Breaking: RadNet Drops Key Metric Hunterbrook Exposed

Multiple former RadNet accountants affirmed Hunterbrook’s reporting. One told Hunterbrook that RadNet’s goal was to present a “better financial picture than what’s truly accurate.”

By: Michelle Cera, Sam Koppelman, Andrew Ford, Laura Wadsten

Editor: Jim Impoco

Hunterbrook Media’s investment affiliate, Hunterbrook Capital, does not have any positions related to this article at the time of publication. Positions may change at any time. Full disclosures on our website.

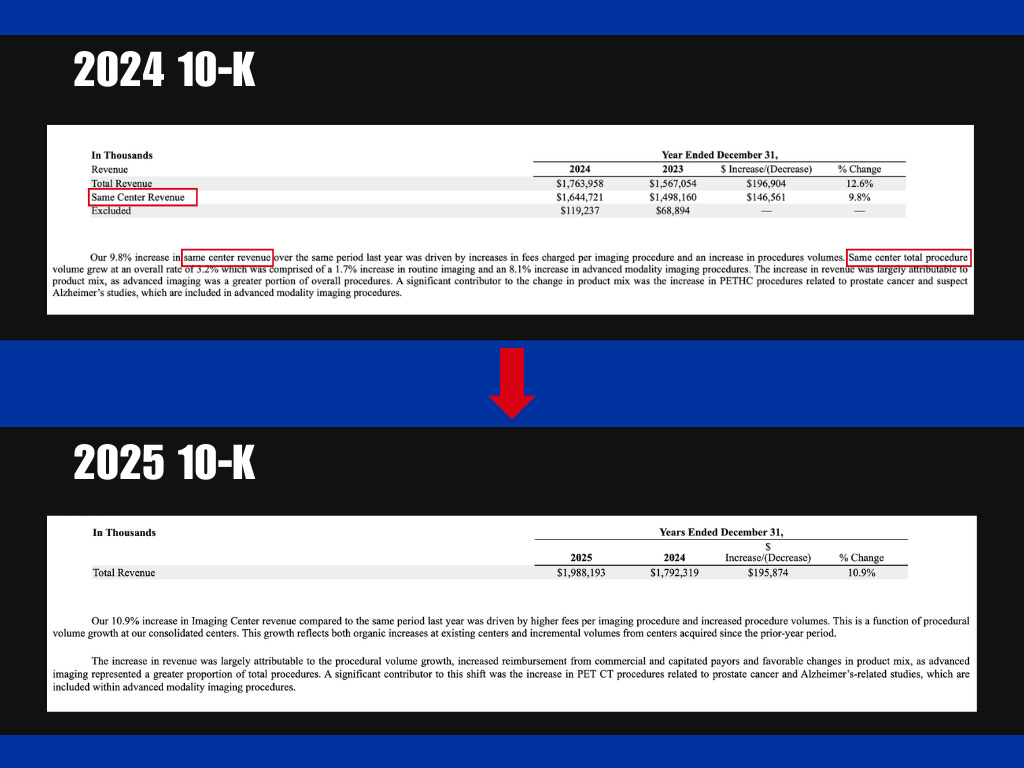

When Hunterbrook Media reported that RadNet ($RDNT) appeared to artificially inflate its same-center sales growth, the company didn’t dispute the findings. It just stopped releasing the number altogether, according to its latest annual SEC filing, released on Monday.

In December 2025, Hunterbrook published a deep dive led by Bethany McLean into RadNet, the radiology roll-up that has repositioned itself as an AI growth story. A central finding: The company’s same-center sales growth — a metric Wall Street pointed to as evidence of RadNet’s special sauce — appeared inflated by the undisclosed consolidations of nearby imaging centers.

This week, RadNet released its latest annual report. The same-center metric … disappeared altogether.

The contrast is stark. In RadNet’s 2024 10-K, “same-center” or “same center” showed up 18 times. This phrase appears a grand total of zero times in RadNet’s 2025 10-K filing.

Notably, RadNet’s most recent unaudited statement, provided in a press release, does still refer to same-center procedure volumes — reporting 9.6% growth in advanced imaging and 4.5% overall in the fourth quarter.1 But those numbers do not allow investors to quantify how much revenue the company is generating year over year on a center-by-center basis.

The change raises an obvious question: If RadNet’s same-center growth were as strong as management repeatedly told investors, why stop reporting it?

It’s the latest example of a company whose accounting practices Hunterbrook has found to be creative — and, potentially, concerning. And now, Hunterbrook’s findings are being corroborated from the inside.

We spoke with multiple former RadNet accounting employees who described an accounting department under pressure to present favorable numbers — and a leadership team whose goal, as one former employee put it, was ”to present a better financial picture than what’s truly accurate.”

Radnet did not reply to Hunterbrook’s request for comment. But at an investor conference this afternoon, RadNet’s CFO Mark Stolper was explicitly asked for his response to allegations in an unnamed report — presumably Hunterbrook’s — that scrutinized same-center growth.

“So just give me your perspective on that report, and just anything you’ve done to maybe change how you present information, to make yourself, inoculate yourself from future [inaudible] on that front,” the moderator said.

Stolper did not address the changes in RadNet’s 10-K and tried to brush aside the concerns raised by Hunterbrook.

“If we do close down a center and we move that volume to an existing center, we keep that volume in the prior period. So we’re not gaming the system at all, which I think was the concern from that report that came out,” Stolper replied.

“So we feel very, very comfortable in how we look at same center performance, and it’s been done consistently with the same team since the beginning of time,” he said. “And ultimately, you know, our GAAP revenue, our audited GAAP revenue and financial statements reflect that growth.”

How RadNet Juiced Its Numbers

Our original investigation reconstructed RadNet’s shifting footprint with archived web data, SEC filings, and independent financial analysts.

The reporting found that RadNet had been closing imaging centers located within a 15-minute drive of other RadNet sites, likely consolidating patients into surviving locations. These closures were excluded from the same-center calculation — but the revenue that transferred to nearby RadNet locations was not.

The result was a metric that made RadNet look like it was growing organically at 6% to 10% per year. A financial analysis shared with Hunterbrook estimated that after removing the artificial boost from consolidations, real same-center growth was closer to 2.5% to 3% — roughly in line with what RadNet’s own CFO, Mark Stolper, described as “normalized” growth before the company’s AI rebrand.

Tiktok failed to load.

Tiktok failed to load.Enable 3rd party cookies or use another browser

On this week’s earnings call, RadNet was asked by an analyst about its growth outlook.

Stolper responded by citing “same-center” performance, claiming it is typically modeled at 3% to 5% — and citing a long-term baseline of 2% to 4%, which often jumps higher.

But he never provided the same-center revenue growth metric RadNet just deleted from its 10-K.

“A Dumpster Fire”: Inside RadNet’s Accounting Department

Since the December investigation, Hunterbrook has spoken with multiple former RadNet accounting employees who worked in the company’s Los Angeles headquarters. Their accounts paint a picture of an accounting department with a chaotic internal culture and a leadership team focused on optics over accuracy.

A former accounting manager who worked at RadNet for two years described “adjustments made on a quarterly basis” to management estimates to make the company’s financial picture look better than it was.

The former employee said that on one occasion, when a manager refused to book a $2.1 million entry to cover underestimated audit fees, leadership simply bypassed them to find a more compliant manager. “Management estimates shouldn’t be changed whenever they feel like it,” the former manager said, adding that estimates were changed “quite frequently and quite drastically.”

The same former employee described a top-down corporate culture where financial statements would change because “adjustments would come through from the highest of the high up and then we just had to book them.”

“And there would be no questions asked…it would get booked and then the numbers would change with no other reason or cause,” they added.

Asked how RadNet’s practices compared to what they’d experienced at another public company, the former employee called it “night and day.” At RadNet, they said, there were “last-minute adjustments to get things to work.” They described the overall tone from leadership as “atrocious,” adding, “They have a goal and that’s to keep the company going, but they also will do whatever it takes to have that happen.”

Another former employee in RadNet’s accounting department, who worked closely with the Digital Health team, described the transactions between divisions as deeply confusing.

“There were so many intercompany transactions that I didn’t even know how they were even reconciling it,” they said. Invoices were miscoded, expenses were booked to closed imaging centers, and managers were rotating so quickly that institutional knowledge was lost, according to the interview.

“Nobody really knew what to, like, do,” they said, adding, “It was a dumpster fire.”

They recalled confusion around imaging centers closing and being absorbed, as well as pressure to cater to directors and VPs. “We were sometimes bullied into doing things that we didn’t particularly think was right,” they said, noting that directors finagled reports in an effort to “roll up better.”

This former employee also described being asked to make minor adjustments to run rates: “I remember actually the VP was saying, telling me, we have to get this right because our share price is kind of going down, too.”

They also described being told to reclassify certain expenses as capitalized assets — a move that would reduce reported expenses and increase reported assets. “Assets going up and expenses going down sounds like a great thing to have happen,” they said, adding that the Digital Health team “always wanted it to be like these things aren’t expenses but capitalized assets.”

The former employee said that at the executive level, leadership “did not care about how it was done as long as it was getting done. They don’t care that it was done right. They just cared that it was being done beneficially for the company … or maybe the best presentation for the company.”

Both former employees recounted a mass exodus of accounting staff, including managers, in 2025.

The Story That Doesn’t Add Up

The decision to quietly drop same-center reporting fits a pattern Hunterbrook has documented: a company whose disclosures shift in ways that make independent verification harder, not easier.

RadNet’s 2025 10-K does show Imaging Center segment revenue of approximately $1.99 billion, up 10.9% from $1.79 billion in 2024 — but investors can no longer see how much of that growth came from existing locations versus acquisitions and consolidations. The company attributes growth to higher fees per procedure, increased procedure volumes, and incremental volumes from acquired centers. But without quantified same-center data in audited financials, it’s impossible to distinguish organic performance from roll-up math.

The same-center question is just one thread in a broader pattern our December investigation uncovered. RadNet’s much-hyped Digital Health division — the foundation of the company’s AI rebrand — generated less than 5% of total revenue in 2025. A former accounting employee was skeptical of this rebrand: “Especially when a company’s kind of touting that they’re going to be the revolutionary change for AI,” they mentioned, questioning whether RadNet “is even capable of implementing something like that in a way that is per generally accepted accounting principles.”

Hunterbrook also reported that RadNet’s disclosures around its center count were riddled with inconsistencies. Its 2024 10-K said 44 centers were opened through internal development; the earnings release said nine. One quarterly filing reported 398 centers; a later filing restated the same period at 375, with no explanation.

Before its AI rebrand, RadNet traded at roughly 8 to 10 times adjusted EBITDA, in line with peers. It now trades at around 18 times — and closer to 24 times once stock compensation and non-capitalized R&D are factored back in. If you strip out the core imaging business at even a generous multiple, the implied valuation of the Digital Health unit tops $3 billion — a staggering price for a division whose products are struggling to find buyers outside of RadNet’s own walls.

Authors

Laura Wadsten is an investigative journalist specializing in healthcare. She began her career reporting on antitrust and healthcare as a Correspondent for The Capitol Forum, a premium financial publication. Laura was a Hodson Scholar and Editor-in-Chief of The News-Letter at Johns Hopkins University, where she earned a B.A. in Medicine, Science & the Humanities.

Sam Koppelman is a New York Times best-selling author who has written books with former United States Attorney General Eric Holder and former United States Acting Solicitor General Neal Katyal. Sam has published in the New York Times, Washington Post, Boston Globe, Time Magazine, and other outlets — and occasionally volunteers on a fire speech for a good cause. He has a B.A. in Government from Harvard, where he was named a John Harvard Scholar and wrote op-eds like “Shut Down Harvard Football,” which he tells us were great for his social life. Sam is based in New York.

Andrew Ford is an investigative journalist who exposed systemic flaws and prompted reforms in healthcare, business, policing, and state government. His reporting was published by ProPublica, USA Today, The Arizona Republic, Asbury Park Press, and Florida Today. He holds a journalism bachelor’s from the University of Florida and received a data analytics master’s from Georgia Institute of Technology. He is based in Phoenix, AZ.

Michelle Cera trained as a sociologist specializing in digital ethnography and pedagogy. She completed her PhD in Sociology at New York University, building on her Bachelor of Arts degree with Highest Honors from the University of California, Berkeley. She has also served as a Workshop Coordinator at NYU’s Anthropology and Sociology Departments, fostering interdisciplinary collaboration and innovative research methodologies.

Editor

Jim Impoco is the award-winning former editor-in-chief of Newsweek who returned the publication to print in 2014. Before that, he was executive editor at Thomson Reuters Digital, Sunday Business Editor at The New York Times, and Assistant Managing Editor at Fortune. Jim, who started his journalism career as a Tokyo-based reporter for The Associated Press and U.S. News & World Report, has a master’s in Chinese and Japanese History from the University of California at Berkeley.

Hunterbrook Media publishes investigative and global reporting — with no ads or paywalls. When articles do not include Material Non-Public Information (MNPI), or “insider info,” they may be provided to our affiliate Hunterbrook Capital, an investment firm which may take financial positions based on our reporting. Subscribe here. Learn more here.

Please contact ideas@hntrbrk.com to share ideas, talent@hntrbrk.com for work opportunities, and press@hntrbrk.com for media inquiries.

LEGAL DISCLAIMER

© 2026 by Hunterbrook Media LLC. When using this website, you acknowledge and accept that such usage is solely at your own discretion and risk. Hunterbrook Media LLC, along with any associated entities, shall not be held responsible for any direct or indirect damages resulting from the use of information provided in any Hunterbrook publications. It is crucial for you to conduct your own research and seek advice from qualified financial, legal, and tax professionals before making any investment decisions based on information obtained from Hunterbrook Media LLC. The content provided by Hunterbrook Media LLC does not constitute an offer to sell, nor a solicitation of an offer to purchase any securities. Furthermore, no securities shall be offered or sold in any jurisdiction where such activities would be contrary to the local securities laws.

Hunterbrook Media LLC is not a registered investment advisor in the United States or any other jurisdiction. We strive to ensure the accuracy and reliability of the information provided, drawing on sources believed to be trustworthy. Nevertheless, this information is provided “as is” without any guarantee of accuracy, timeliness, completeness, or usefulness for any particular purpose. Hunterbrook Media LLC does not guarantee the results obtained from the use of this information. All information presented are opinions based on our analyses and are subject to change without notice, and there is no commitment from Hunterbrook Media LLC to revise or update any information or opinions contained in any report or publication contained on this website. The above content, including all information and opinions presented, is intended solely for educational and information purposes only. Hunterbrook Media LLC authorizes the redistribution of these materials, in whole or in part, provided that such redistribution is for non-commercial, informational purposes only. Redistribution must include this notice and must not alter the materials. Any commercial use, alteration, or other forms of misuse of these materials are strictly prohibited without the express written approval of Hunterbrook Media LLC. Unauthorized use, alteration, or misuse of these materials may result in legal action to enforce our rights, including but not limited to seeking injunctive relief, damages, and any other remedies available under the law.

While 10-K financial statements are audited, these same-center performance indicators are management metrics (often non-GAAP/operational) and are not themselves covered by the auditor’s opinion.