CSG: The Indonesia Problem

How a mystery payment may help explain billions in backlog funneled through a single suspicious intermediary.

By: Jenny Ahn, Till Daldrup, Blake Spendley

Editor: Sam Koppelman

Based on Hunterbrook Media’s reporting, Hunterbrook Capital is short $CSG.AS and long a basket of comparable securities at the time of publication. Positions may change at any time. This article is not investment advice or a recommendation to buy, sell, or hold any security. See our website for full disclosures.

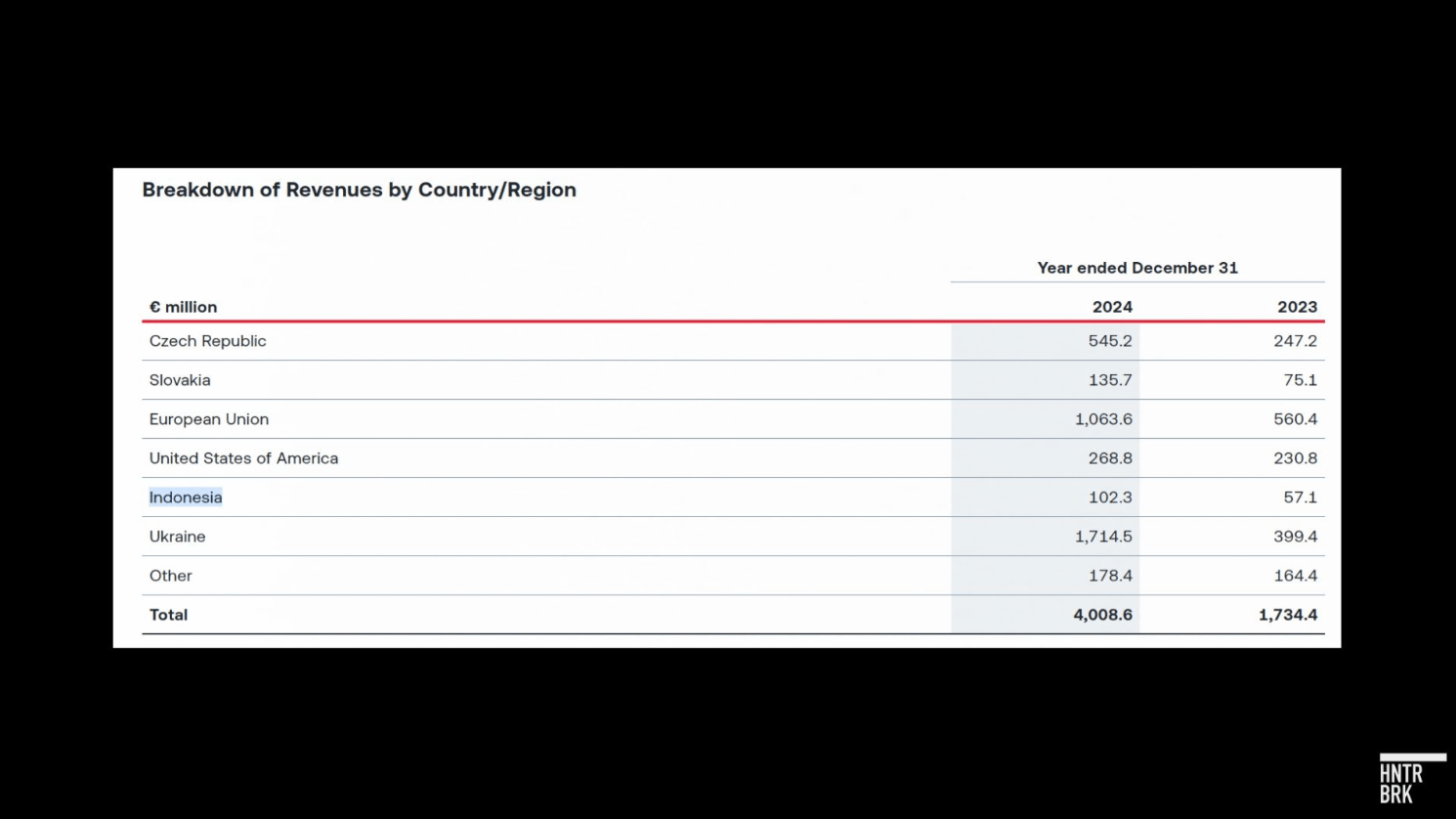

Czechoslovak Group (CSG.AS) has recently announced billions of dollars in contracts with unnamed “Southeast Asian” customers. It appears most of these transactions may actually be with just one counterparty: Indonesia, which CSG used to name explicitly in its filings. CSG’s announced deals tied to this customer since the IPO could amount to up to $2.8 billion, nearly a fifth of the size of CSG’s entire order backlog as of last year, suggesting CSG’s order book may be less diverse than it appears.

Virtually all of CSG’s business in the country appears to flow through a single intermediary, Republikorp, a private Indonesian arms dealer. CSG has no disclosed manufacturing subsidiaries, offices, or employees in Indonesia. Republikorp’s founder, Norman Joesoef, is the son of Indonesia’s former ambassador to Slovakia and was initially named the CEO of Czechoslovak Group Indonesia in 2018, though references to that entity name have since disappeared.

CSG’s history in Indonesia has been marred by controversy, including allegations of bribery and price gouging. In 2023, CSG’s Excalibur Army brokered a $792 million deal for the transfer of 12 used Qatari fighter jets to the Indonesian defense ministry that triggered a public outcry. An Indonesian outlet accused the overpriced deal of including a multi-million dollar kickback to then-defense minister and now-president Prabowo Subianto. Prabowo’s campaign team vigorously denied any kickback but ultimately canceled the deal after public scrutiny.

Hunterbrook also found a paper trail that points to a potential multimillion-euro payment to an intermediary linked to CSG’s business in Indonesia. CSG’s subsidiary filings show a Singapore-based consultant, Irwan Bin Omar — who has operated under the Republikorp brand and described himself as a bridge between EU entrepreneurs and Indonesia — paid 410,000 euros toward a 24% stake in a CSG subsidiary in 2021. In its IPO prospectus, CSG discloses its re-purchase of the subsidiary as an “acquisition” worth 24.4 million euros, requiring a net cash expense of 17.9 million euros. Asked if CSG paid Bin Omar the 17.9 million euros, CSG did not respond to Hunterbrook’s repeated email and phone requests for comment, after previously engaging on Hunterbrook’s prior reporting about CSG’s production rates and IPO disclosures.

It is a weird transaction.

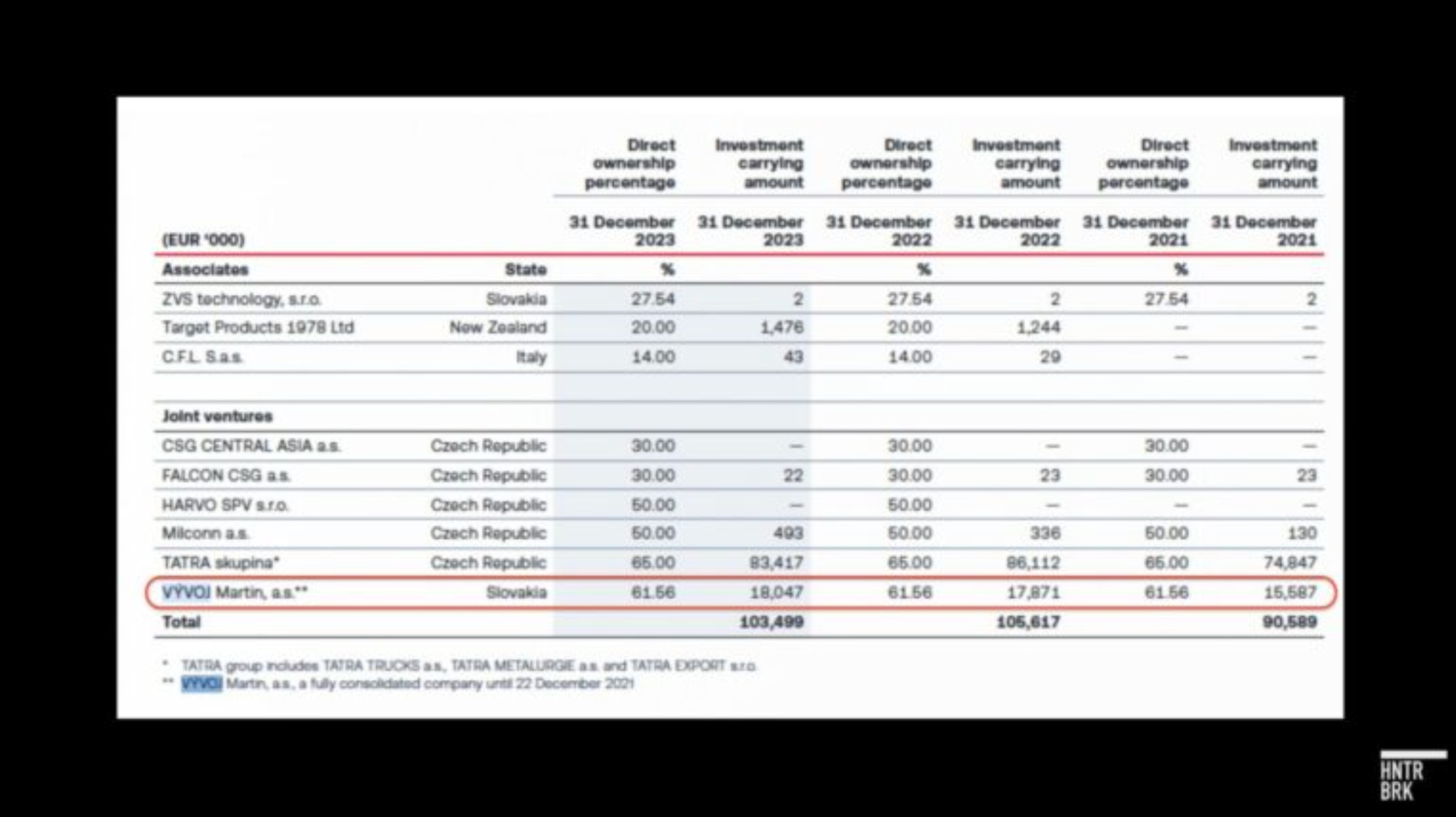

Buried on page 374 of the European defense conglomerate Czechoslovak Group’s 728-page IPO prospectus is a table describing an acquisition of a Slovak subsidiary called Vývoj Martin.

No counterparty is named.

The deal is relatively small — 24.4 million euros — the kind of purchase that’s easy to gloss over when analyzing the prospectus of what was a $30 billion company at the time of the IPO.

But Hunterbrook — whose deep-dive investigation of CSG published earlier in May sparked international coverage and a press tour from the defense conglomerate’s CEO1 — took a closer look.

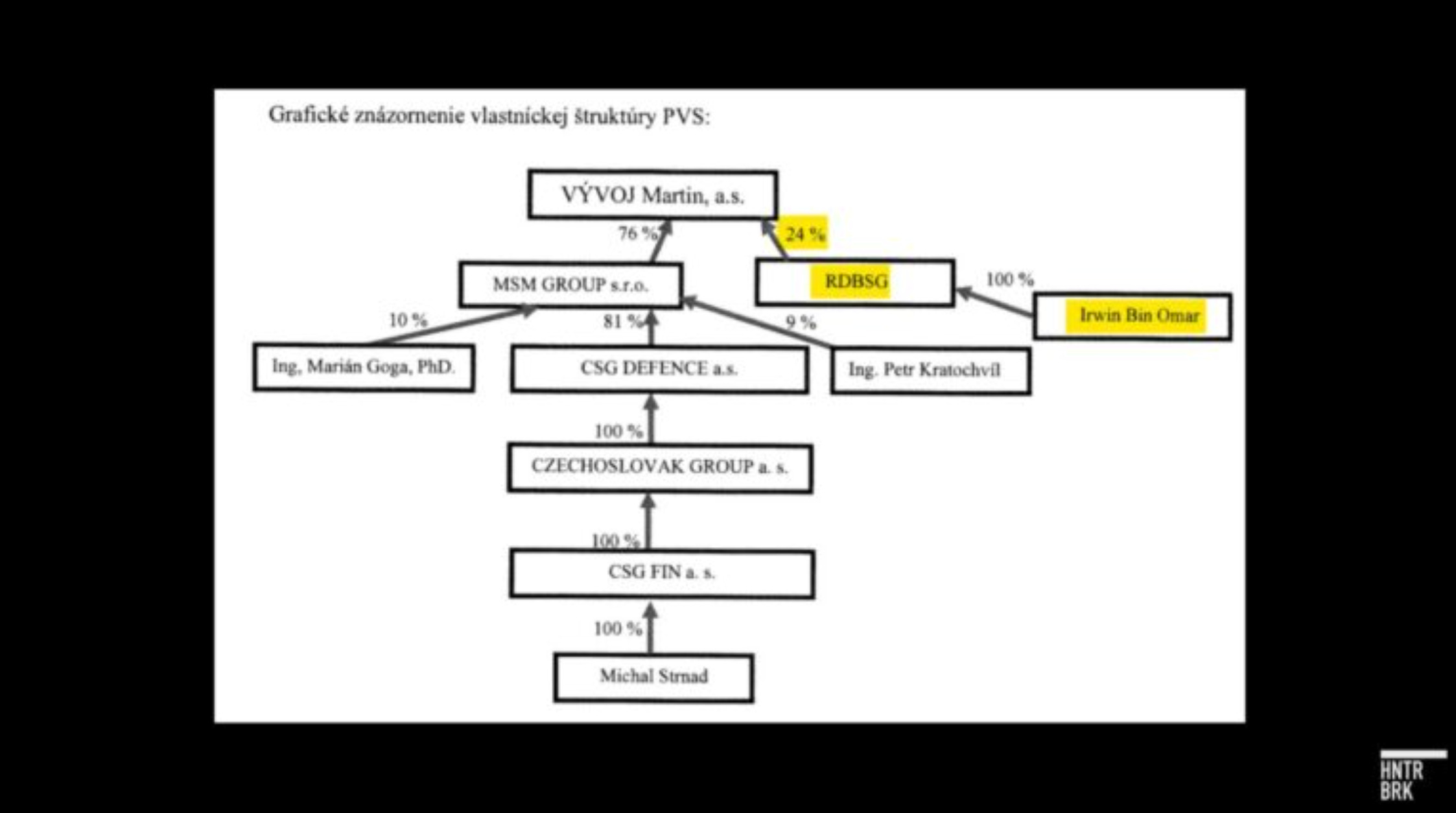

What we found was odd. CSG already owned most of the subsidiary, Vývoj Martin, and seemed to be just buying back a minority share it sold earlier.2 The party CSG appeared to be buying out — a Singapore-based entity called RDBSG — had no known ties with CSG or any European defense companies, as far as Hunterbrook could tell. According to its Singapore registry filings, RDBSG is described as providing “human resource consultancy services.” It has no website and no known representatives other than its sole proprietor, a Singaporean national named Irwan Bin Omar.

Its address, as listed on a Slovak government register, matches a coworking space in an eastern commercial district in Singapore.

In 2021, RDBSG paid CSG a total of 410,000 euros for its stake in Vývoj Martin, Hunterbrook’s review of statutory filings suggests.

Three years later, CSG appeared to have spent about 18 million euros to regain those shares, the prospectus shows.

It’s unclear from the scant disclosures how exactly the cash flowed — and whether the entire 18 million euros in cash went to the shareholder, RDBSG, which would amount to an over 4,000% return on its 410,000-euro investment. But records reviewed by Hunterbrook suggested no other counterparties obviously involved in the transaction.

And CSG’s accounting treatment of the transaction suggests the 18 million euros is real cash that physically left CSG with the repurchase, according to JP Krahel, chair of Loyola University Maryland’s accounting department, whom Hunterbrook asked for an independent expert opinion on the puzzle.

As Hunterbrook dug deeper, our findings showed this transaction may be linked to billions of dollars in contracts CSG had recently announced with unnamed customers in Southeast Asia, where the Czech arms dealer apparently has no employees.

Hunterbrook found, based on our research of defense publications, social media, and CSG’s own past disclosures, that the unnamed Southeast Asian customers may all tie back to just one country — Indonesia — with the deals channeled through a single intermediary, an Indonesian arms dealer called Republikorp.

Those deals would add up to a number roughly equivalent to a fifth of CSG’s total 15 billion euro backlog as of 2025. But more than half of that backlog is related to ammunition sales, contingent on meaningfully expanding production — which may prove to be more difficult than CSG has described to investors, as Hunterbrook found in our previous investigation.

That means the Indonesia sales could amount to nearly half the non-ammunition-related backlog reported by CSG.

And Republikorp, the single conduit of that massive sales channel, seems to be linked with RDBSG, the mysterious counterparty that may have earned a big payday when CSG bought back Vývoj Martin.

NOTE: CSG did not respond to repeated requests for comment — and its filings are (perhaps intentionally!) very ambiguous. So it’s unclear what, exactly, happened here. There could be another, better explanation. If you have one, email ideas@hntrbrk.com.

CSG’s Decade-Long Ties to a Mystery Customer Behind Billions in Orders

In February, 13 days after the IPO, CSG announced a $300 million armored vehicle deal — “the largest export order” of the platform to date. Two months later, another press release announced a $2.5 billion air-defense mega-package. Together, the deals represent nearly a fifth of the size of the total backlog the company reported for the past year.

In each case, CSG identified the buyers only as customers in “Southeast Asia.”

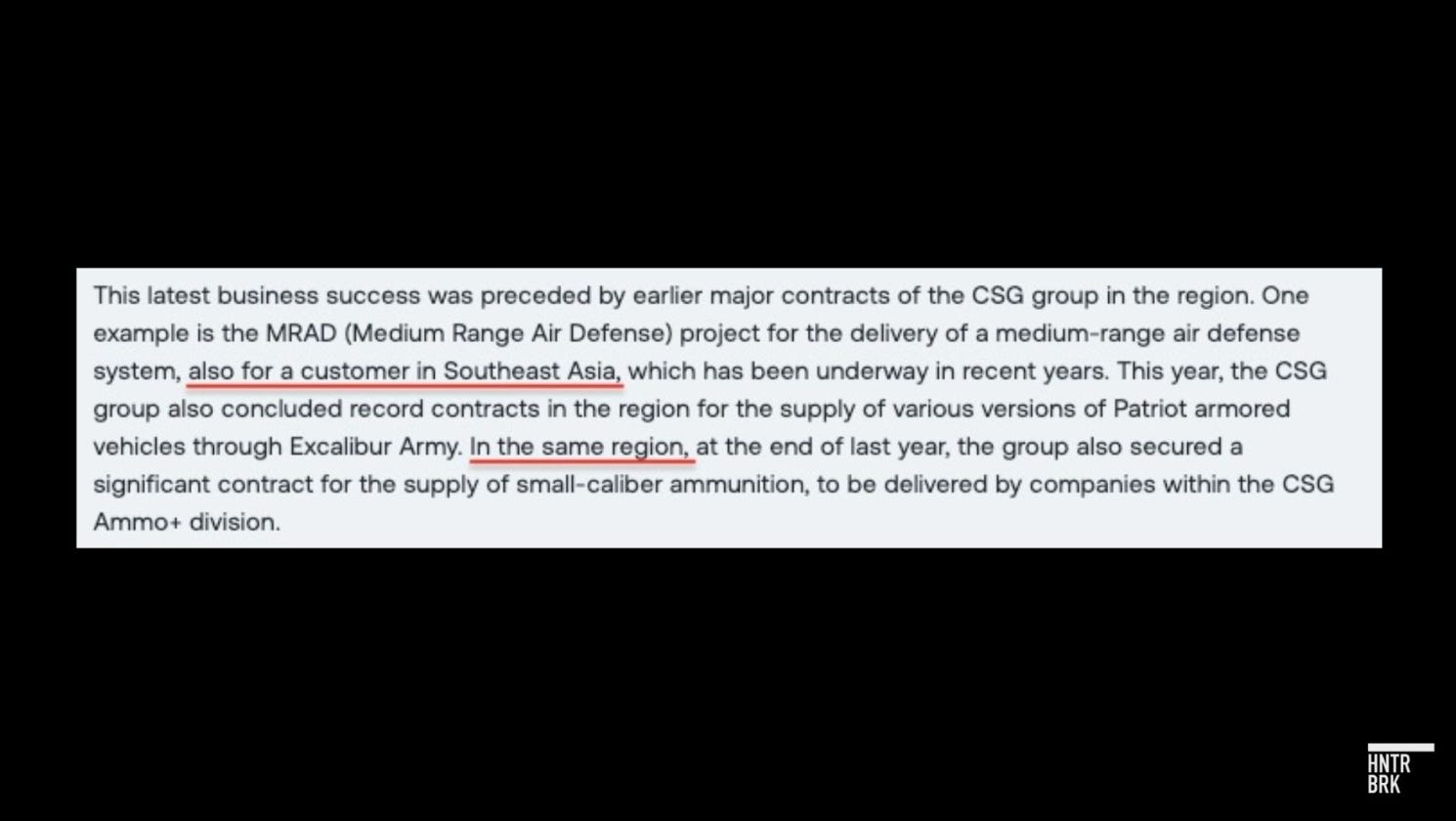

CSG’s April announcement of the $2.5 billion deal also included a list of past deliveries to the same “region” — worded in a way that might lead a reader to assume CSG has a diversity of customers across Southeast Asia.

But CSG was not always so coy. In late 2022, CSG’s subsidiary Excalibur International explicitly named the buyer for a medium-range air-defense system — very likely the same MRAD delivery referenced in the April announcement3 — as Indonesia. And in 2024, Indonesian press confirmed Republikorp was also cooperating with CSG’s majority-owned subsidiary Fiocchi Munizioni on ammunition production — consistent with the small-caliber ammunition contract “in the same region” that CSG referenced in its April announcement.

The 2022 deal — which also included a ballistic missile system and had a price tag of more than 500 million euros — came on the heels of another key deal between CSG subsidiary Excalibur Army and Republikorp for the purchase of 122 rocket launchers on Tatra chassis, potentially worth tens of millions of dollars.4

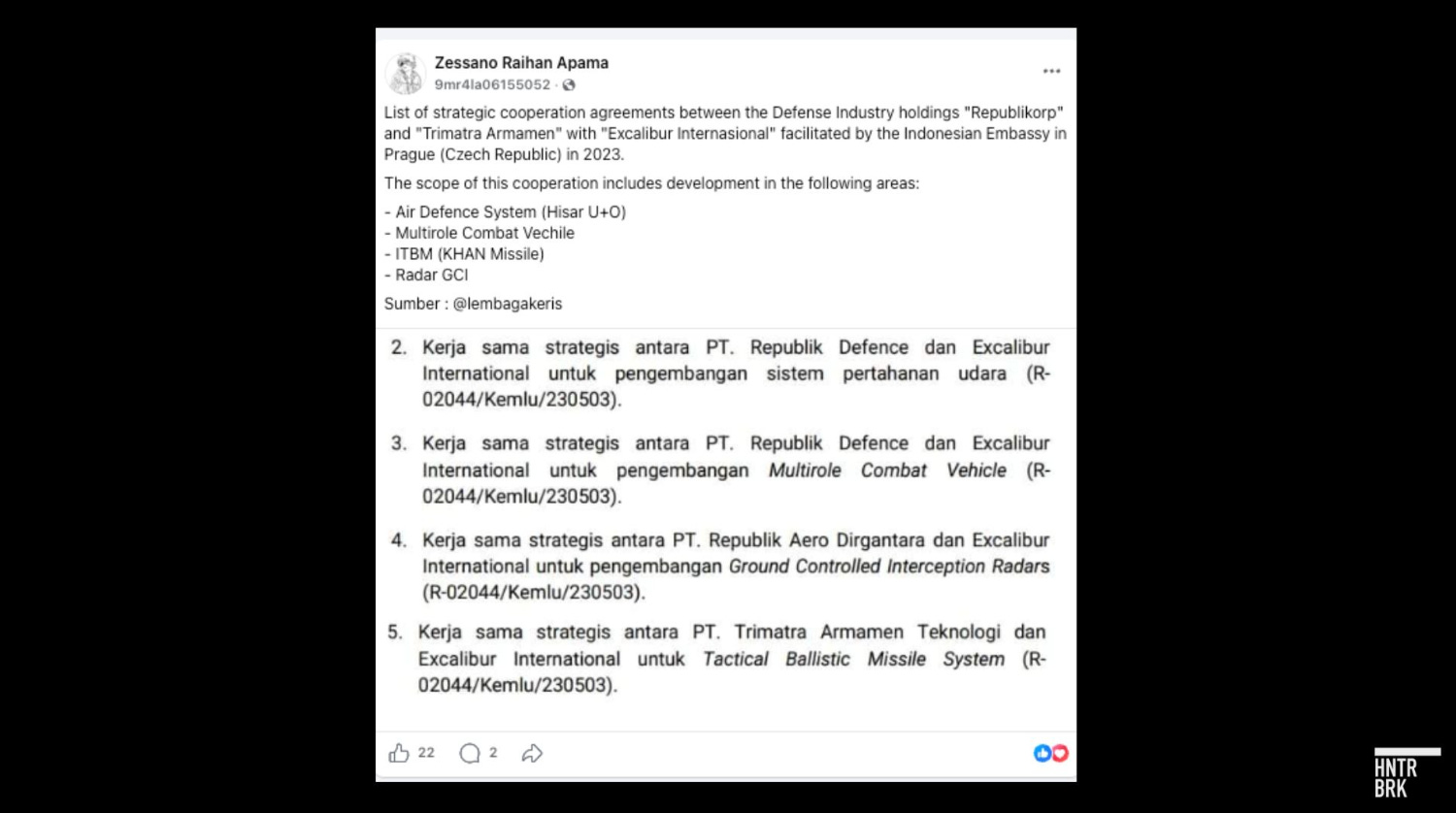

A screenshot of an alleged 2023 Indonesian foreign ministry document posted on a Facebook group for Indonesian military enthusiasts summarizes other strategic agreements between Republik and CSG subsidiary Excalibur International, facilitated by the Indonesian government.

No other Southeast Asian country appears to have had a similar level of cooperation with CSG or institutional infrastructure that could serve a similarly scaled deal, according to Hunterbrook’s review. The only other deal in the region Hunterbrook could identify was what appears to be a 2022–2023 subcontract for 10 armored vehicles supplied to the Philippines through Israel’s Elbit Systems.

But that contract doesn’t seem to have been material enough for CSG to break out the Philippines in the revenue section of its annual disclosures. In CSG’s 2023 and 2024 annual reports — before the company switched to the less granular region-based reporting post-IPO — Indonesia appears to have been the only Southeast Asian country it felt compelled to identify specifically.

The recent $2.5 billion mystery deal appears to be a continuation of the same 2022 air defense system deal.

According to CSG’s press release, the recent contract includes the delivery of complete batteries of multi-layer air defense systems and will utilize Tatra chassis. That’s pretty much how the architecture of the 2022 missile defense systems was described as: Turkish-made missile launchers mounted on Tatra chassis.

Deliveries of a Turkish system mounted on a Tatra chassis began in 2025; a regional defense outlet reported that military enthusiasts spotted a tactical ballistic missile system at an Indonesian army base in Borneo, mounted atop 8×8 Tatra trucks.

At a minimum, those who follow Indonesian military news appear convinced CSG’s mystery customer is Indonesia. In response to a recent article on the $2.5 billion CSG deal published by Indonesian defense news outlet Airspace Review — which did not mention Indonesia as a potential candidate for the unnamed Southeast Asian customer — 300 commenters largely expressed their belief that the mystery customer is Indonesia.

CSG’s Indonesia Deals Marred by Local Controversy

The Indonesian government — along with Republik and CSG — may have its own reason not to publicize the multibillion-dollar deal, given the recent controversy that had previously linked the three names.

In 2023, Excalibur International brokered a $792 million deal to transfer 12 used fighter jets from the Qatari Air Force to the Indonesian defense ministry. Indonesian investigative outlet Ceri reported that Republikorp served as an intermediary for the deal, citing rumors among Indonesian defense ministry officials. The deal, translating to $66 million per jet, triggered an outcry among the Indonesian public, who accused the government of overpaying for old jets that Qatar had once offered to Indonesia for free.

A few months later, a report alleged the deal included a 7% kickback — worth about $55.4 million — to then defense minister Prabowo Subianto, including a $20 million upfront payment.5 Prabowo’s campaign team — he was running for the 2024 presidential election — immediately denied the allegation, describing it as fake news. Indonesia eventually scrapped the deal, citing budget limitations.

The Ambassador’s Son

Across CSG’s deals in Indonesia, virtually everything appears to flow through a single private intermediary: Republikorp.

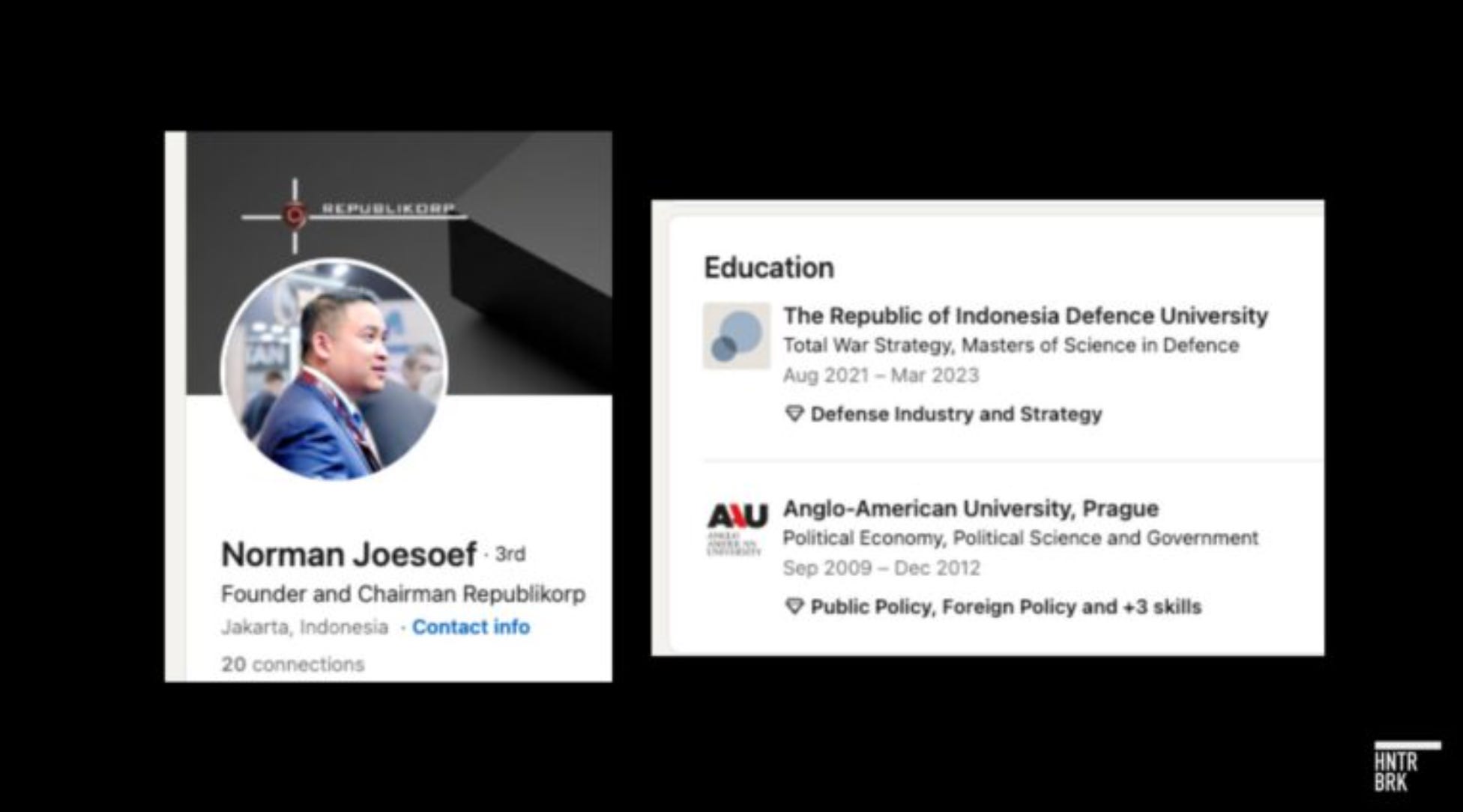

Republikorp’s founder and chairman is a man named Norman Joesoef.

Norman Joesoef appears to be the son of Harsha Edwana Joesoef, a prominent Indonesian businessman and former diplomat. The elder Joesoef is the founder of the RPX Group, Indonesia’s FedEx licensee — and, from 2009 to at least 2012, he served as Indonesia’s ambassador to Slovakia. That posting placed the Joesoef family squarely in the Czech-Slovak diplomatic orbit.

A 2022 social media post celebrating Norman Joesoef’s daughter cites Harsha Joesoef as her grandfather. A 2019 social media post also suggests Harsha Joesoef is Norman Joesoef’s father. Republikorp’s address on its website is the same as the Jakarta headquarters of the Joesoef family’s logistics company RPX in Jakarta.

Norman Joesoef founded Republikorp in 2013 after returning from his studies in Prague, where he was allegedly inspired by a college colleague working in a European defense conglomerate. Joesoef’s school years in Prague likely overlapped with CSG CEO Michal Strnad’s budding career at his father’s company starting in 2010, at around age 17.

Hunterbrook couldn’t confirm if the two actually knew each other in Prague, but what is clear is that the two men have since been doing business together at an enormous scale — and the corporate paper trail connecting Republik to CSG is unambiguous.

One prominent example: In 2018, Strnad pledged to invest $100 million in a new industrial park in Indonesia, to be headed by Norman Joesoef as the CEO of Czechoslovak Group Indonesia, according to Indonesian Antara News.

The reference to Czechoslovak Group Indonesia appears to have disappeared since then, however, with Republikorp — helmed by the same Joesoef — seemingly emerging as CSG’s Indonesian counterpart, creating at least the appearance of an independent entity.

Hunterbrook repeatedly attempted to ask CSG about all of these relationships — also reaching out to Republik, Norman Joesoef, and Bin Omar. Nobody responded to repeated requests for comment.

But one answer may live in that mysterious payment.

A Mystery Figure Tied to the 24.5 Million Euro “Reacquisition” of a Subsidiary

In December 2021, CSG transferred a 24% stake in a Slovak subsidiary, Vývoj Martin, to a Singapore-registered entity called RDBSG, whose sole proprietor is a Singapore national named Irwan Bin Omar. The agreed-upon price was 5.85 million euros, according to a filing by Vývoj Martin’s parent company, MSM Group, with the Slovak commercial registry.

Bin Omar paid 410,000 euros up front. He never paid the rest. The share transfer deal got canceled.

MSM Group’s 2023 annual report says the remaining purchase price “was supposed to be paid, but this did not happen.6” The parties rescinded the deal, with the reverse transfer of shares expected to occur by the end of 2024 and the return of the deposit on the purchase price by no later than mid-2025, MSM Group’s filings show.

That reversal was recorded in CSG’s 2024 annual statement, and on its 2026 IPO prospectus.7

But the way CSG booked this transaction was interesting.

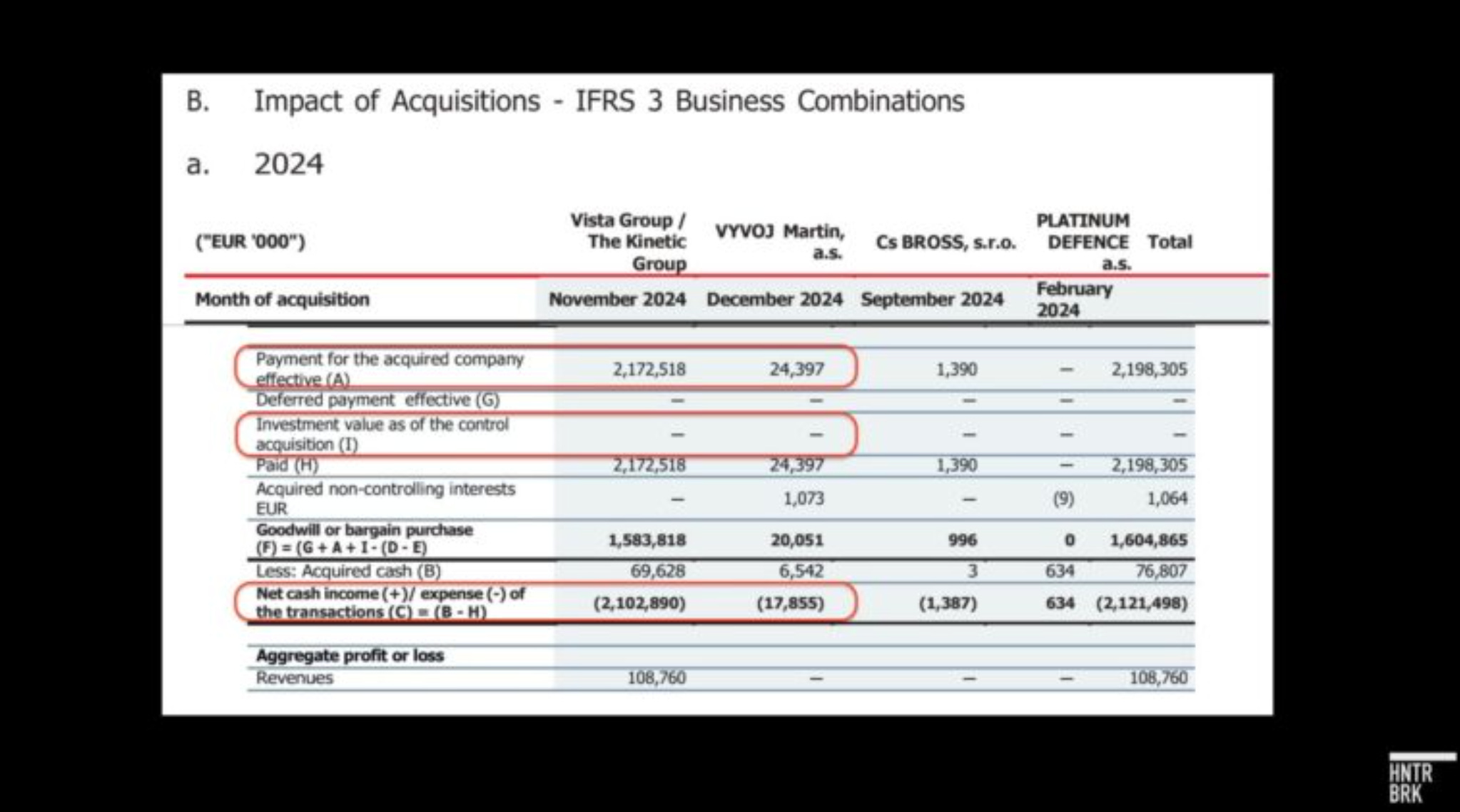

The payment for the reacquisition of those shares was listed as 24.4 million euros — suggesting an over 300% premium on the 5.85 million euros selling price for the shares in 2021.

The magnitude of that valuation increase is also seemingly contradicted by CSG’s own prior disclosures that put the carrying value of its retained majority shares in the subsidiary as having increased far more modestly — at just 16% between 2021 and 2024.

But it gets even weirder. CSG also reported the value of its pre-existing shares in Vývoj Martin as zero — contradicting CSG’s own disclosure, as mentioned above, that its existing shares in Vývoj Martin were worth roughly 18 million euros as of 2023.

The rules of International Financial Reporting Standard 3 (IFRS 3) — the accounting method CSG used for the business combination — are quite clear, as Krahel confirmed to Hunterbrook. “When a company consolidates an entity which it had partially owned, it has to disclose the fair market value of its ownership stake immediately before the acquisition date,” Krahel explained. This disclosure is supposed to go on the “Investment value as of the control acquisition” line of the IFRS table – which, in CSG’s case, was zero.

The implication of this accounting choice — besides being inconsistent with IFRS — could be that the entirety of CSG’s carry value of its existing shares was impaired to nothing, without explanation. Alternatively, CSG may have just wanted to present the acquisition as a fresh one, with the 24.4-million-euro price tag representing the value of the entire entity, and with CSG’s existing interest in the entity buried somewhere in that overall figure.8 That would, potentially, obscure the exact amount of any payment that went to Bin Omar.

Either way, that 24.4 million euro price tag seems to have led to a cash expense from CSG of 17.9 million (24.4 million net of about 6.5 million cash that was held by Vývoj Martin), as recorded in CSG’s prospectus.

The bottom line is, according to the accounting, CSG seems to have spent about 18 million euros as part of a deal to buy back shares it had sold for just 410,000 euros three years prior.

To whom did the 18 million euros go? We don’t know.

But we found no other counterparties aside from Bin Omar related to the reacquisition disclosed by CSG or its subsidiaries.

CSG did not respond to Hunterbrook’s questions about any of it.

But one potential clue may come from the identities of RDBSG and its sole owner, Irwan Bin Omar.

Among Bin Omar’s extensive list of corporate entities he owns is one called Republikorp Project Management Services Pte. Ltd., since renamed the more nondescript Research and Development Innovations.

Hunterbrook could find few details about Bin Omar, but the Republikorp name may be no coincidence. It matches the name of Norman Joesoef’s company, CSG’s counterparty in Indonesia.

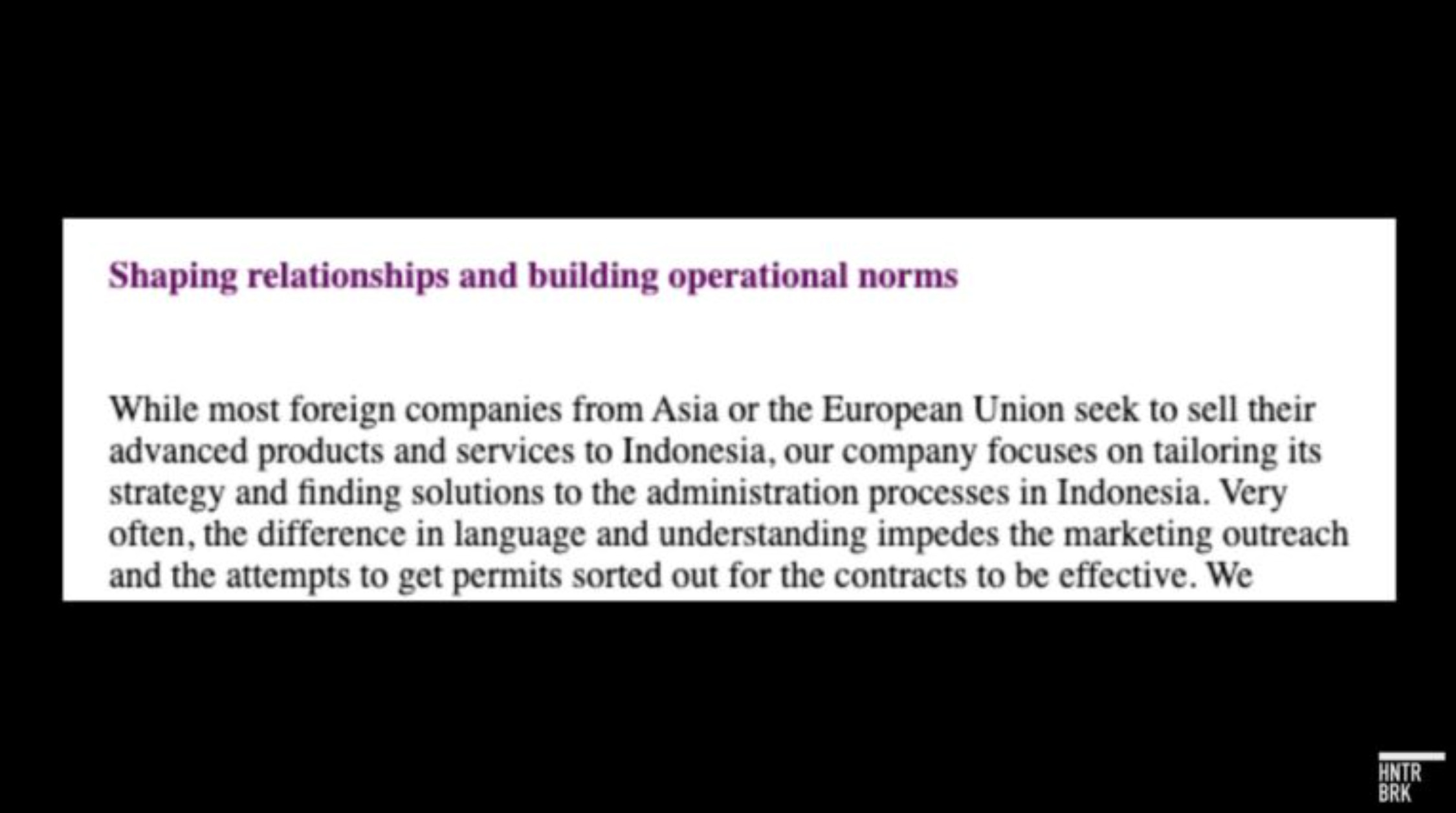

On his own archived website for Republikorp, Bin Omar describes his work as providing foreign companies that “seek to sell their advanced products and services to Indonesia” with “solutions to the administration processes” in the Southeast Asian country. He says he is well-versed in the political context of Indonesia and ASEAN. He studied political science on a joint Singapore-Indonesia scholarship at Gadjah Mada University in Indonesia.

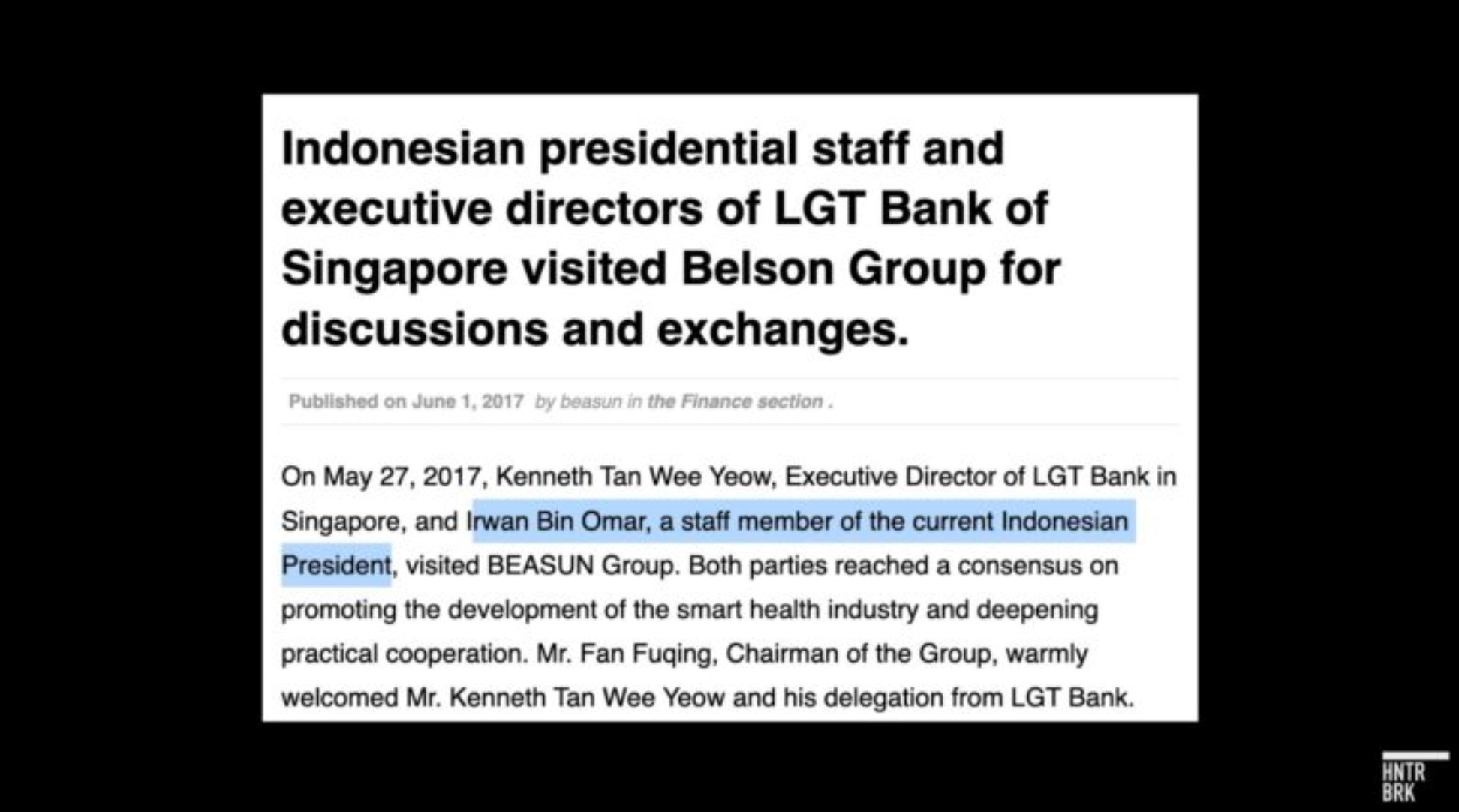

One promotional article appearing on a Chinese outlet in 2017 also described a man with the same name as a member of the Indonesian presidential staff, though Hunterbrook could not independently verify the claim.

After CSG repeatedly ignored emails about Bin Omar — and Republikorp — a Hunterbrook reporter called the company’s spokesperson. “Please communicate in written form,” the spokesperson said.

When the reporter pointed out Hunterbrook’s emails had gone unanswered, and asked for clarity, the spokesperson hung up.

Authors

Jenny Ahn joined Hunterbrook after serving many years as a senior analyst in the US government. She is a seasoned geopolitical expert with a particular focus on the Asia-Pacific and has diverse overseas experience. She has an M.A. in International Affairs from Yale and a B.S. in International Relations from Stanford. Jenny is based in Virginia.

Till Daldrup is an investigative journalist who joined Hunterbrook from The Wall Street Journal, where he focused on open-source investigations and content verification. In 2023, he was part of a team of reporters who won a Gerald Loeb Award for an investigation that revealed how Russia is stealing grain from occupied parts of Ukraine. He has an M.A. in Journalism from New York University and a B.S. in Social Sciences from University of Cologne. He’s also an alum of the Cologne School of Journalism (Kölner Journalistenschule).

Blake Spendley joined Hunterbrook from the Center for Naval Analyses (CNA), where he led investigations as a Research Specialist for the Marine Corps and US Navy. He built and owns the leading open-source intelligence (OSINT) account on X/Twitter, called @OSINTTechnical (over 1 million followers), which also distributes Hunterbrook Media reporting. His OSINT research has been published in Bloomberg, the Wall Street Journal, and The Economist, among other top business outlets. He has a B.A. in Political Science from USC.

Editor

Sam Koppelman is a New York Times best-selling author who has written books with former United States Attorney General Eric Holder and former United States Acting Solicitor General Neal Katyal. He helped build Fenway Strategies into one of the preeminent strategic communications firms in the country. Sam has published in the New York Times, Washington Post, Boston Globe, Time Magazine, and other outlets — and occasionally volunteers on a fire speech for a good cause. He has a BA in Government from Harvard, where he was named a John Harvard Scholar and wrote op-eds like “Shut Down Harvard Football,” which he tells us were great for his social life.

Graphic

Dan DeLorenzo is a creative director with 25 years reporting news through visuals. Since first joining a newsroom graphics department in 2001, he has built teams at Bloomberg News, Bridgewater Associates, and the United Nations, and published groundbreaking visual journalism at The Wall Street Journal, Associated Press, The New York Times, and Business Insider. A passion for the craft has landed him at the helm of newsroom teams, on the ground in humanitarian emergencies, and at the epicenter of the world’s largest hedge fund. He runs DGFX Studio, a creative agency serving top organizations in media, finance, and civil society with data visualization, cartography, and strategic visual intelligence. He moonlights as a professional sailor working toward a USCG captain’s license and is a certified Pilates instructor.

Hunterbrook Media publishes investigative and global reporting — with no ads or paywalls. When articles do not include Material Non-Public Information (MNPI), or “insider info,” they may be provided to our affiliate Hunterbrook Capital, an investment firm which may take financial positions based on our reporting. Subscribe here. Learn more here.

Please contact ideas@hntrbrk.com to share ideas, talent@hntrbrk.com for work opportunities, and press@hntrbrk.com for media inquiries.

LEGAL DISCLAIMER

© 2026 by Hunterbrook Media LLC. When using this website, you acknowledge and accept that such usage is solely at your own discretion and risk. Hunterbrook Media LLC, along with any associated entities, shall not be held responsible for any direct or indirect damages resulting from the use of information provided in any Hunterbrook publications. It is crucial for you to conduct your own research and seek advice from qualified financial, legal, and tax professionals before making any investment decisions based on information obtained from Hunterbrook Media LLC. The content provided by Hunterbrook Media LLC does not constitute an offer to sell, nor a solicitation of an offer to purchase any securities. Furthermore, no securities shall be offered or sold in any jurisdiction where such activities would be contrary to the local securities laws.

Hunterbrook Media LLC is not a registered investment advisor in the United States or any other jurisdiction. We strive to ensure the accuracy and reliability of the information provided, drawing on sources believed to be trustworthy. Nevertheless, this information is provided “as is” without any guarantee of accuracy, timeliness, completeness, or usefulness for any particular purpose. Hunterbrook Media LLC does not guarantee the results obtained from the use of this information. All information presented are opinions based on our analyses and are subject to change without notice, and there is no commitment from Hunterbrook Media LLC to revise or update any information or opinions contained in any report or publication contained on this website. The above content, including all information and opinions presented, is intended solely for educational and information purposes only. Hunterbrook Media LLC authorizes the redistribution of these materials, in whole or in part, provided that such redistribution is for non-commercial, informational purposes only. Redistribution must include this notice and must not alter the materials. Any commercial use, alteration, or other forms of misuse of these materials are strictly prohibited without the express written approval of Hunterbrook Media LLC. Unauthorized use, alteration, or misuse of these materials may result in legal action to enforce our rights, including but not limited to seeking injunctive relief, damages, and any other remedies available under the law.

In a Bloomberg interview, CSG’s CEO said he is now starting an 11 billion euro investment fund separate from CSG that will diversify him away from defense.

According to statutory filings with the Slovak government, CSG owned 61.6% of Vývoj Martin before the reacquisition: CSG owned 81% of MSM Group, Vývoj’s immediate parent, and MSM Group itself owned 76% of Vývoj Martin after MSM Group sold a 24% stake to an entity called RDBSG in 2021. The 2024 reacquisition seemingly involved the repurchase by MSM Group of the 24% minority share in Vývoj Martin. After the reacquisition, CSG again owned 81% of Vyvoj, by virtue of its 81% stake in MSM Group and MSM Group’s 100% ownership of Vyvoj.

The 2022 deal was reportedly in part financed by a Czech bank — believed to be the state-owned Czech Export Bank.

The relationship between CSG and Indonesia in fact extends back further. In 2017, Indonesia purchased four Pandur II armored vehicles from CSG as part of a $39 million contract. In 2019, Indonesia signed an $80 million contract for 22 more Pandur IIs. In these contracts, the deals appear to have been between CSG and PT Pindad, an Indonesian state-owned defense firm. Source: Army Recognition

The report also alleged that a European anti-corruption watchdog, the Group of States Against Corruption (GRECO), had sent a cable to the U.S. Embassy in Jakarta and that an European Investigative Order had opened an investigation on the Czech company. Prabowo’s campaign team claimed that both GRECO and the U.S. State Department denied the investigation; Hunterbrook could not independently corroborate the claims. Source: VOI

The quote is from Hunterbrook’s translation of a sentence in MSM Group’s 2023 annual report, which said (in Slovak): “V priebehu roku 2023 malo dôjsť k zaplateniu zvyšnej časti kúpnej ceny za prevádzané akcie, čo sa nestalo.” English translation: “In the course of 2023, the remaining part of the purchase price for the transferred shares was supposed to be paid, which did not happen.”

MSM Group explained in its 2022 annual report that the 24% share sale resulted in CSG effectively losing control over Vývoj according to the subsidiary’s shareholder agreement. Vývoj Martin subsequently was removed from CSG’s consolidated books and switched to equity-based accounting. The 2024 reacquisition triggered the reconsolidation of Vývoj Martin into CSG’s full portfolio.

The math actually checks out pretty neatly: 24.4 million is almost exactly the implied value of the total share in Vývoj Martin based on the 5.85 million price for 24% shares.