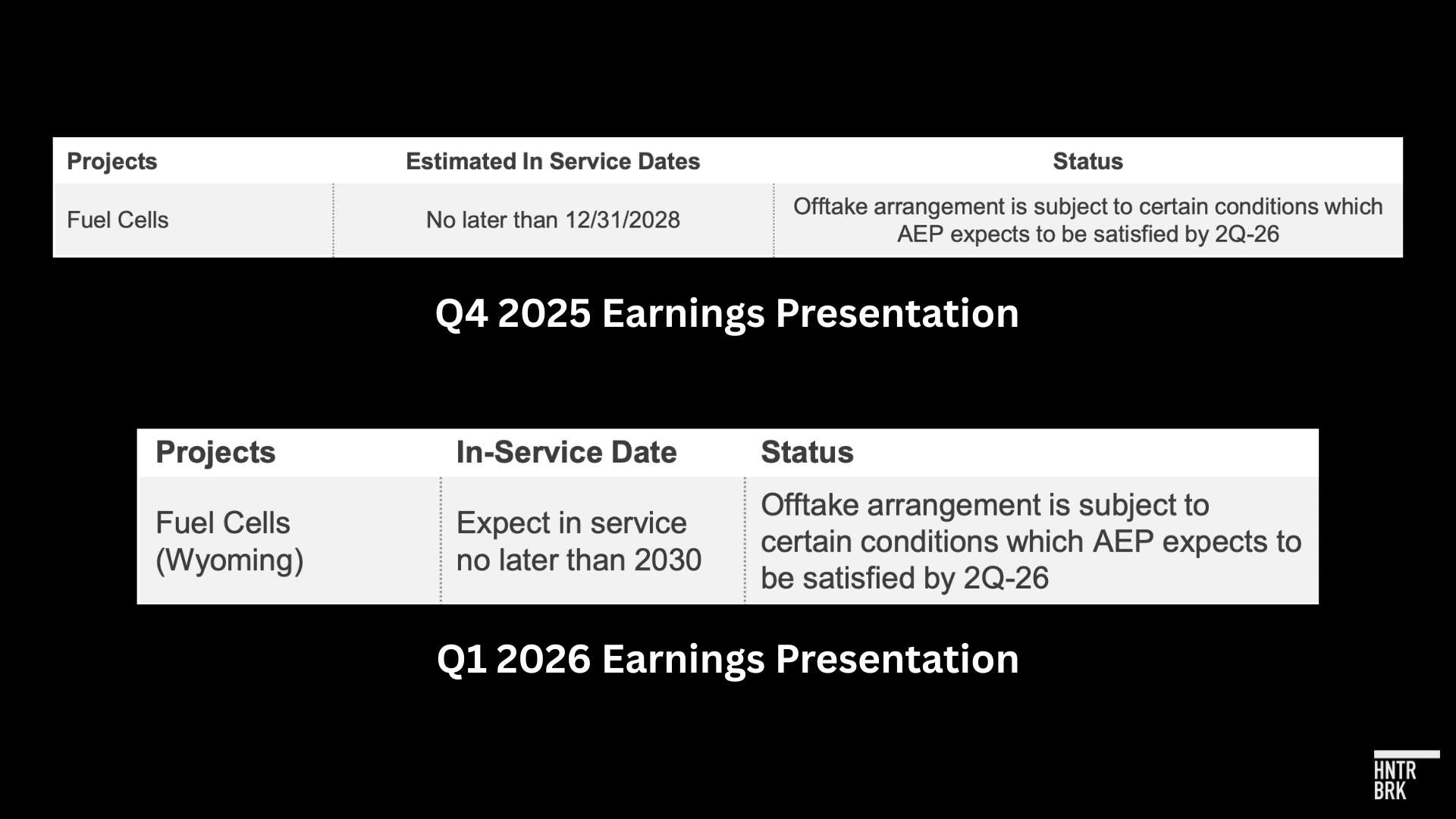

The two flagship projects presumably driving that backlog are both facing serious challenges to their viability. Oracle’s Project Jupiter in New Mexico has no approved air permit for fuel cells and no gas pipeline to feed the fuel cells, leading research firm SemiAnalysis to push back its base case for first power from 2027 to 2029. Hunterbrook interviews with New Mexico officials and an environmental group suing to stop the Oracle project indicate it could be delayed into the 2030s, or even canceled outright like Blackstone’s data center in Virginia last week. Meanwhile, AEP’s $2.65 billion fuel cell order also appears to have slipped, with the utility updating its investor deck from a target deployment by the end of 2028 to one “no later than 2030.” That deal, which represents a meaningful share of Bloom’s backlog — related to a campus that reportedly lost its developer Crusoe in June — is backstopped by an unnamed hyperscaler that can walk away by covering AEP’s costs incurred, plus roughly 10%. Both new Oracle and AEP delays followed Bloom raising guidance in its last earnings call.

Put together: Either the 5 GW ramp is real — and the scandium math breaks it, plus Beijing holds the off-switch — or it is not, and the record quarters are largely circular financing.

Bloom can’t easily engineer its way out. Its own patents identify too little scandium in the electrolyte as a cause of accelerated fuel-cell aging. Cutting scandium seems to reduce the stack life on which Bloom’s 10-to-15-year service contracts depend. Nor can ex-China supply fill the gap: “Right now in the Western world, there’s basically no scandium processing capability to speak of, or just very, very little,” John Mavrogenes, a professor of economic geology at the Australian National University, told Hunterbrook. “It would be a long road to say we’re gonna get serious about scandia.”

Bloom has repeated this pattern for years: When end demand doesn’t materialize, it finds an intermediary willing to bet on Bloom — then books that bet as growth. Delaware ratepayers were legally obligated to buy Bloom’s power for two decades, at costs that eventually ran over five times what the public was originally told, for jobs that came up 600 short of Bloom’s projections. SK ecoplant committed to volumes that propped up two years of results, then quietly got three extra years to comply when Korean demand stalled. The month after SK ecoplant began selling its Bloom stake, Bloom formed its joint ventures with Brookfield, which is now the counterparty buying Bloom’s boxes. Each time, the financier’s commitment — not a customer’s consumption — makes the numbers.

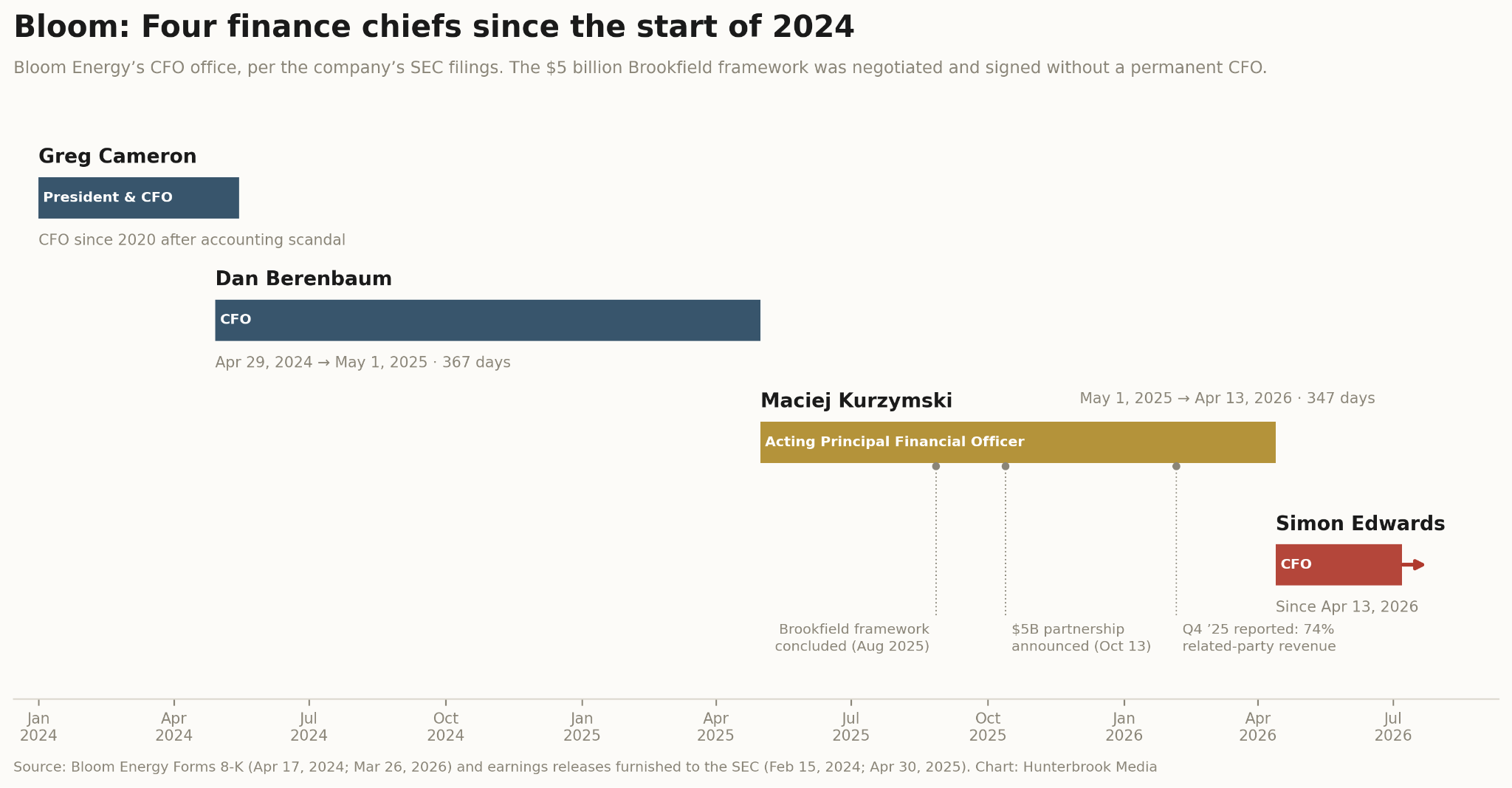

The people in charge of reporting those numbers keep changing. Bloom has had four finance chiefs since the start of 2024, including nearly a year with no permanent CFO, which happened to be the same year the Brookfield structure was built. The CEO, meanwhile, has never changed.

Neither Bloom nor its CEO replied to Hunterbrook’s repeated requests for comment, which laid out our findings in detail. Oracle replied to initial outreach, then did not respond when asked if it knew Bloom sources from China. Brookfield did not respond to repeated outreach from Hunterbrook. AEP directed Hunterbrook to links of statements it had already made.

While Bloom did not respond to our requests, it certainly seems like someone at the company read our questions. The day before publication, Bloom published a blog post about scandium, written by its COO. The post confirmed several of Hunterbrook’s findings, including that scandium oxide plays “an important role” in the functioning of its fuel cells, and that Bloom believes itself to be the world’s biggest consumer of the rare earth. Bloom also included vague responses to some of our other findings. Rather than echo Sridhar’s unequivocal statements about China, the blog post asserts that no “single country” can determine Bloom’s “destiny.” It explains that Bloom sources scandium from the by-products of other mining operations — as Hunterbrook’s reporting already noted — giving titanium as an example. Bloom emphasized that more than half of titanium mining (though not necessarily half of scandium production) occurs “outside of China.” The post further claims Bloom believes its supply chain “can support up to 25 GW per year,” but did not share any details on the calculations or assumptions that lead the company to that belief; nor did Bloom specify the timeline of when that supply would become available. Per our calculations, which are based on the scandium levels listed in Bloom’s own patents, 25 GW of power would require roughly 620 tons of scandium a year: about ten times what the entire world consumed in 2025, per USGS figures. Bloom cautions readers: “This article was published on July 7, 2026, and is for informational and educational purposes only. Readers are encouraged to read Bloom’s full disclosures, including information on potential risks and uncertainties that may impact Bloom’s business, set forth in its periodic reports filed with the SEC.” As far as we can tell, no other post on the company’s blog includes this disclaimer. As of press time, Bloom has not issued a press release or 8-K denying any of the facts presented in this article.

“We are not dependent on China for scandium,” Bloom Energy ($BE) CEO KR Sridhar pledged in an April 2025 earnings call. “I can state that very clearly.”

“We do import materials and components from abroad, but not from China,” he said.

Analysts pressed him three times on Bloom’s supply chain. He left no room for ambiguity.

“What you need to understand is none of our critical materials come from contested supply chains or war zones, and there is no China supply chain for us.”

Sridhar made the same guarantee in Bloom’s February 2025 call: “We are not dependent on China for our supply chain, and that is super important.”

That April, China added scandium to a list of materials requiring national security export licenses. That means the material can only leave China with Beijing’s discretion on a case-by-case basis.

Among many exotic uses, scandium is essential to America’s F-35 fighter jets, making access to the metal a national security issue for both the U.S. and China.

But the biggest buyer of scandium isn’t any government. It’s Bloom, which, according to Sridhar, has become the single largest consumer of the metal in the world, because scandium is a critical component of its fuel cells.

Specifically, scandium is the key material in the electrolyte of Bloom’s fuel cells (“Bloom Boxes”). It allows electricity to be produced and lengthens the fuel cell’s lifespan. There is no known commercially viable substitute for scandium in Bloom’s fuel cell design that wouldn’t degrade quality, according to the company’s patents and fuel cell experts that Hunterbrook interviewed.

The problem: China produces most of the world’s scandium, by one estimate as much as 90%.

That is why the company has been asked, repeatedly, about how it procures the metal. And it is likely why Bloom has been so insistent that it is not reliant on China.

In a September 2025 interview with Semafor, Sridhar went as far as to say that Bloom had decided more than 20 years ago that it would not rely on Chinese suppliers. “Starting in 2004, we said we are not going to depend on a Chinese supply chain. If we believe in energy abundance for all, there cannot be a single source to strangle you,” he said.

Then he told an energy podcast: “We never coupled ourselves to the China supply chain, which in hindsight means today we don’t have to decouple from something.” Sridhar specifically said this was a big part of Bloom’s edge over gas turbine producers, whose supply chains he described as rooted “in the same place.”

Last month, Sridhar stated yet again that Bloom is not sourcing from China in a June 10 interview onstage with The Wall Street Journal.

”Very early on in the company we made a decision that we are only going to depend on supply chains that we can completely trust and that was a country we avoided,” he said, responding to a WSJ question on China. He gave 2005 as the year the company made this decision. Then he teased a possible deal with the U.S. Department of Defense based on Bloom’s independence from Chinese supply.

But Bloom does rely on Chinese scandium — and it did at the time of each of these claims, according to Hunterbrook’s analysis based on trade data, satellite images, and conversations with major suppliers and experts.

In total, we found four separate trade routes that appear to show Chinese scandium is still part of Bloom’s supply chain, and the material is reaching the U.S. through intermediary countries.

As recently as May 2026, Bloom even featured three Chinese scandium suppliers — one of them with the word “scandium” in its name — on a logo wall at its supplier conference.

After the April 2025 earnings call, Bloom made a subtle update to its quarterly filing for 3Q25, adding that China supplies “multiple components including 70% of rare earth metals used in electronic and electromechanical components that are part of our tier 2 and tier 3 sub-assembly suppliers.” Its 10-K report, filed in February, then used substantially similar language on pages 47 and 56, but dropped the 70% figure, and added language stating that “continued escalation of trade tensions between China and the U.S. could impact our ability to source these rare earth metals and components.”

Yet the company maintained in both filings: “Our supply chain is not dependent on China.”

And months after the annual filing, Sridhar went onstage with The Wall Street Journal in June 2026 — where he reiterated, unambiguously, that the company does not source from China.

“I don’t know of anywhere else they would get it from that’s of the scale that they would need,” Eric Wachsman, director of the Maryland Energy Innovation Institute, told Hunterbrook about Bloom’s scandium needs. “You have to be able to purify it, and that purification process tends to be primarily in China.”

One way Bloom appears to be obfuscating its reliance on China is by rerouting shipments through intermediary countries. This may look better in the trade data, and provide some support for Sridhar’s claim that Bloom sources from “multiple countries” across “multiple continents,” but it doesn’t change the fact that a large chunk of the scandium is still from China: a single point of failure supply chain risk.

And China can cut off that scandium supply regardless of how indirectly it flows to Bloom.

In fact, multiple Chinese scandium suppliers told Hunterbrook that China’s Ministry of Commerce requires end users of scandium — not just exporters — to provide information to the government regarding its planned use for the material. If the Chinese Communist Party does not approve, it can block the exports.

Bloom’s reliance on this supply chain means China may have an off-switch on America’s data center build-out — at least, data centers dependent on Bloom.

After about two decades of losses since its 2001 founding, Bloom recently became a darling of the AI stock boom because fuel cells might provide data centers with behind-the-meter power. Fuel cell financials had been uneconomical, but new grid connections are now taking years, so data centers are willing to pay the premium for quicker time to power. The numbers work even better with the cells now consuming cheap methane instead of more expensive green hydrogen. (Whether Bloom’s original approach was green in the first place is an open question that led to an EPA fine against Bloom and featured in Hindenburg Research’s investigation.)

Bloom’s keystone data center deal is an agreement with Oracle ($ORCL) to provide up to 2.8 GW of power for data centers. According to Hunterbrook’s model, there may not be enough scandium on the entire global market to meet the production required for that deal, let alone the rest of Bloom’s backlog — which includes a deal with the Nebius Group ($NBIS), a neocloud backed by Nvidia ($NVDA).

$BE stock nearly quadrupled in 2025 after the news broke of the Oracle partnership — and more than doubled again in the first half of 2026. In total, its share price is up more than 2,000% within two years, with Bloom’s market cap peaking around $100 billion in June, rivaling energy giants like Constellation ($CEG) and Vistra ($VST), on the thesis Bloom can rapidly scale up.

$BE also appeared to be a big winner for Leopold Aschenbrenner’s fund Situational Awareness, though the fund sold over a third of its disclosed $BE position in its most recently reported quarter, even as its assets under management soared.

But can Bloom actually deliver enough fuel cells?

The answer to that question may explain the reason for the company’s repeated insistence on its independence from China.

On its scandium sources, Bloom has told investors: “We don’t reveal those sources and methods. That’s part of our IP.”

But Hunterbrook reconstructed the global scandium supply chain — identifying the few active projects and evaluating potential future sources. The newsroom also reviewed patents, market data, and academic and industry research to estimate Bloom’s consumption.

The conclusion was clear: Bloom lacks enough scandium for its lofty ambitions and timeline.

The model’s math aims to be conservative. Rather than counting only current production, it gives partial credit to meaningful planned production, including generous assumptions about the likelihood and speed with which pre-commercial projects can ramp up. It also assumes the existing growth rate of scandium consumption by other customers will hold steady, despite wider adoption across aerospace, military, and automotive industries. The model also considers the case in which Bloom has engaged in significant “thrifting” (essentially recycling scandium from used fuel cells) and innovating to consume less scandium, though it does not assume needle-moving stockpiling for reasons described below.

Bloom did not respond to repeated requests for comment about its scandium supply. Instead, the day before publication, its COO posted a blog asserting Bloom’s supply chain “can support up to 25 GW per year,” without providing evidence. Bloom said it “maintains strict confidentiality around its sourcing network” — supplier relationships and sourcing volumes are “proprietary” — “to protect the resilience of our supply chain.”

Bloom then cautions readers to read its “full disclosures, including information on potential risks and uncertainties that may impact Bloom’s business, set forth in its periodic reports filed with the SEC.”

Hunterbrook’s data demonstrates that without Chinese scandium, even if every new non-Chinese project meets current timelines, adjusted for the risk it slips, in 2030 there would only be about 60 tons of scandium oxide that’s not already contracted by other customers like Lockheed Martin.

Bloom needs about 220 tons to power 5 GW and fulfill unit replacements. Even with Chinese supply, the data indicates there will not be enough available scandium to meet Wall Street’s expectations for Bloom.

If Bloom can’t deliver enough fuel cells, it wouldn’t be the first time the company’s claims didn’t match reality. In the 16 years since Sridhar debuted Bloom to a national audience on 60 Minutes, its statements about cost, hazardous waste, ratepayer fees, and fuel cell life have been contradicted by the record, including state filings, federal enforcement findings, and Bloom’s own SEC disclosures.

Each time, the better number came first and the correction came later, in a clawback, a penalty, or a restatement.

This time, it’s not just the scandium supply numbers that don’t add up. It’s also the demand for Bloom’s products.

Bloom’s recent string of record-setting quarters rests on fuel cells sold to financing vehicles the company itself part-owns with the financier Brookfield, but the orders don’t appear to be turning into operating data centers.

And since Bloom’s last guidance update, two flagship destinations have recently slipped by years.

Project Jupiter in New Mexico has no approved air permit and a gas pipeline stuck at FERC. In May, the industry publication SemiAnalysis estimated first power at the site in 2029. Meanwhile, Bloom’s fuel cell deal with the utility AEP — apparently tied to a hyperscaler plant outside Cheyenne, Wyoming — slid from “no later than year-end 2028” to “no later than 2030,” according to AEP investor slide decks.

The roughly $20 billion backlog Bloom markets to investors is more than 40 times the $492.6 million in binding contractual obligations disclosed in its most recent quarterly filing. Across peers Hunterbrook analyzed, from turbine makers to hyperscalers, the widest comparable gap was about two times. This, at a company that has run through four finance chiefs since the start of 2024 — and five since 2020.

The scandium shortage and the demand gap converge on a single debate: whether the 5 GW ramp key to Bloom’s valuation is real, or whether it’s just the latest Bloom story that turns out to be too good to be true.

INSIDE THE CHINA SUPPLY CHAIN BLOOM SAID IT DIDN’T HAVE

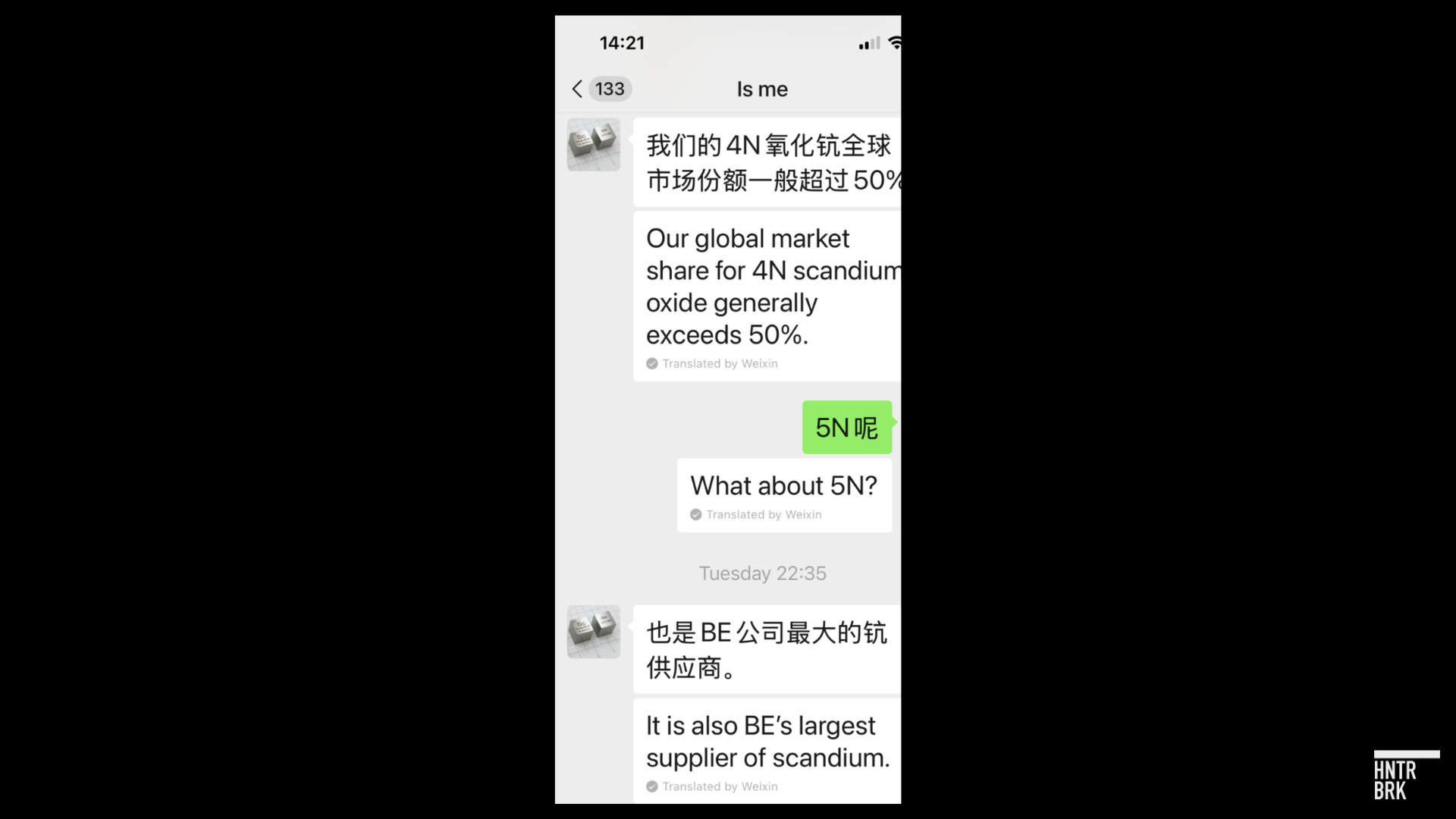

Hunan Oriental Scandium is a major scandium producer in China. When a Hunterbrook reporter reached out about shipments to the U.S., a representative listed the company’s credentials.

“Our global market share for 4N scandium oxide generally exceeds 50%,” they wrote, adding: “We are also BE’s largest supplier of scandium.” BE is the ticker symbol for Bloom Energy.

A bold claim by the Chinese supplier, as Bloom’s CEO said his company has no China supply chain.

But trade data and company announcements corroborate longstanding ties between Bloom and Hunan Oriental, which is a subsidiary of LB Group, a large Chinese chemicals company.

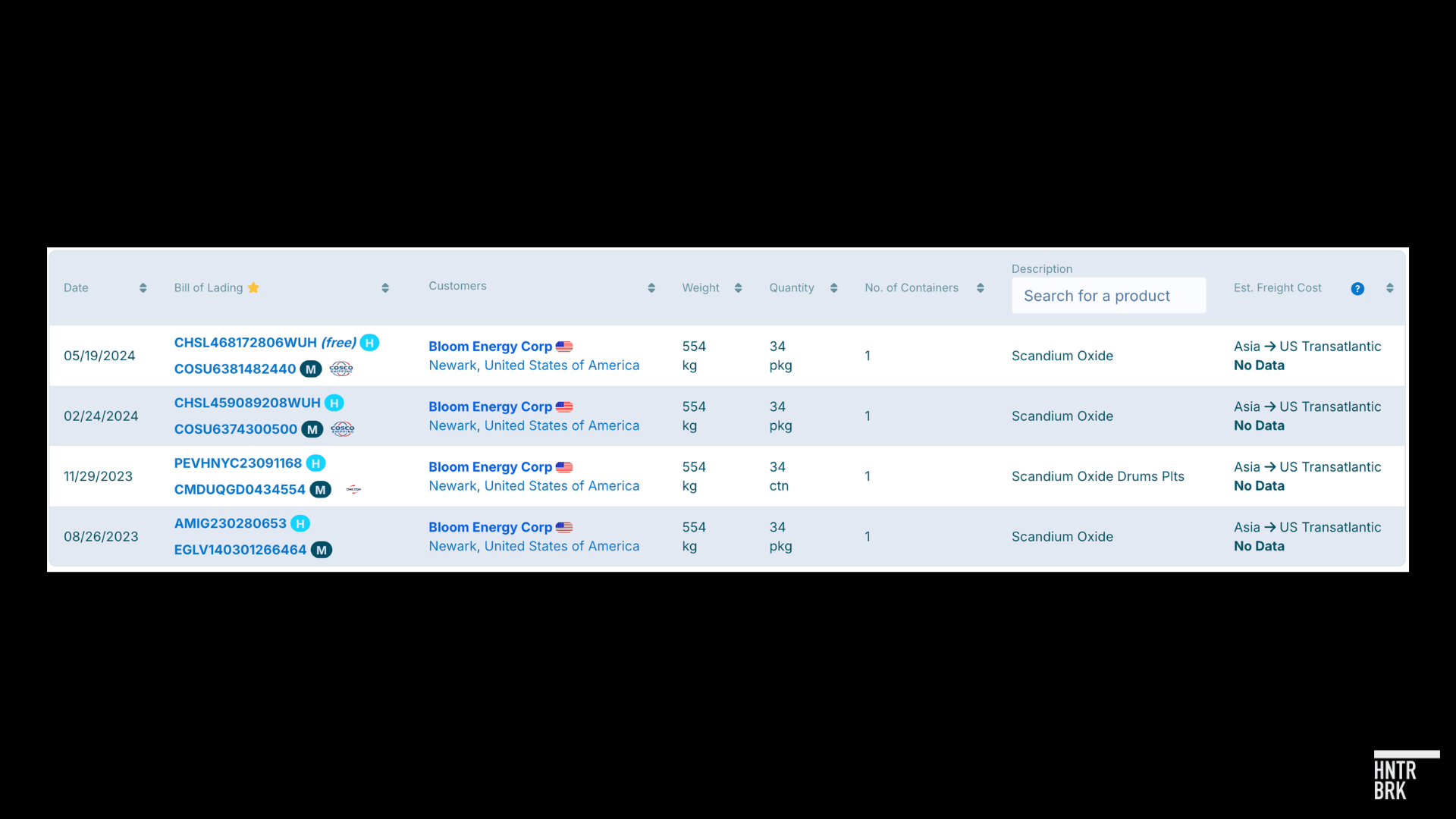

Hunan Oriental shipped scandium oxide directly to Bloom in Newark, Delaware, at least four times between August 2023 and May 2024, according to commercially available trade data. The product descriptions include “scandium oxide” and “scandium oxide drum pits.”

Bloom also visited the same supplier a few months after the first of these shipments.

On November 2 and 3 in 2023, a Bloom delegation from the U.S. visited Henan Rongjia Scandium-Vanadium, a “wholly-owned subsidiary of Hunan Oriental Scandium,” for an “inspection and exchange,” according to a Chinese-language company account. The Bloom delegation included a product manager, chief engineer, senior staff engineer, supply-chain procurement manager, and quality manager.

The delegation toured LB Group’s “exhibition hall, corporate technology center, and Rongjia’s scandium oxide production workshop,” the company said in a press release.

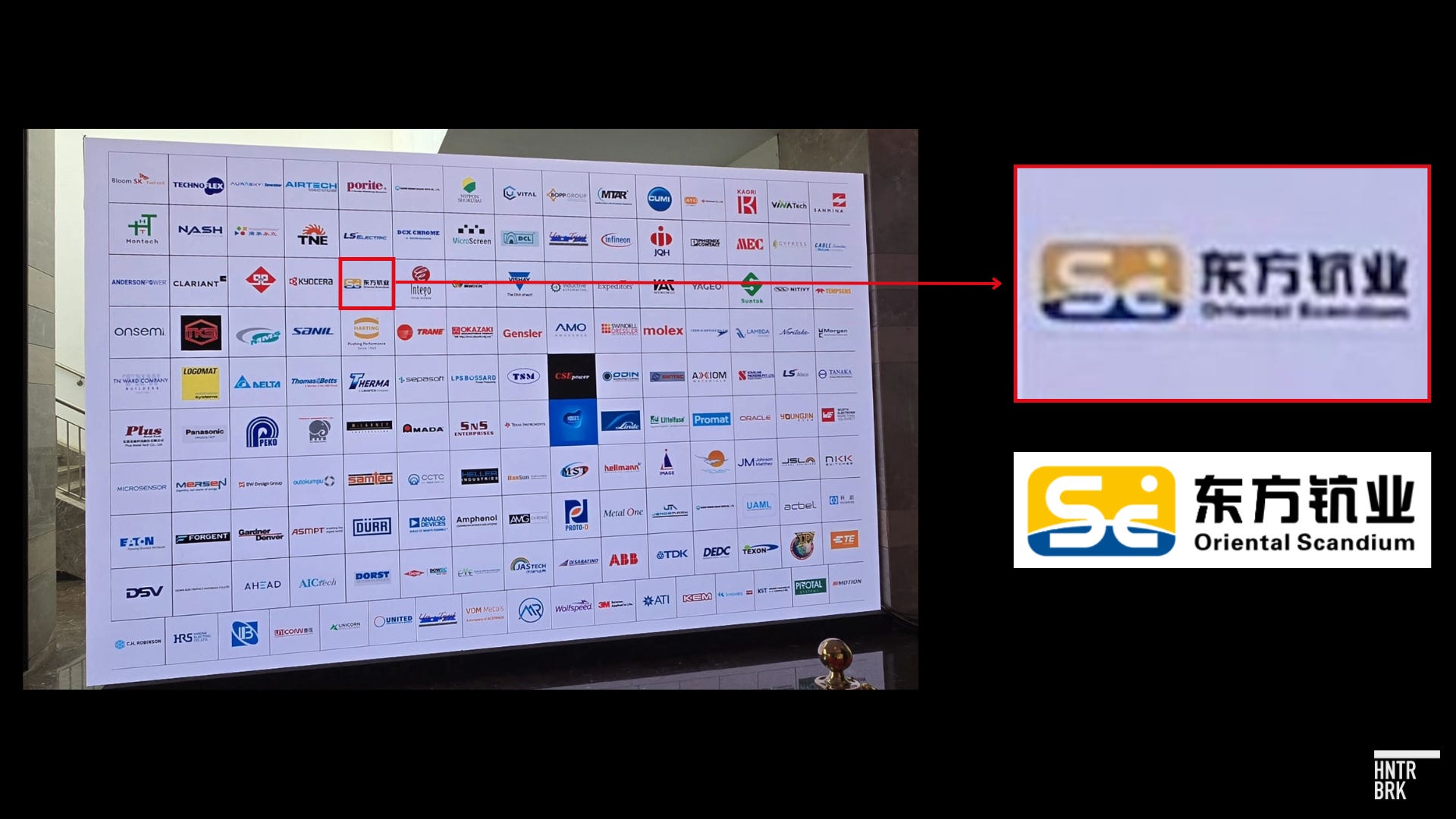

A photo taken at Bloom’s 2026 supplier conference in May and posted to LinkedIn appears to confirm the relationship between the two companies has continued: It shows Hunan Oriental Scandium’s logo.

But while Hunan Oriental claims to be one of Bloom’s top suppliers, no further shipments to the fuel cell manufacturer appeared in that trade data, after the scandium deliveries in 2023 and 2024.

So how does the material reach Bloom now, especially given the tighter Chinese export controls on rare earths that took effect in 2025?

When the Hunterbrook reporter asked the Hunan Oriental sales rep how the company is sending its scandium to U.S. customers, the response was blunt.

“Not exported directly,” they wrote.

THE PLAYBOOK — AND THE MONEY RUNNING IT

A Chinese securities filing gives insight into Bloom’s supply chain playbook and how one of its partners has apparently obfuscated Bloom’s reliance on Chinese products.

Zhejiang Chunhui Intelligent Control, a Chinese manufacturer, has supplied Bloom with the temperature sensors that monitor its fuel cell stacks since 2007. In a November 2025 disclosure to the Shenzhen Stock Exchange, reviewed and translated from Chinese by Hunterbrook, Chunhui describes itself as Bloom’s dominant sensor supplier, accounting for more than 70% of the American company’s purchases of the part over a roughly two-decade relationship.

The sensors are not scandium. But the filing lays out, in Chunhui’s own words, how Bloom is trying to limit its exposure to Chinese trade. Bloom “has begun changing its supply-chain process” — directing Chunhui to ship its products not to the United States, but to Bloom’s “other overseas suppliers,” who “complete assembly before shipping on to the United States,” in order to “gradually reduce direct exports to the U.S. and thereby mitigate the impact of U.S. tariff policies.”

The Chinese filing even names Bloom’s waypoints.

Starting in 2025, Chunhui began routing its Bloom-bound product through Kaori Heat Treatment in Taiwan and MTAR Technologies in India. Both are Bloom suppliers. The trade data matches: Chunhui’s direct deliveries to the U.S. fall during this period and become sporadic, while the weight of shipments from Kaori and MTAR to Bloom increases significantly.

Chunhui’s direct sales to Bloom dropped from roughly 31% of its revenue to under 13% as the rerouting took hold.

Bloom’s recent 10-K disclosure appears to confirm that the company is using the same playbook with rare earth metals and compounds from China by routing them to the company’s “tier 2 and tier 3 sub-assembly suppliers.”

Hunterbrook looked at Bloom’s shipments over the past two years to uncover the waypoints through which Bloom receives Chinese scandium. We identified three trade routes that appear to obscure the Chinese origin of Bloom’s scandium imports.

ROUTE 1: A MAJOR CHINESE SUPPLIER’S THAI SUBSIDIARY

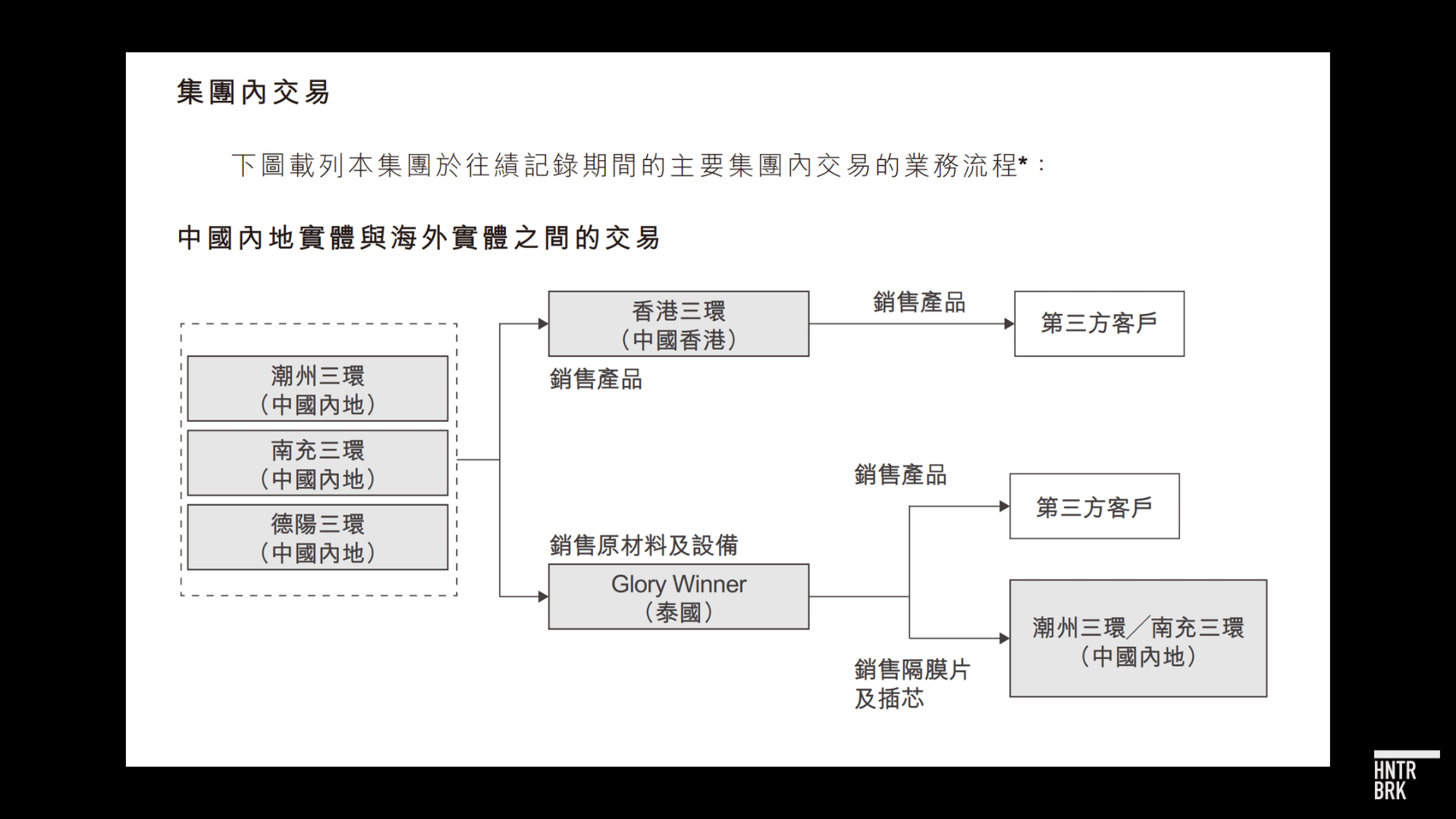

According to the import data we reviewed, Glory Winner (Thailand) Co. Ltd. shipped more than 154 metric tons of ceramic electrolyte membranes to from Thailand to Bloom between July 2024 and November 2025. Glory Winner is a subsidiary of China’s Three Circle Group, which has been identified as a “core supplier” for Bloom in Chinese media.

Scandium is a key component of the ceramic electrolyte membranes in Bloom’s fuel cells, per the company’s own patents and multiple fuel cell experts interviewed by Hunterbrook.

The United States Geological Survey (USGS) does not list Thailand as a scandium producer.

So while Bloom’s scandium-containing parts sourced from Glory Winner may not be shipped directly from China, trade data and Chinese industry coverage indicate that they are in fact of Chinese origin.

A diagram in Three Circle’s 2026 draft IPO prospectus for the Hong Kong Stock Exchange shows that the company’s China-based operation is supplying “raw materials and equipment” to Glory Winner. Elsewhere in the document, Three Circle says “the main raw materials are all sourced domestically,” referring to China.

Three Circle’s 2021 response to a Shenzhen Stock Exchange inquiry letter suggests that this trade route was set up in 2019 and designed to avoid U.S. tariffs.

“To mitigate the impact of the additional tariffs on fuel cell separator plates, the company consulted with relevant customers and implemented the following measures,” the document states. “In July 2019, it established a new subsidiary, Glory Winner (Thailand) Co., Ltd., and relocated the fuel cell separator plates business to Thailand, assigning production and sales responsibilities to the new subsidiary.”

But Three Circle did not always use the Thai route.

Trade data shows a related entity, Hong Kong Threecircle Electronic, shipping “ceramic substrate for fuel cell application” directly to Bloom under its own name between 2024 and 2025.

Glory Winner hasn’t shipped to Bloom since November 2025 according to the trade data, over six months after the Bloom CEO’s repeated denial of reliance on Chinese scandium during the earnings call. But Three Circle told investors as recently as December that it “has established a long-term cooperative relationship with Bloom Energy and is its main supplier of fuel cell membrane sheets,” according to Chinese media.

The company, which happens to be listing in Hong Kong this week, did not name Bloom directly in its IPO prospectus. Instead it said its largest customer in 2023, 2024, and 2025 is a “public company listed in the U.S. that mainly engages in development and production of reliable new energy products.” It also disclosed: “SOFC electrolyte sheets have been supplied to a leading North American fuel cell company.”

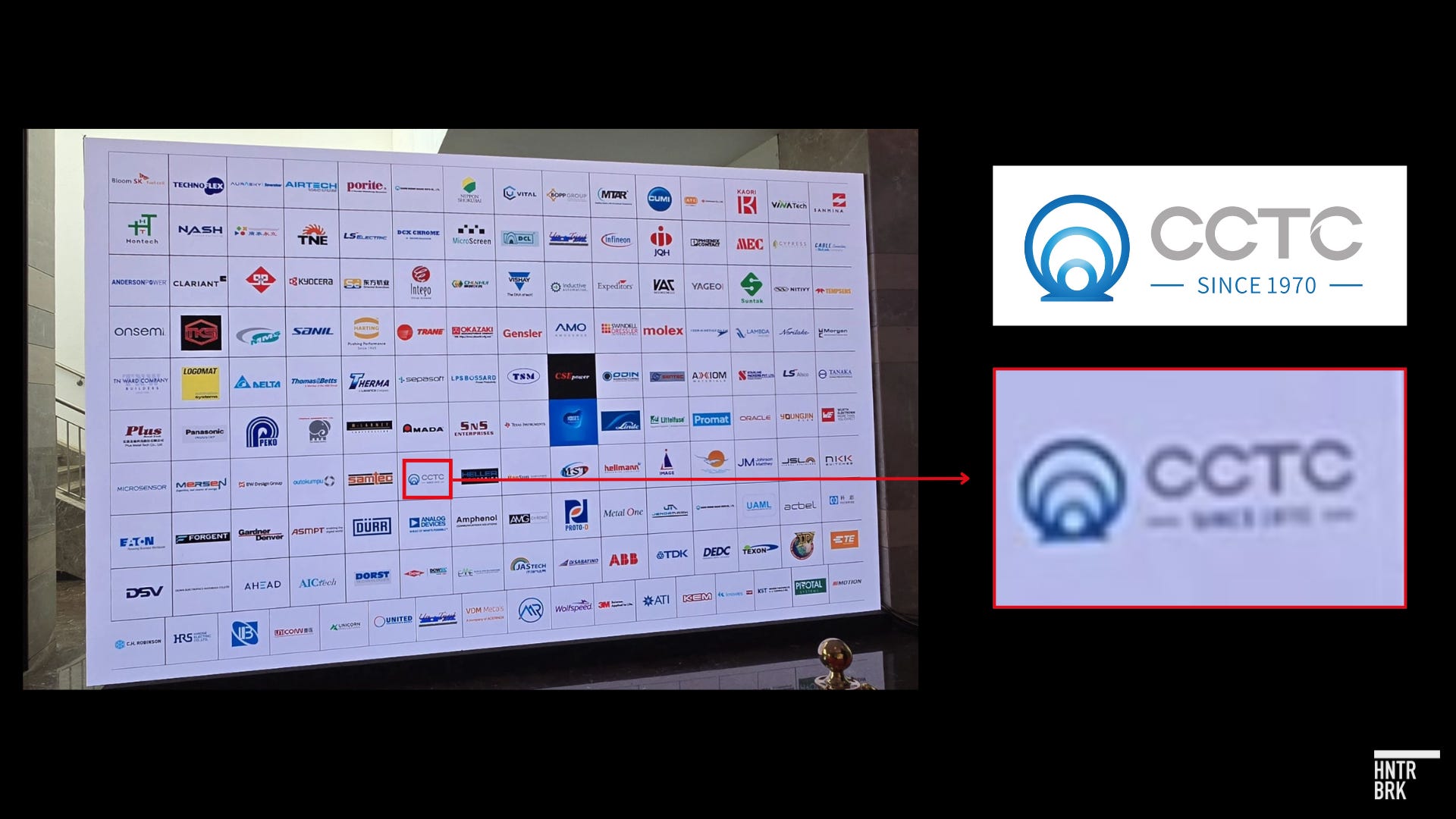

Similarly to Hunan Oriental Scandium’s logo, Three Circle’s logo appeared on a logo wall at Bloom’s May 2026 supplier conference, indicating the two companies are still doing business together.

But while the apparent rerouting through Three Circle’s Thailand subsidiary might help evade U.S. tariffs, it likely will do nothing to mitigate Beijing’s export control choke point, as Hunterbrook’s conversation with Hunan Oriental indicated.

When Hunterbrook asked Hunan Oriental about procuring via an intermediary in a third country, the company’s representative walked through the rigorous disclosure requirement that included explicit disclosures from the end user, including financial information, as well as business scope and main products produced. The ultimate end user had to directly provide the information to the exporter before the product could be shipped.

“Whether the declaration is approved depends on the Ministry of Commerce’s review of the buyer and the intended use of the products,” the rep said, adding the process typically takes 45 days.

The requirements also include a commercial inspection, the rep said.

“No step can be skipped.”

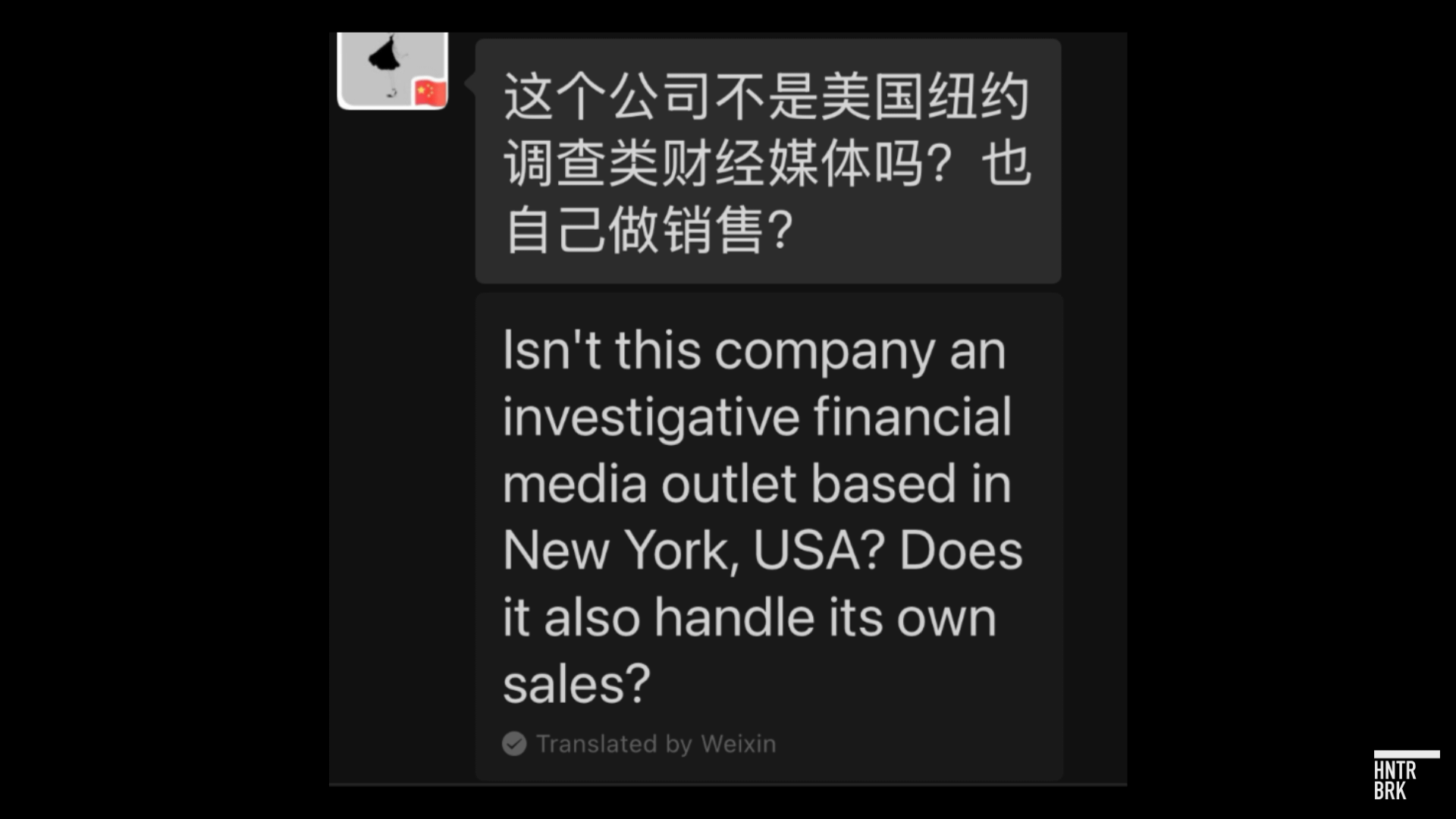

It’s a rigorous process. So rigorous that Hunan Oriental’s second representative had questions about the end user for the sale it was discussing, asking Hunterbrook’s journalist: “Isn’t this company an investigative financial media outlet based in New York, USA?”

ROUTE 2: A JAPANESE SUPPLIER’S CHINESE TRADING ARM

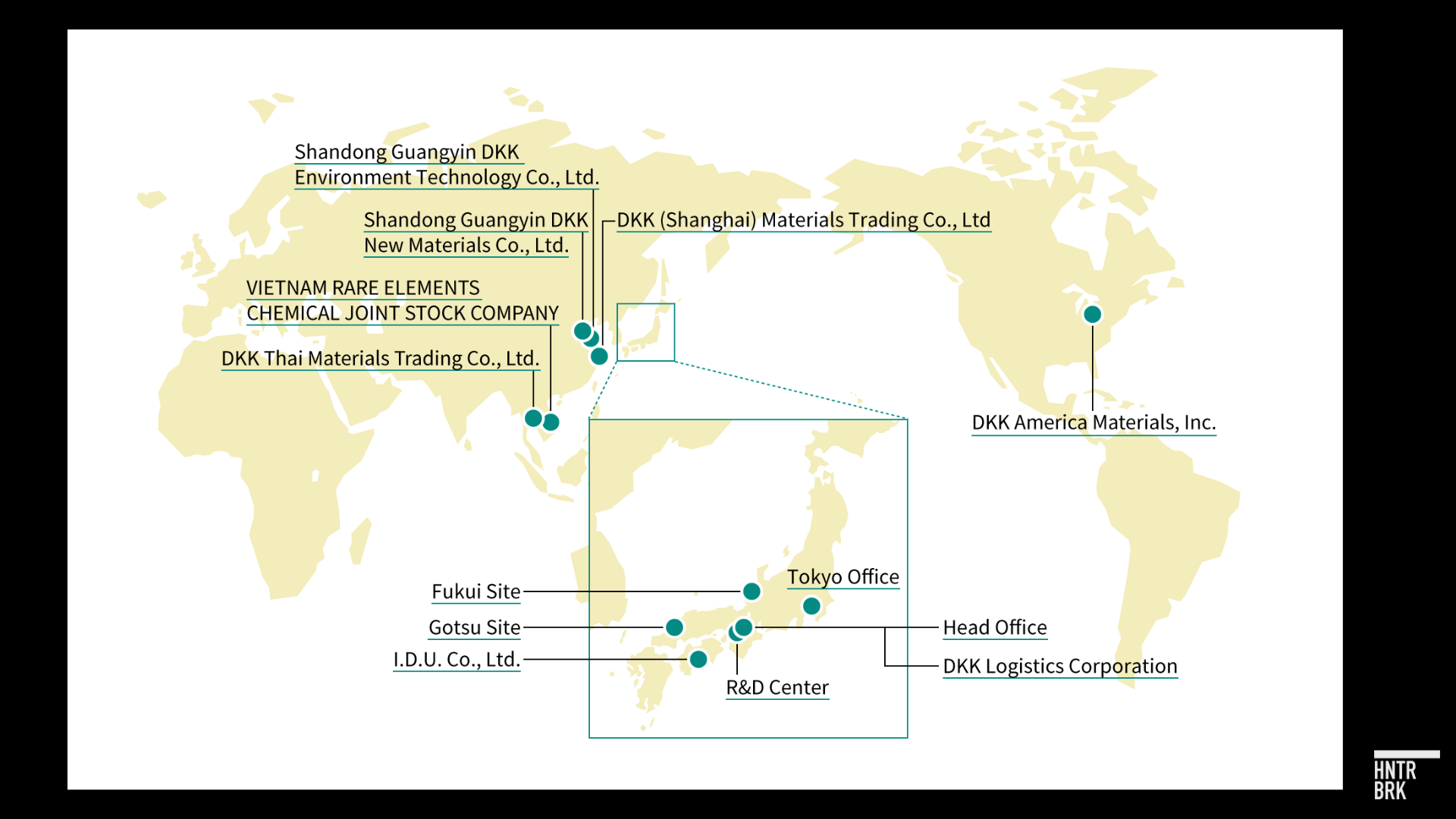

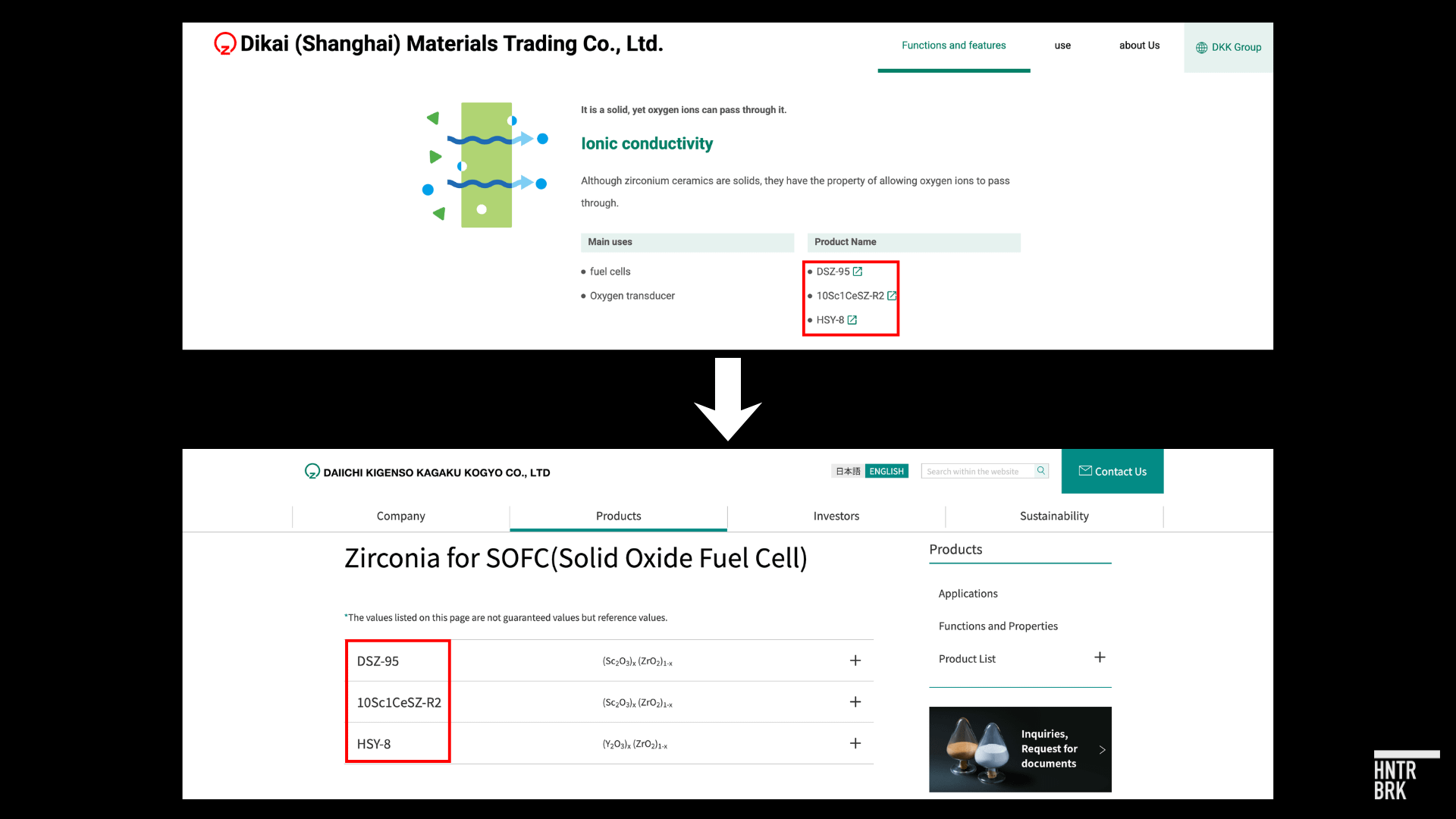

Bloom also receives “scandia-stabilized zirconia powder” from Daiichi Kigenso Kagaku Kogyo (DKK) in Japan, according to import records reviewed by Hunterbrook. The powder is the raw version of the critical material the fuel cell manufacturer needs for its electrolytes. Since September 2024, Bloom has received almost 300 drums of “scandia” or “scandia-stabilized” powder, though not all was labeled as zirconia powder. While they were shipped from Japan, a look at DKK’s corporate structure suggests the powder’s actual provenance is China.

The Japanese materials manufacturer’s corporate network includes two Chinese “associated companies” and one Chinese subsidiary, DKK (Shanghai) Materials Trading, which specializes in zirconium compounds.

Its website features scandium prominently. The product page links to DKK’s Japanese website of zirconia for solid oxide fuel cells, the type of scandia-stabilized zirconia powder Bloom bought from DKK, suggesting the Japanese company sources from its Chinese subsidiary.

A possible non-Chinese source of scandium for a Japanese supplier is Sumitomo Metal Mining, which recovers scandium as a byproduct at its nickel operation in the Philippines and refines it into scandium oxide in Japan. Sumitomo Metal Mining said in 2016 that it had signed a long-term scandium supply deal with an unnamed “major U.S.-based fuel cell manufacturer,” widely believed to be Bloom.

But that operation has remained small. Philippine government data from the Mines and Geosciences Bureau’s Caraga office shows scandium oxalate output from the region that hosts Sumitomo’s Taganito operation hasn’t meaningfully exceeded 8 tons in a year in scandium-oxide equivalent (there’s about 1 ton of usable scandium oxide from each 3 tons of scandium oxalate). Sumitomo said in May that it planned to increase scandium production capacity, and Japanese press reported the increase at about 20%. That’s a fraction of what Bloom needs. The USGS does not list Japan among countries where scandium resources have been identified.

That leaves DKK’s Chinese subsidiary as a more probable origin of the powder shipped from Japan.

In recent financial filings, DKK does not mention scandium specifically, but the company flags that for “medium-to-heavy rare earths, production is heavily concentrated in China, and the impact of export restrictions persists.”

A 2026 DKK-commissioned analyst report expressly flags that the company uses scandium oxide in “zirconia for fuel cells” and that the material is subject to Chinese export controls, suggesting once again that the company is sourcing it from China.

ROUTE 3: THROUGH BLOOM’S PARTNERS IN SOUTH KOREA

In 2024, Korean media reported a local success story. The company KV Materials had effectively localized the production of “electrolyte raw materials and powder” in Korea and would supply these products to Amosense, “a company specializing in materials and components,” to be turned into electrolyte substrates.

Subsequent industry coverage confirmed which trade partner Amosense was producing these components for: “Amosense will accelerate earnings growth by gradually expanding supply volumes following the shipment of the initial batch of solid oxide fuel cell (SOFC) ceramic substrates for Bloom Energy, which was prepared in the first week of March,” Daily Invest reported.

The shipments seem to be ultimately headed to the U.S. to be used for Bloom’s data center push, according to Korean news reports: “As Bloom Energy’s orders expand due to the surge in demand for AI data centers, Amosense’s ceramic substrate production capacity is also expected to expand more than threefold to approximately 50 billion won by the third quarter of this year,” Pinpoint News wrote.

Bloom’s ceramic electrolyte substrates contain scandium, according to its patents. But the USGS doesn’t list South Korea as a nation in which scandium resources have been identified, meaning the scandium baked into the Korean ceramic electrolyte substrates Bloom bought had to come from somewhere else.

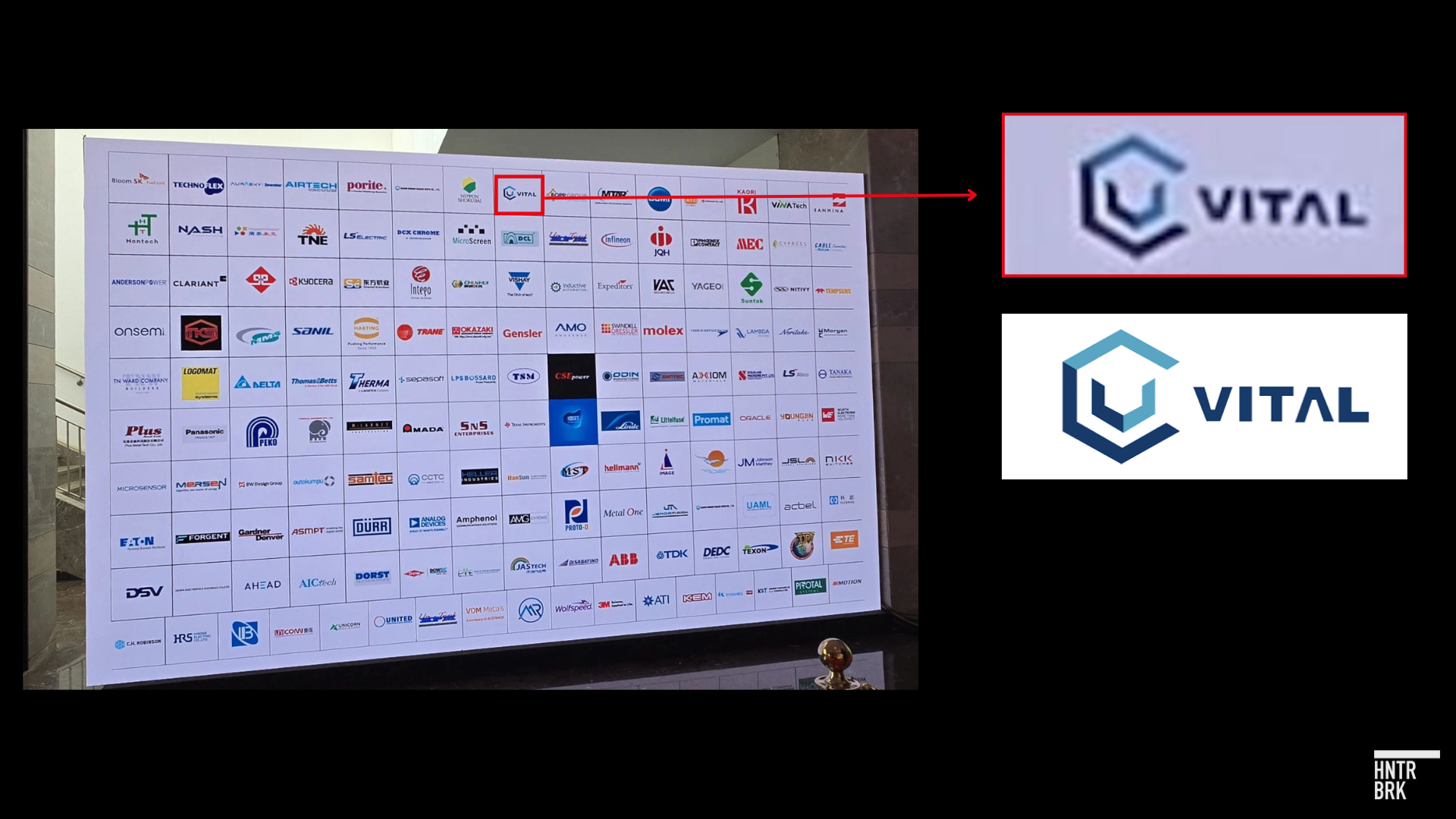

The most likely place seems to be China. KV Materials, which provides the “electrolyte raw materials,” is actually owned by Vital Thin Film Materials, a Chinese scandium-products maker and part of Vital Group, corporate records show.

In January 2024, a Korean newspaper reported that Vital Group had shifted part of its fuel-cell business into the subsidiary with 20 billion won invested into the production. KV’s CEO pledged to make the company “a core hub of Vital Group.”

According to filings in Korea’s corporate disclosure database, KV Materials spent 127 billion won ($83 million) purchasing from its parent company, Vital’s Hong Kong subsidiary, in 2025.

If the scandium powder feeding Bloom traces back to a Chinese parent, then Bloom’s Korean operation would not take China out of the supply chain. It would transform the scandium and obscure its ultimate origin, turning Chinese-sourced scandium into a Korean electrolyte substrate before it reaches the United States.

Vital itself appears to be one of Bloom’s key suppliers. Its logo showed up on the same wall at Bloom’s May 2026 supplier conference as Hunan Oriental Scandium’s and Three Circle’s logos.

Bloom even seemed to have bestowed a special honor on the company: Vital apparently received the “Impact Supplier Award 2025.” The award is given to a supply partner who “significantly advanced our operational success, strengthened resilience and enabled scalable growth across the value chain,” according to a video Bloom posted on its LinkedIn page.

Vital’s North American subsidiary, Vital & FHR North America, has been a known Bloom supplier since 2023 — but the Chinese company’s apparent involvement in Korean electrolyte substrate production for Bloom has not been reported before.

THE TIES THAT BIND

Bloom’s scandium supply chain seemingly has at least four separate links to China: via Hunan Oriental, Japan, Korea, and Thailand.

And Chinese records show Bloom’s relationship with Chinese scandium suppliers goes back more than a decade, despite the CEO’s claims that Bloom has avoided the country since as early as 2005 and never had to “decouple” from China.

In May 2009, Bloom personnel visited China and Bloom signed a cooperation-intent contract with Hunan Rare Earth Technology Development Co. to jointly invest in a rare earth materials production line for Bloom’s fuel-cell division.

According to an April 2010 Chinese media report, Liu Jiaxiang, the director of the Hunan Rare Earth Metal Materials Research Institute, said that Bloom used the institute’s scandium for its fuel cell modules. “For the previous one or two decades, Bloom’s research had not been successful, but the positive electrode made with high-purity scandium oxide reduced the reaction temperature of the fuel cell by more than 200 degrees Celsius,” the article says.

In 2012, a Chinese recruitment notice described Taojiang Ruilong Metal New Materials Co., Ltd. as a joint venture between Hunan Rare Earth Metal Materials Research Institute and Bloom. The company’s business included crude scandium enrichment, high-purity scandium oxide production, and key fuel-cell materials.

And a 2013 Chinese industry-news article said a state research team led by the Beijing General Research Institute for Nonferrous Metals built a 20-ton-per-year high-purity scandium oxide line in cooperation with Bloom Energy.

Bloom acknowledged that its products rely “on a rare earth mineral” from suppliers “primarily located in Asia” several times in SEC filings between 2016 (pre-IPO draft registration statement) and 2019, before removing the mention altogether. The company also repeatedly flagged that it was sourcing from China before 2023 and then apparently dropped Chinese supply chain disclosures from its reports — before they reappeared in its quarterly filing for the third quarter of 2025.

At one point, Bloom appears to have tried to reduce its reliance on Chinese scandium by starting its own U.S. scandium extraction operation. According to an SEC filing ahead of its 2018 IPO, the company disclosed that “a subsidiary of the Company operated a scandium mining operation in the state of Montana pursuant to a lease.” That lease was terminated in April 2016. “The operation did not involve any actual mining, but rather entailed a physical treatment to upgrade the scandium concentration in tailings left on the mine’s surface from past mining operations not related to the Company,” Bloom states in the SEC filing.

Corporate records seem to indicate that this subsidiary was Rye Creek LLC, which reprocessed tailings from the Crystal Mountain in Darby, Montana. The company is still active, according to Montana’s corporate registry. It’s unclear why the Montana mining operation shut down, but this apparent attempt to build a domestic supply chain did not come to fruition.

It’s not just scandium-containing components that Bloom is sourcing from China: A Chinese sell-side analyst report from June also lists various other Chinese companies as Bloom suppliers, for goods ranging from electrolyte separator sheets to interconnects, magnetic components and temperature sensors. Trade data indicates that Bloom received shipments from a Chinese company as recently as Monday.

This is not necessarily surprising. Almost every hardware company has China in its supply chain. But it’s strange considering one of Bloom’s key selling points — one its CEO highlighted in an interview with the Wall Street Journal last month — is that it does not rely on China.

SHOW ME THE SCANDIUM

The math explains why Bloom can’t escape China.

Between its founding in 2001 and 2024, Bloom had deployed a total of approximately 1.4 GW of fuel cells. By 2030, Wall Street is modeling the company scaling to production of up to 5 GW per year, driven by the AI boom.

That’s a big scale up.

How big?

Hunterbrook ran an extensive calculation of scandium supply and demand each year from 2025 through 2030. The deep dive included assessing every identifiable source of potential scandium production and consumption we could find worldwide. All calculation inputs directly cite government filings, Bloom patents, peer-reviewed academic literature, satellite imagery, company statements, and other independent sources.

The takeaway: Reliance on China isn’t even Bloom’s biggest problem. There won’t be enough scandium in the world — let alone outside of China — to meet Bloom’s needs across several years.

Here’s the math.

DEMAND

Bloom won’t say how much scandium it needs for its fuel cells. The public record is full of misinformation.

The Wikipedia page on the Bloom Box, for instance, claims the company requires just “130kg–150kg of scandium per GW,” a figure orders of magnitude lower than the public estimates reviewed by Hunterbrook. The number was added earlier this year by an anonymous editor with no source, and the page’s only scandium citation was flagged as an AI-generated reference.

Even employees have been kept in the dark, a former senior engineering manager told Hunterbrook. “They were very, very quiet about what they did, what they created, what they added,” they said about scandium. “There wasn’t really any understanding of what that was, where they were getting it from, what they needed to secure.”

So Hunterbrook built the number, measured in metric tons, from scratch, using two independent methods that converge.

METHOD 1: COUNT THE ATOMS

Bloom’s electrolyte is a ceramic material made from scandia-stabilized zirconia. In a solid oxide fuel cell, the electrolyte separates the anode and cathode and conducts oxygen ions; at the anode, those ions react with natural-gas-derived fuel in an electrochemical process that produces electricity without combustion.

The high operating temperatures of fuel cells mean that plain zirconium oxide won’t hold the right crystal structure as it cools: It cracks and loses conductivity. So you “stabilize” zirconia by mixing in another oxide. Bloom chose scandium oxide, which has superior properties to alternatives like yttria.

Bloom’s patents describe that mix at around 10 mol%.1 That means that out of every 100 oxide molecules in the ceramic, 10 are scandia and 90 are zirconia. Because a scandia molecule is a bit heavier than a zirconia molecule, 10 mol% works out to roughly 11% of the electrolyte by weight.

That’s the recipe. The next question is how much ceramic electrolyte each cell actually contains.

A 2021 Bloom technical deck put the company’s electrolyte at a 100-micron thickness, producing 25 watts per cell. Bloom repeated the same watt figure in a 2022 deck. Hunterbrook modeled each cell at roughly 100 square centimeters of active electrolyte area, nearly identical to the 99-square-centimeter active-area input in a Department of Energy stack-cost model which uses Bloom as a benchmark.

Run the geometry through the density of the ceramic, and each finished 100-kW stack has roughly 2.5 kilograms of scandium oxide baked inside it.

That’s roughly 25 tons per GW actually sealed into sellable products.2

But a factory has to buy more powder than ends up being used in finished cells.

A Bloom-authored white paper says each step from stack to column to power module has a “yield loss,” meaning some parts, which could contain scandium, don’t pass to the next build stage. Models tied to the U.S. Department of Energy put numbers around that: A mature-process case gets to roughly 85% yield3 and a downside case gets to roughly 65%.4 Hunterbrook modeled an 85% yield in the best case and 65% yield in the downside case, then used the midpoint for the central estimate.

At that rate, the scandium Bloom actually has to purchase climbs to roughly 3.0 to 3.9 kilograms per 100 kW, depending on the scenario.

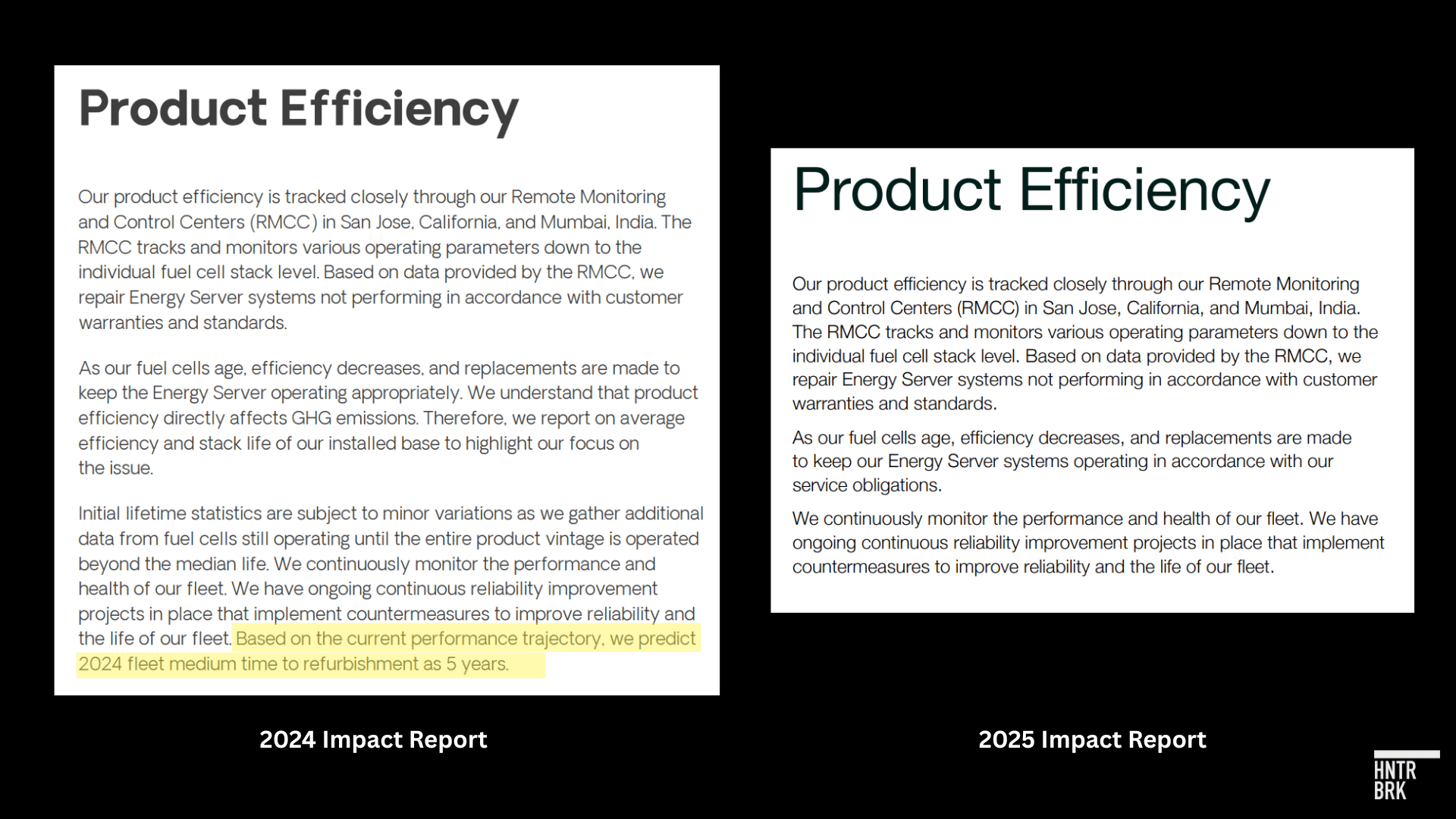

That assumes Bloom has been honest about its stack life, which has been questioned in the past. And between its 2024 and 2025 Impact Reports, Bloom made its language regarding the life of its fuel cells much more conservative. In 2024, the company said: “We predict 2024 fleet medium time to refurbishment as 5 years.” In 2025, the company deleted that language, saying only: “As our fuel cells age, efficiency decreases, and replacements are made.”

Bloom statements about product efficiency in its 2024 and 2025 Impact Reports (highlight added by Hunterbrook). Source: Bloom Energy

That’s one approach to modeling Bloom’s scandium need. Here’s a second.

METHOD 2: FOLLOW THE MARKET

We checked our bottom-up model answer against the market, from the top down.

That starts with the question: How much of the world’s scandium supply is consumed by solid-oxide fuel cells (SOFCs)?

Two industry reports put SOFCs at roughly two-thirds or more of total scandium oxide consumption.

Sunrise Energy Metals, in a 2026 feasibility study, estimated global demand for high-purity scandium oxide at 50 to 60 metric tons per year, with about 40 tons going into SOFC production. A 2025 Asian Metal interview with the general manager of Hunan Oriental Scandium reached almost the same fraction from the other direction: roughly 20 tons of SOFC demand out of about 30 tons of global scandium oxide use.

That does not all belong to Bloom, though the company holds by far the largest share in the industry. A February 2026 Soochow Securities report put Bloom’s SOFC market share at about 75%. That marks a small increase from Fortune Business Insights’ roughly 55% to 65% estimate for 2025 and a separate 2023 estimate of around 60%.

Hunterbrook used the more recent estimates: SOFCs at roughly two-thirds of the 60-ton global scandium demand, and Bloom at 75% of SOFC demand. Multiply them together, and Bloom alone accounts for about 50% of the world’s scandium oxide consumption. This may be conservative, as some of Bloom’s SOFC competitors, like the Asian giants licensing tech from Ceres Power (Doosan, Delta, Weichai), reportedly don’t rely on scandium.

That leaves another 50% — which, besides the other SOFC makers, is spread across aluminum-scandium alloys for aerospace, military, and automotive applications, as well as thin-film manufacturing for semiconductors and other specialty uses.

That means that Bloom plausibly consumed about 30 tons of global scandium oxide in 2025. What did 30 tons enable? According to analysts, Bloom deployed somewhere around 0.7 to 0.8 GW last year, once you count both new installations and the aging modules it swaps out in the field.5 That implies between about 37 and 43 tons of scandium oxide per GW, a very similar number to the bottom up approach.

Hunterbrook opted for the more conservative number: 37 tons per GW.

Wall Street’s models now assume Bloom deploys between 1 GW and 2 GW fuel cells in 2026 — the volume implied by the company’s raised revenue guidance of $3.4 to $3.8 billion — and scales toward 5 GW a year by 2030, the “manufacturing footprint” Bloom told investors it can already support on its April earnings call, with additional capex.

Analysts have chased the story upward: UBS raised its target to a street-high $350 after the Brookfield expansion, with RBC at $335, even as BMO warned the headline deals do not yet translate into firm contracted backlog.

That ramp is the valuation: At a recent price of $300 a share, Bloom commands a market value around $70 billion — more than 30 times sales and over 100 times forward earnings — and between 13 times and 20 times the billions of annual EBITDA that even a flawlessly executed 5-gigawatt ramp would generate based on sell-side models.

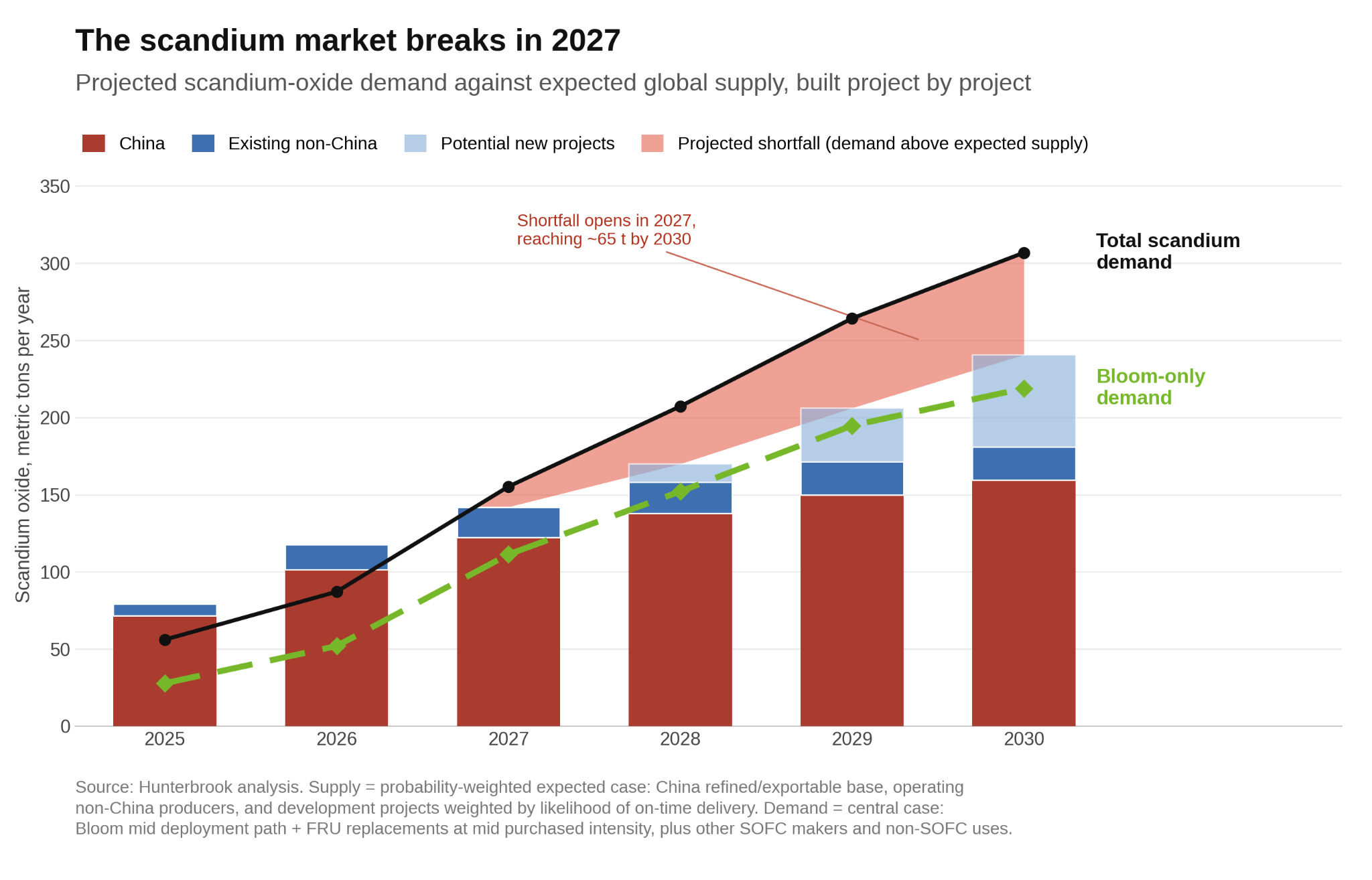

Assuming 5 GW of production in 2030, the company would need about 185 tons of scandium oxide a year — and once you count Bloom’s commitment to replace existing units under warranty (known as field replaceable units, or FRUs), its estimated demand climbs to roughly 220 tons by the end of the decade.

Add the rest of the market — other SOFC makers, aerospace and the aluminum-alloy crowd, et al — and total global demand runs from about 60 tons in 2025 to about 310 tons in 2030.6

That figure introduces some problems. Most importantly, supply.

SUPPLY

Supply does not keep up, even with the model bending certain assumptions in Bloom’s favor.

The model starts by assessing how much scandium is produced in the world now. For that, we counted every publicly available output figure from global suppliers we could find and got about 79.2 tons in 2025, roughly equivalent to the 80 ton figure calculated by the U.S. Geological Survey.

Then we added every announced scandium project and expansion we could find, on its own stated schedule, probability-weighting each one by how far along it actually is.78

Spurred by growing demand prospects from SOFC and auto industries, Western suppliers have signaled intentions to ramp up scandium production, though in reality most are still years from actually producing it. And even the Western supply that does come online may not be Bloom’s to buy — some of it is already optioned to a defense contractor, and at least one potential developer is chasing the auto market. It’s a market where more supply may mean more demand, and as more scandium comes online, more industries will want to adopt it.

In Australia, Sunrise Energy Metals’ project Syerston — designed for 60 tons a year — is only targeting a final investment decision in 2026, with first output around 2028. Lockheed Martin already holds an option on Sunrise’s first 15 tons a year to manufacture fighter jets. Sunrise’s stock has risen over 1,000% in the past year, driven by excitement around the opportunity to sell into the fuel cell supply chain.

And in the U.S., NioCorp’s Elk Creek project in Nebraska — whose primary focus is producing niobium but also plans to produce about 100 tons of scandium oxide a year — has begun pre-construction on a mine portal.

Formal groundbreaking awaits up to $800 million in debt financing the company has sought from the U.S. Export-Import Bank since early 2023. At an investor conference last month, NioCorp CEO Mark Smith said the company hopes to begin full construction by the end of 2026, with production of some products beginning in late 2029. He did not specify whether scandium would be among the first products produced.

But Washington’s interest in the project appears real. The Pentagon has committed up to $10 million in Defense Production Act funding to NioCorp and backs a joint scandium-alloy program with Lockheed’s Skunk Works.

Even in the best case, though, Elk Creek would not close the gap, especially as NioCorp’s stated focus for scandium is automobiles, namely aluminum-scandium alloys to lighten cars, not fuel cells. Peer-reviewed research has indicated that a major demand boost from the auto industry could put meaningful pressure on an already tight scandium market.

Assuming both Sunrise and NioCorp are likely to come online — with several other, more prospective projects less likely — global supply climbs from about 79 tons to about 240 in 2030.

Roughly 160 of that, about two-thirds, is Chinese. The remaining roughly 80 tons is spread across the rest of the world (after applying risk-adjustments to the production capacity of planned but unfinished Western projects). Under these assumptions, the global market enters a deficit. The gap widens every year, to more than 65 tons short in 2030.

Strip out China, and what’s left, the scandium a Western buyer could get its hands on outside the chokepoint, is not even close to enough. That’s why China reliance is necessary, even if not sufficient.

In the model’s expected case, uncommitted Western-deliverable supply covers about 12% of global demand in 2026 and falls to below 10% in 2027 and 2028 — the precise window of the Oracle ramp — before recovering to only about 20% by 2030.

The constraint doesn’t wait for 2030. It starts binding this year.

Some analysts are underwriting far more than the Street’s one-gigawatt base case for 2026 — SemiAnalysis reads Bloom’s raised guidance as implying 1.7 to 1.9 GW of shipments.9 Run a 2 GW year through the model, adding the replacement units Bloom’s aging fleet requires, and the company would need roughly 90 tons of scandium oxide in 2026 — more than one and a half times what the entire world consumed, for every purpose, in 2025.

Global supply does grow this year in the model’s expected case, to roughly 118 tons — but most of the growth, and roughly 86% of the modeled total production, is Chinese. After the rest of the market takes its share — Lockheed’s F-35 chain, aerospace alloys, competing fuel cell makers, about 35 tons in all — approximately 83 tons remain. To produce 2 GW, Bloom needs more than that, according to our model, pulling the global deficit forward from 2027 into 2026.

Others are more conservative. But the outcome isn’t all that different. Run the banks’ own deployment forecasts through the model — Morgan Stanley’s path to 4.7 GW in 2030, Jefferies’ to 5 — and, once the replacement units Bloom’s aging fleet requires are included (TD Cowen estimates about 300 megawatts of field replacements a year today, scaling toward 500), every published Wall Street deployment trajectory reviewed by Hunterbrook pushes the global scandium market into deficit by 2028, according to our estimates of consumption.

And one final consideration makes the picture even bleaker for Bloom.

Hunterbrook’s model includes every ton of scandium oxide supply, whether or not it is fuel-cell grade. But Bloom’s electrolyte does not appear to be made from generic scandium feedstock. Its 2012 offtake agreement with Metallica called for “high purity scandium oxide.” Sumitomo Metal Mining sells 99.9% pure scandium oxide for fuel cells to a customer that is likely Bloom.

The usable pool for Bloom could therefore be smaller than the headline supply number.

All of which is to say: Bloom’s claims of not having a single point of failure are mathematically unsupported. China is integral. And even with China, the math doesn’t work out.

“Right now in the Western world, there’s basically no scandium processing capability to speak of, or just very, very little,” John Mavrogenes, a professor of economic geology at the Australian National University, told Hunterbrook.” It would be a long road to say we’re gonna get serious about scandia.”

Bloom’s July 7 blog post espouses a somewhat different view — noting that scandium is more abundant than lead in the Earth’s crust, and that the amount needed for each cell is little more than “a sprinkle of salt.” But those observations say nothing about how much scandium Bloom actually needs, or can get, in the aggregate. And while the post acknowledges that the diffuse nature of scandium deposits makes mining it an “economics problem,” it implies that Bloom has solved this problem by figuring out that scandium “can be produced” from titanium and nickel waste streams around the world, which is widely known.

Yet again, Bloom says nothing about its actual scandium sourcing operations, nor does it acknowledge that the companies recovering and purifying scandium in this way at commercial scale today are overwhelmingly Chinese — including Bloom’s own suppliers. The flagship Western example, Rio Tinto’s Quebec operation, which recovers scandium from titanium processing exactly as Bloom’s post describes, produces about three tons a year — and the U.S. Defense Logistics Agency is already seeking to buy 6.4 tons from Rio over five years for the national defense stockpile.

And China’s grip on rare earth exports may grow even tighter later this year.

Every scandium shipment leaving China already requires a case-by-case export license under an April 2025 export-control regime that has never been paused, with only select exceptions. But a second, more sweeping set of controls — suspended as part of the Trump-Xi trade truce — snaps back into place automatically on November 10, 2026, unless the truce is extended.

Under Beijing’s “0.1% rule,” modeled on Washington’s own chip controls, any product made anywhere in the world containing Chinese-origin rare earths would itself need a Chinese export license to be sold onward. These rules would presumably reach Bloom’s waypoints in places like Thailand, Japan, and Korea directly.

President Trump left May’s Beijing summit without a rare earths deal, and the White House said only that China had agreed to address shortages of several rare earths, scandium among them.

Beijing doesn’t need a formal ban to act: April 2025 controls took effect, Chinese exports to the U.S. of yttrium — controlled under the same announcement as scandium — collapsed from 333 tons in the eight months before the block to 17 in the eight months through the end of 2025.

No announcement. Just licenses that never came.

THE FIRST OUT

That leaves one lever inside Bloom’s own control, assuming the company hasn’t secretly built a massive stockpile over the last two decades:10 Use less scandium per cell.

Bloom’s patents describe how this could potentially happen. Cheaper co-dopants to cut the scandia fraction. Thinner electrolytes to cut the volume. Push both hard enough and it could drag the market back toward balance early next decade.11

But there is no public evidence we could find that Bloom has reduced the scandium in its cells as of 2026.

And its own patent record argues it can’t easily, because Bloom itself identified under-doped scandia as a cause of accelerated fuel cell aging. Its patented remedy was more dopants, not less.12 Cutting scandium trades directly against stack life, on which Bloom’s 10-to-15-year service contracts and warranty economics depend.

Bloom’s own July 7 statement comes to a similar conclusion: The company says it “has developed other materials that can perform a similar role,” but that scandium “remains the best choice for our current fuel cell platform.”

Unless Bloom accelerates that transition away from scandium, or unless Western mines come online faster than their current schedules suggest, the shortfall leaves Bloom reliant on the same risky Chinese supply chain it repeatedly promised investors it does not depend on.

THE OTHER OUT: MANUFACTURED DEMAND — THE FINANCING MACHINE BEHIND BLOOM’S RECORD QUARTERS

There is one other scenario in which Bloom wouldn’t have a scandium problem: Maybe the 5 GW of demand never shows up — and maybe it’s not even close.

Evaluating this possibility starts with the question: Who is actually buying all the fuel cells that make up Bloom’s revenue and backlog today?

RING AROUND THE ROSIE

The answer, on Bloom’s own books, isn’t hyperscalers — at least not directly. Bloom’s new major sources of revenue are financing vehicles Bloom itself part-owns, which buy the equipment and deploy it in projects serving end customers.

In total, nearly half of Bloom’s 2025 revenue came from buyers Bloom helped create.

Of the $2.02 billion Bloom reported for the year, $892 million — 44% — came from related parties, according to the company’s 10-K. And $862.1 million of that came from the Brookfield “Fund JVs,” entities that did not exist until August of 2025. That is, in roughly five months, joint ventures that Bloom co-owns became the source of approximately 43% of its annual revenue.

In the fourth quarter of 2025, $574 million of Bloom’s $778 million in revenue came from related parties. In the first quarter of 2026, it was $373 million of $751 million.

The related parties include joint ventures formed in August 2025 with Brookfield, with names like Bolt US JVCo LLC and ORC HoldCo LLC. Bloom holds a 9.9% stake in one and 15% in another; Brookfield and its AI fund hold the rest. Bloom sells to these entities and can recognize product revenue when control of the equipment transfers, even when the counterparty is a financing affiliate rather than the ultimate user of the equipment.

Bloom’s own filing acknowledges that its “customers” may not be customers in the way investors assume. A footnote to the concentration-of-risk section states that in certain transactions the counterparty “may be a project-finance affiliate rather than the ultimate end user of the products.”

The filings show Bloom booking this revenue not just before deployment, but before it may even send a bill. A new line item appeared on Bloom’s balance sheet in 2025 — $62.3 million of “non-current” contract assets, revenue recognized where “billing milestones have not been reached” and invoicing sits more than a year out. The line didn’t exist in 2024; 78% of it is related-party.

It raises the question: Where do all the boxes go after the joint ventures buy them?

The answer isn’t clear.

In the eight months from when the deal was formed through March, during which Bloom booked more than $1.2 billion in related-party revenue, nearly all from sales to the Brookfield joint ventures, the partnership has not publicly named its end customers. The $5 billion announcement in 2025 specifically promised a European AI factory site “that will be announced before the end of the year.” It never was, at least not in a direct enough way for Hunterbrook to find — and the companies’ June 30 announcement of a $25 billion expansion nine months later makes no mention of the European site at all.

The closest thing to a named tenant is a company Brookfield created itself. In February, Brookfield launched Radiant, a “vertically integrated AI infrastructure company” formed by merging its in-house venture with a London startup, Ori Industries. Radiant describes itself as the “first compute deployment vehicle and second seed investment” of Brookfield’s AI Infrastructure Fund — the same fund whose first seed investment was the Bloom framework — and, per trade press reporting, it will get first dibs on capacity at the fund’s new sites.

Radiant has announced no chief executive — its leadership appears to be a Brookfield managing director serving as executive chair and the startup’s founder as president — and no publicly named customers.

What it has announced is what it will buy: Radiant is an “NVIDIA Cloud Partner“ whose AI factories will be “based on the NVIDIA DSX reference design“ and stocked with Nvidia’s latest chips. Nvidia, in turn, anchors the Brookfield fund.

The circle closes itself: Nvidia backs the fund; the fund’s vehicles buy Bloom’s fuel cells; the boxes await AI factories whose designated first tenant is Brookfield’s own cloud company; and that company exists to buy Nvidia hardware. At every point in the loop, the demand comes from inside the partnership.

But you might not know this was the end customer from listening to Bloom’s executives. Bloom hasn’t mentioned “Brookfield” since the first earnings call after the partnership was formed.

On the other hand: None of this is exactly concealed. It’s disclosed in footnotes. Deloitte flagged the JV accounting as a critical audit matter.

BACKLOGGED BACKLOG

Bloom, in any case, isn’t being valued primarily on any one customer.

It is being valued on the dream of behind-the-meter power. And, for investors, there are two numbers on a balance sheet where dreams generally come true: backlog and remaining performance obligations.

The weird part: In Bloom’s case, those two numbers diverge.

Bloom’s most recent quarterly filing put its RPO at $441.1 million for products and installation, plus $51.5 million for service, as of March 31, 2026.

Its backlog was an order of magnitude larger: $20 billion total, with $6 billion of the backlog attributable to product revenue specifically.

The mismatch is explained by Bloom’s own definitions. Under ASC 606, RPO captures one thing: the transaction price of binding contracts, for obligations not yet fulfilled.

Bloom’s 10-K defines its backlog, an unaudited number, far more expansively, as “revenue attributable to existing contractual commitments for the purchase or use of Energy Servers by a financier or an end customer,” a figure that “reflects anticipated ITC and other tax incentives as applicable.”

Read those clauses one at a time.

“Or use” means the backlog counts arrangements where no one has committed to buy anything, only to take power.

“A financier” means a commitment from a financing vehicle, like the Brookfield joint ventures Bloom part-owns, counts the same as an order from an actual customer.

And “anticipated ITC” means the backlog includes tax credits Bloom hopes to receive from the U.S. Treasury (money from the government), folded into a number marketed as customer demand.

The service side stretches further still: Bloom counts “5 to 20 years” of future maintenance revenue in its $14 billion service backlog while disclosing, in the same paragraph, that those contracts are “subject to termination for convenience on an annual basis.”

The audited service RPO, the portion that actually binds, is $25 million.

This is not how others in the industry do it.

GE Vernova’s 2025 earnings release shows a backlog of $150 billion and defines the term as “remaining performance obligation.”

Oracle, Microsoft, CoreWeave, and Baker Hughes all market the same number their auditors sign.

Quanta Services, which does fold estimates into its backlog, labels the figure “a non-GAAP financial measure” and reconciles it quarterly.

Across the peers Hunterbrook analyzed, the widest gap between a marketed backlog and audited obligations was about 2x. Bloom’s is above 40x. (Even just isolating the analysis to product revenue, and excluding servicing revenue, the gap is 14x.)

And the quality of that backlog is unclear, as Bloom’s keystone projects appear to be delayed.

DECEPTION IN THE DESERT

In April, Bloom issued Oracle a warrant to buy 3.53 million Bloom shares at $113.28 apiece — roughly $400 million of stock, fully vested and immediately exercisable, on terms the companies had agreed to back in October 2025.

Four days later, Oracle announced it was expanding its partnership with Bloom to “up to” 2.8 gigawatts — only 1.2 GW of it actually contracted.

Bloom’s stock soared. So, too, did the value of Oracle’s warrants. A win-win.

Weeks later, Oracle made another announcement that boosted Bloom’s stock price: The hyperscaler said that a single New Mexico data center campus — Project Jupiter, intended to house infrastructure for OpenAI — would run on up to 2.45 GW of Bloom cells.

Whether Jupiter gets built in the next couple years is itself an open question.

The 17.77-mile gas pipeline required to feed the facility is stuck, as research firm SemiAnalysis reported. And Oracle recently told regulators: “Without a reliable source of natural gas, the power plant that will generate electricity for the data center campus cannot function.” That’s because Bloom’s fuel cells need methane at the campus.

Due to regulatory delays for Oracle’s gas pipeline, SemiAnalysis already pushed its base case for first power from 2027 to 2029. Hunterbrook interviews with four New Mexico officials and a group suing to stymie Oracle indicate it could be delayed into the 2030s, or canceled altogether.

The New Mexico Environment Department (NMED) spokesperson told Hunterbrook it decided on Thursday that Oracle must face opposition at a public hearing. Oracle’s goal: getting a key air permit for emissions from Bloom’s fuel cells.

NMED decided to hold the hearing after public comments were contaminated. Local news reported Oracle’s canvassers collected names and contacts from residents, then submitted supportive comments using their identities, even if the person opposed data centers. Locals found out from an automated NMED email thanking them for input. An Oracle spokesperson denied wrongdoing to local news.

Agency spokesperson Drew Goretzka called it “unprecedented” in an interview with Hunterbrook. He said that NMED “may be pursuing civil or criminal prosecution.” Deputy Cabinet Secretary John Rhoderick at the air permit regulator concluded, “They’re trying to pad the bet with more positive comments.” Without the permit, Oracle cannot install fuel cells, according to the interviews. Bloom’s cells are its sole source of power.

Secrecy is how Jupiter arrived in the desert. The project began with mysterious LLCs that hid their real ownership behind misleading names — Green Chile, after the state’s pepper, and Acoma, after a Pueblo tribe that made the LLC stop using its name due to no relationship.

Only after the New Mexico Environmental Law Center (NMELC) filed lawsuits did the LLCs reveal they were Oracle, building one of the world’s largest data centers for OpenAI.

And Bloom only became part of the project after Oracle withdrew its earlier permit application, which involved even more emissions.

Kacey Hovden, an attorney at NMELC, told Hunterbrook that Oracle’s application is “incredibly incomplete” and “wildly underestimated” emissions from Bloom’s fuel cells, a claim supported by the emissions reports from Bloom’s troubled Wyoming data center, which contradict the New Mexico data.

“Bloom Energy has a really messy past, and I think that they’ve been trying to push this product for seems like decades, without really anyone biting. And I think the data center industry propped them up at just the right time, because it seemed like they were about to go under,” she said. “It’s not this clean energy solution that they claim it to be.”

The backlash now runs throughout the local government. The New Mexico Foundation for Open Government sued over Oracle-related emails. A state legislative aide pointed Hunterbrook to a bill that senators will file next session to block new data centers statewide. The county commission chair Manuel Sanchez laughed when Hunterbrook asked how the outcry compares to past issues. “There’s no contest, this has had by far the most public outcry,” he said, citing residents’ alarm over emissions, water, and the disposal of “hazardous waste.” Hovden specified “benzene and formaldehyde,” and said, “Bloom has a history in California actually of dumping that waste into just local landfills, which then of course impacts folks’ soil quality, water quality, and everything in between.”

Hovden estimated that first power is now likely “early-to-mid 2030s.” Reuters reported last week that Blackstone’s QTS terminated a Virginia data center after “years of local opposition and litigation.” Hovden’s conclusion about Jupiter: It may not happen at all.

WYOMING

The prospects for Bloom’s other flagship project seem to be worsening too.

The timeline of the apparent anchor of AEP’s $2.65 billion fuel-cell investment, a plant near Cheyenne, Wyoming, slipped from “no later than 12/31/2028” in AEP’s February investor deck to “no later than 2030” in its May deck, a potential delay of up to two years in under 90 days.

The data center campus that plant would power reportedly lost its developer in June, when Crusoe was pushed out after the prospective anchor customer — allegedly Google, which has reportedly signed nothing — raised concerns about costs and timelines.

AEP’s CFO disclosed the mechanics on the May earnings call: If the offtake conditions failed by the end of June, the “hyperscaler” customer would get six months to find the equipment another home “anywhere in the U.S.”

If that extension fails, AEP has indicated the utility could force the hyperscaler to pay it back at roughly 110% of “all capital and costs incurred” on the fuel cells.

Whether this would force Bloom to slash its product backlog, nearly 40% of which can be traced to the AEP deal, according to a recent note from analysts at Jefferies, is less clear.

Asked whether AEP would take delivery of fuel cells before its end-customer contracts were final, Sridhar told analysts that Bloom’s servers are “not perishable” and can be redeployed. On the next quarter’s call, he referred to the fuel cells as “portable and fungible.” That is, Sridhar is claiming the boxes can be delivered regardless of whether the specific project moves forward.

“Can,” however, doesn’t mean “will.”

Asked whether it would take delivery of the fuel cells, or instead have its hyperscaler customer reimburse incurred costs at 110%, AEP directed Hunterbrook to the public statements it has already made — including the updated earnings deck.

This is not the first time AEP has run a similar route with Bloom. In the fourth quarter of 2024, AEP agreed to procure up to 1 gigawatt of Bloom’s fuel cells. The first 100 megawatts weren’t bought by AEP’s utility, or by any end customer. They were bought by AEP Development Services, or “Devco” — a subsidiary financed entirely by the parent company’s internal money pool, created to buy the fuel cells and resell them to AEP’s Ohio utility once each installation is “mechanically complete.”

By December 31, 2024, within weeks of the order, Devco’s construction-work-in-progress stood at $457 million, per AEP’s own 10-K. A year later: $480 million. Just $23 million of progress in 12 months.

And the demand the boxes were bought ahead of never really showed up. The end customers were supposed to come through an Ohio program that let AEP sell customer-sited fuel-cell power to data centers. According to the 10-K, that program yielded signed customer contracts for 98 megawatts — about a tenth of the gigawatt AEP contemplated buying. Then the program effectively stalled: Ohio House Bill 15, signed in May 2025, repealed the statute it ran on, “grandfathered the two existing PUCO approved contracts” and barring new ones.

However many Bloom boxes AEP procures, Ohio’s demand under this program is now seemingly frozen at the 98 megawatts already signed.

Even that remnant is contested: In September 2025, according to AEP’s 10-K, an intervenor challenged the approval before the Supreme Court of Ohio, “claiming that the order was unlawful, anti-competitive, and discriminatory.”

That is the pattern, captured in audited numbers on both sides of a single transaction, a year before the Brookfield vehicles existed. Bloom can book revenue, immediately; the buyer can park the equipment in a financing entity; and the demand the purchase was meant to serve is a question for later.

Wyoming is the same architecture at a larger scale. This time AEP’s CEO says the company is doing “a little bit of earthwork” on the site and “waiting for the full release,” indicating it hasn’t frontloaded the entire payment.

BIG BUZZ, FEW DEPLOYMENTS

To sum it all up: The two flagship destinations — Project Jupiter and Cheyenne — are delayed, apparently until at least 2029 and 2030. The Brookfield vehicles that accounted for half to three-quarters of recent revenue have not named a site. And Bloom’s existing deployments are relatively insubstantial.

One data-center fleet Bloom can verifiably point to belongs to Equinix, the world’s largest data-center colocation provider. The partnership began in 2015 as a one-megawatt pilot at a single Silicon Valley facility. A decade later, Bloom’s February 2025 announcement celebrating the milestone put the tally at roughly 75 megawatts operating across 19 Equinix data centers in six states, with 30 more under construction. But in its own chief commercial officer’s words, the fuel cells are “supplementing grid power,” not replacing it. That’s a very different use case than the story driving Bloom’s AI boom.

There is also an alleged 14-megawatt CoreWeave site in Illinois whose commissioning, slated for the third quarter of 2025, Hunterbrook hasn’t been able to confirm; and a Nebius deal that Hunterbrook’s OSINT traced to a New Jersey site where the neocloud seems to buy the power, not the fuel cells, meaning the undisclosed equipment owner is potentially a Brookfield vehicle.

Satellite imagery of the CoreWeave and Nebius sites shows both appear to be making slower progress than initially planned. At Nebius’ New Jersey facility, between 30 and 39.6 MW of generation capacity is installed, according to Hunterbrook estimates — roughly 9% to 12% of the 328 MW deployment that Nebius and Bloom announced on May 20, 2026, which the companies said was “expected to be operational this year“. At CoreWeave’s facility in Volo, Illinois, Hunterbrook estimates roughly 1.6-2.8 MW of installed Bloom generators. Though Bloom has never disclosed the planned fuel cell capacity at Volo, even when measured against the building’s 14 MW power capacity, the installed base amounts to no more than a fifth.13

Bloom also was included in a Texas air permit application for 248 MW of power for a data center in Pawnee, which was approved in June.

The upshot: If the 5 GW ramp is real, the scandium constraint binds, and Beijing holds the off-switch. But it’s unclear there is really as much demand for Bloom’s fuel cells as investors seem to think.

After all, the big headlines for Bloom are often reflective of the same deals at different stages of development — such that a $25 billion “framework,” a $20 billion “backlog,” and billions in “revenue” are not necessarily three independent proofs of demand.

To varying degrees, they can be the same boxes at three stages of one pipeline — financed by a fund using LP money, sold to affiliates ahead of end customers, meant to power data centers that in many cases do not yet exist.

DO YOU HAVE DÉJÀ VU?

Yogi Berra said it best: It’s déjà vu all over again.