CSG: Why the Largest Military IPO in European History Is Combusting

We did the math.

By: Jenny Ahn, Till Daldrup, Blake Spendley

Editor: Sam Koppelman

Based on Hunterbrook Media’s reporting, Hunterbrook Capital is short $CSG.AS and long a basket of comparable securities at the time of publication. Positions may change at any time. See full disclosures on our website.

In the largest European military IPO in history, Czechoslovak Group (CSG.AS) pitched investors a chance to buy the next Rheinmetall, riding the continent’s recent rearmament boom. Hunterbrook Media’s investigation — drawing from statutory filings, subsidiary accounts, satellite imagery, and a range of other sources — suggests investors bought something very different: an arms-dealer marking up old ammunition, with a critical subsidiary under NATO suspension, production numbers that don’t add up, and a major minority owner with “extraordinary rights” holding a sword of Damocles over the company’s balance sheet.

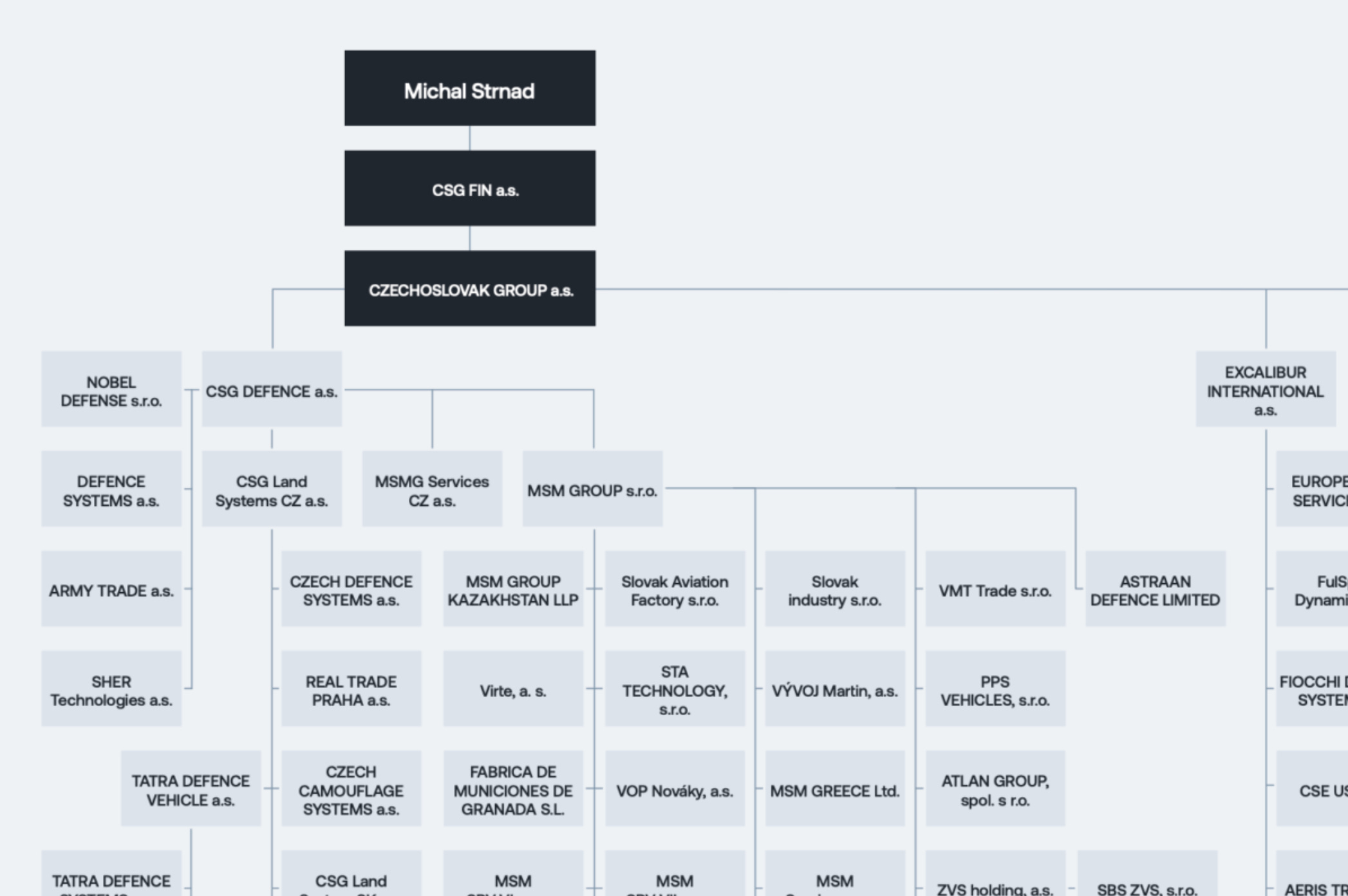

The story began to fall apart almost immediately after the IPO. In January 2026, CSG raised 3.8 billion euros, with BlackRock and Qatar’s sovereign wealth fund anchoring the deal. 33-year-old owner Michal Strnad cashed out 2.55 billion euros. By February, the nonprofit Ján Kuciak Investigative Center reported that the record 58 billion euro Slovak ammunition framework deal — which CSG highlighted as a growth catalyst during the IPO process — had not been formally joined by any of the eight countries Slovakia claimed were interested. A month later, another nonprofit investigative journalism outlet Follow the Money reported that CSG’s Spanish ammunition factory, which produces essential propellant, had been suspended by NATO’s procurement agency over alleged “sanctionable practices.” Then, a month after that: Another outlet, Seznam Zprávy, reported that Petr Kratochvíl — a minority shareholder with “extraordinary” rights over CSG’s most important subsidiary — had exercised a put option days before the IPO and was demanding 1.4 billion euros. None of this was clearly or comprehensively disclosed in the prospectus.

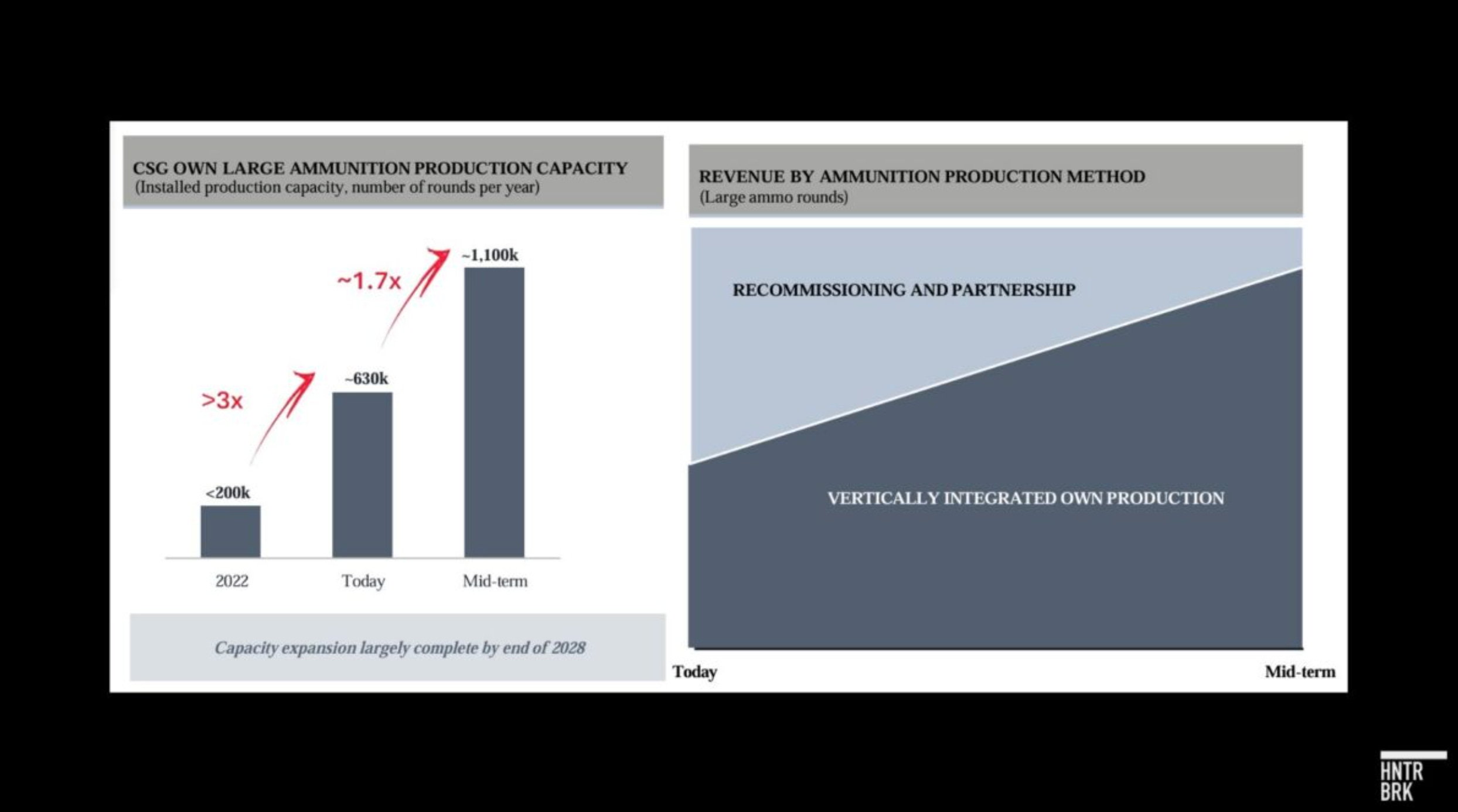

CSG’s prospectus positions it as a rival to Rheinmetall, but Hunterbrook’s analysis suggests the vast majority of its ammunition revenue comes not from making shells but from reselling them. Ammunition was two-thirds of the company’s revenue last year and the primary driver of its guided margin increase. The prospectus claims a current capacity of roughly 630,000 large-caliber rounds a year and says 80% of CSG’s production is 155 mm ammunition, the NATO-standard artillery most in demand. Read together, those two figures suggest CSG is producing roughly half a million 155 mm rounds a year in-house — putting it in the same ballpark as Rheinmetall. But “production” is not the same as “production capacity,” and CSG may be exploiting the ambiguity. When Hunterbrook asked CSG to clarify whether it really could produce around 500,000 155 mm rounds, the company refused to answer — saying it does not disclose capacity by ammunition type.

Hunterbrook’s own reconstruction of CSG’s production footprint points to most of its revenue coming from recommissioning. We could identify only one facility, the Dubnica plant, that appears capable of final assembly of 155 mm rounds; its estimated output last year was between 100,000 and 280,000 rounds. The combined revenue of all four ammunition-producing subsidiaries we identified totaled no more than an estimated 524 million euros in 2024 — roughly a fifth of the 2.5 billion euros CSG reported in medium- and large-caliber ammunition sales that year. The rest likely came from re-selling: acquiring ammunition from third parties, refurbishing it, and reselling it at a markup. CSG has since invested in new production lines — but its total factory upgrades of roughly 205 million euros appear to amount to a fraction of what Rheinmetall has invested in capacity expansion so far.

The reselling model depends on a global stockpile that may be running out. CSG’s founder once described the core trade bluntly: “You buy one warhead for CZK50 and immediately sell it abroad for CZK150 or more.” It’s a good trade — when there is supply. But CSG admits it has “limited visibility” on remaining stock available for recommissioning. A Reuters investigation put the global market of available large-caliber ammunition at roughly two million rounds as of 2024 — a number Ukraine could burn through imminently. And a key pipeline for lucrative ammunition sales — the so-called “Czech ammunition initiative” — may be losing political support and funding. The new pro-Russia Czech prime minister Andrej Babiš, elected last year, is halting the country’s funding for the program, which procures ammunition through intermediaries like CSG. Other key members like Germany, the Netherlands, and Denmark, are also drawing back support. During his campaign, Babiš said “he was uncomfortable with individuals earning excessive profits from the war,” according to the publication Liga. One document obtained by RFE/RL illustrates that point: CSG was selling ammunition to the Czech government at a 28% markup over similar shells a Turkish company was offering. CSG denies profiteering.

The minority shareholder seeking 1.4 billion euros for his stake has veto rights over the entity where much of CSG’s cash and trading activity actually lives. CSG is disputing Petr Kratochvíl’s asking price, offering just a tenth of that, but Kratochvíl, the former head of Excalibur Army, owns 10% of CSG Land Systems — the holding company above EA — and holds extraordinary blocking rights over key corporate decisions. EA reported 2.6 billion euros in revenue — nearly two-thirds of the group’s total — and held roughly 575 million euros in cash in 2024. He also has an 8.9% stake in MSM Group, the ammunition parent. The prospectus did not name Kratochvíl or disclose his exercise of the put option. Asked why, CSG told Hunterbrook that its outside legal counsel confirmed Kratochvíl did not effectively exercise this right. Hunterbrook could not reach Kratochvíl for comment, but he has publicly claimed he exercised the right both digitally and in-person.

Kratochvíl appears to be part of a broader pattern of undisclosed or under-disclosed insiders around CSG’s core subsidiaries and business practices. Before the IPO, CSG transferred 20 to 30 subsidiaries to a vehicle personally owned by Michal Strnad. The IPO described the disposal but did not name Strnad as the recipient. 275 million euros in receivables from those deals remain uncollected. Separately, Excalibur Army disclosed a roughly 4.7 million euro receivable principally from Jaroslav Strnad, the founder and CEO’s father, while also writing off more than 13 million euros worth of time-barred receivables. CSG told Hunterbrook the receivables “will be fully settled in cash” and dismissed the write-off at Excalibur Army as an accounting necessity rather than an actual loss.

Some of the money pooling may be making its way from CSG insiders to political partners: CSG, for instance, appears to pay rent to a former vice-chairman’s real estate company. That former vice-chairman, Miroslav Dorňák, also controls FinGood, a crowdfunding platform that Seznam Zprávy reported paid millions to the law firm of Robert Kaliňák — the Slovak defense minister behind the 58 billion euro ZVS announcement. CSG told Hunterbrook its payments to Dorňák reflect a “standard landlord–tenant relationship.”

CSG’s history makes these post-IPO findings less surprising. Jaroslav Strnad built the company by buying, refurbishing, and reselling liquidated Soviet-era military assets. Czech media have tied early surplus deals to family connections inside the Czech defense ministry. Strnad was a major donor to former President Miloš Zeman, accounting for two-thirds of Zeman’s 2018 campaign donations, according to nonprofit investigative journalism group OCCRP, and other outlets have flagged CSG’s contracts and other deals with the government during Zeman’s tenure as irregular.

Before the Ukraine war, CSG was known for its close ties to Russia and Russian influence networks. JD Vance, now U.S. vice president, wrote to the Treasury Department in 2024 urging the U.S. government to block CSG’s acquisition of Vista Outdoor’s ammunition business, calling CSG “Kremlin-linked” and citing alleged ties to Putin’s inner circle. In its email to Hunterbrook, CSG denied Russian financing allegations and said those relationships ended years ago. But for a company whose valuation rests on selling ammunition to NATO and Ukraine, any residual ties may be meaningful.

CSG’s performance appears to depend on temporary conditions amid little scrutiny: a wartime shortage, a sufficient supply of old ammunition to refurbish, captive procurement channels, and political tolerance for middleman margins. But the old ammunition stock is shrinking. The Czech initiative is facing political and funding pressure. The Slovak framework may never be more than an idea. Key subsidiary FMG is suspended by NATO. CSG barely converted its 2025 profit into operating cash. And the company is surrounded by unnamed shareholders, related-party vehicles, historical patronage networks, and unresolved legal and reputational problems. If the wartime premium fades before CSG becomes the manufacturer it claims already to be, investors may be left not with the next Rheinmetall, but with a levered, opaque defense conglomerate whose core skill was never mass-producing ammunition — it was finding old ammunition, navigating political systems, extracting wartime margins, and keeping the messy parts out of the consolidated story.

In response to Hunterbrook’s questions, CSG denied wrongdoing across all areas of inquiry. CSG confirmed its in-house capacity at “more than 600,000 rounds” of medium- and large-caliber ammunition per year, but declined to break it down by type or facility, citing standard industry practice, even after its own prospectus disclosed that 80% of production was 155 mm. The company called its FMG NATO suspension “a temporary and procedural measure” resulting from an internal NSPA investigation into one of the agency’s officials, and said it has had “no material impact.” On the Kratochvíl put option, CSG said outside counsel confirmed Kratochvíl “did not effectively exercise his right” before the IPO, and that auditors found no liability. CSG described the pre-IPO transfer of subsidiaries to Strnad’s Ytara SPV as “standard” restructuring and said all 275 million euros in receivables “will be fully settled in cash”; asked why Strnad was not named in the prospectus as Ytara’s owner, the company said the information is publicly available in the Czech Commercial Register. On the 58 billion euro Slovak deal, CSG emphasized it is a framework agreement with “maximum potential value, not committed orders,” and said it “is not dependent on any single EU funding mechanism.” CSG confirmed that Marián Goga, who faces criminal charges for bribery in Slovakia, “currently serves on the supervisory board of MSM Group” — a fact the prospectus omitted — and said he “has played a positive role in the development of the business.” In addition to CSG denying any wrongdoing across all areas of inquiry, CSG also repeatedly suggested that Hunterbrook’s questions were based on “incomplete information” or did “not fully reflect the underlying facts,” said the IPO process “involved some of the world’s leading financial institutions and law firms” and that it is “inconceivable that any relevant information would not have been properly disclosed.”

If you know more about CSG, including its potential ties to Russia, please reach out at ideas@hntrbrk.com.

Russia’s invasion of Ukraine may have been the best thing that ever happened to the Czechoslovak Group (CSG).

Before February 2022, CSG was a midsized Czech arms conglomerate. Founded in the mid-1990s as a scrap dealer that refurbished liquidated Soviet-era assets, by the early 2020s, the group had built a small arms empire assembled through aggressive acquisitions of Eastern bloc factories. On the eve of the Russian war on Ukraine, CSG stood at about 580 million euros in revenue with around 3,700 employees.

In just four years, CSG’s reported revenue had increased over tenfold to 6.74 billion euros. The employee headcount nearly quadrupled. CSG was one of the few commercial suppliers in Europe capable of overhauling and delivering Soviet-standard tanks, infantry fighting vehicles, and spare parts that Ukrainian crews were already trained to operate.

More importantly, the invasion gave new life to CSG’s artillery ammunition business. Ukraine was burning through artillery ammunition faster than NATO could produce it, and ramping up production became a top priority for alliance countries.

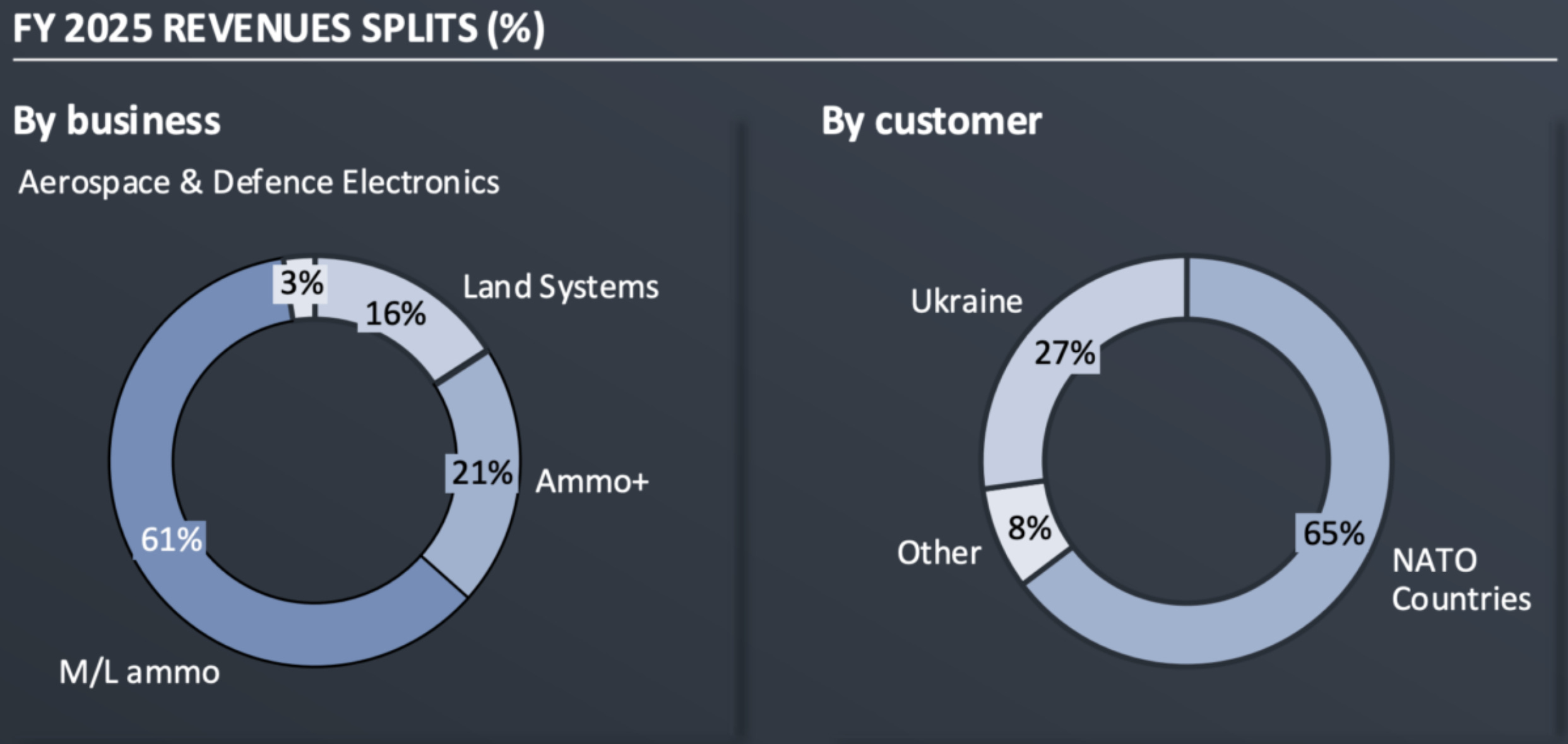

Deliveries to Ukraine hit 42% of sales in 2024, CSG reported. The rest of the sales mainly went to NATO governments scrambling to arm Ukraine and replenish their depleted stockpiles. In 2025, CSG attributed nearly two-thirds of its revenue, or about 4.1 billion euros, to medium- and large-caliber ammunition sales — an extraordinary figure considering Europe’s leading defense supplier, Germany-based Rheinmetall, reported just 3.5 billion euros in revenue for its combined weapons and ammunition segment.

By late 2025, the company was ready to cash in. A syndicate of eight banks — with J.P. Morgan, Morgan Stanley, and Deutsche Bank among the most recognizable names — signed on as coordinators and bookrunners. They produced a 728-page prospectus, approved by the Dutch Authority for the Financial Markets, a financial regulator. BlackRock, Qatar’s sovereign wealth fund, and Artisan Partners each anchored 300 million euros.

Together, these groups shepherded CSG through a 25 billion euro listing on Euronext Amsterdam in January 2026 — the “world’s largest defence IPO ever recorded,” according to the press release. The story resonated: Missed Rheinmetall? Don’t sweat it. There was a new, publicly traded way to get long the militarization of Europe.

Investors piled in — $57 billion in orders, reportedly 14 times oversubscribed. Shares soared 31% on day one. The company raised 3.8 billion euros. Michal Strnad, the 33-year-old who inherited the arms empire from his father, cashed out 2.55 billion euros in the offering, securing his place as the richest man in the Czech Republic.

But within weeks of the listing, a series of revelations began laying bare what the prospectus — and those eight banks — missed.

In February, journalists from Czech outlet the Ján Kuciak Investigative Center revealed that a 58 billion euro ammunition contract with Slovakia — announced weeks before the IPO and cited as a growth catalyst — appeared to be more bark than bite: None of the eight countries Slovakia claimed would participate confirmed plans to join. Another watchdog, Follow the Money, then reported that CSG’s key Spanish ammunition factory had been suspended by NATO’s procurement agency six months before the listing.

Then, another bombshell: Czech investigative news outlet Seznam Zprávy reported that a disgruntled minority shareholder with extraordinary blocking rights had demanded a 1.4 billion euro buyout just days before the IPO.

None of that was clearly or comprehensively disclosed in the prospectus. In fact, CSG apparently considered disclosing the date of Kratochvíl’s request in its March annual report but later deleted it: Seznam Zprávy reported that it had discovered the old language in invisible ink, which CSG claimed was due to a software glitch. (Side note: In 2024, CSG CEO Strnad pressured the owner of Seznam to sell his media business — threatening “ruinous fines” from Czech authorities if he didn’t comply, according to Czech news outlet Respekt.1)

Notably, the date that CSG considered adding was January 24, 2026, four days after Kratochvíl claims he exercised his right. The difference matters a lot: The IPO was on January 23, meaning CSG still had time to disclose Kratochvíl’s put option to investors — but chose not to do so. In a comment, CSG says this was because Kratochvíl exercised the option improperly.

Hunterbrook Media’s investigation — based on a review of subsidiary filings across the Czech Republic, Slovakia, and Spain buried in CSG’s consolidated numbers — suggests the prospectus omissions go well beyond what’s already surfaced. What we found challenges not just CSG’s governance but its fundamental business model.

Underneath the prospectus calling CSG “a leading defence group” and “a top two European player” in ammunition, and the press releases touting “state-of-the-art” filling lines and “one of the most modern workplaces within Europe,” we found a hodgepodge of Soviet-era factories, a history of political patronage, and widespread reselling of old ammunition.

CSG admits in its prospectus that a portion of its ammunition production comes from “recommissioning” — lower quality ammunition like expired inventory it acquires, upgrades, and returns to the field. It doesn’t explain, however, what proportion of its total sales come from this approach. Hunterbrook’s investigation suggests it has been the vast majority, with CSG’s in-house manufacturing capacity responsible for a fraction of total output. CSG calls recommissioning a “nimble and entrepreneurial” approach — but later admits “limited visibility” on the global stock of ammunition to be resold.

CSG has promised to lessen its reliance on outside supply by vertically integrating the ammunition supply chain, with a goal of achieving production of 1.1 million large-caliber rounds by 2028, putting the upstart ammo dealer on a par with Rheinmetall’s multibillion euro production machine. But the gap between that promise and today’s reality is vast, our findings show — and it likely requires significantly more investment than CSG has made so far.

It’s an investment CSG may not have the cash to embark on: While CSG reported 1.6 billion euros in operating profit in 2025, it converted just 3.8% of that to operating cash flow. And the company sat on 3 billion euros in net debt as of the end of last year — nearly twice its operating profit.

CSG appears to be trying to obscure these facts by adorning its growth narrative with big promises and flashy announcements — while important details about its business are left out of the public record. But the numbers exist, across primary source and subsidiary-level documents, and they reveal a central insight: CSG is still running its business like a post-Soviet era conglomerate in the shadow-world of Eastern European defense markets, where it could brush off public scrutiny over questionable practices.

Hunterbrook found other examples of questionable ways CSG is still doing business — from cash disappearing into Strnad’s orbits, to a former minority shareholder and key operator of the company now facing criminal charges for corruption. None of these are in the prospectus or in the annual consolidated statements.

But CSG is now a publicly listed company on a global exchange, backed by some of the world’s biggest investment funds and with obligations to public shareholders. The practices that built the empire will face a very different level of scrutiny from regulators, investors, and journalists than the company may have grown accustomed to.

Hunterbrook is committed to providing that scrutiny. The following represents just some of what we have found in a matter of months. The reporting continues. Reach out at ideas@hntrbrk.com if you know more.

Can CSG Actually Make the Shells It Is Promising?

It would be the biggest deal in CSG’s history. And it was disclosed in December 2025, just weeks before the company’s IPO.

The announcement: ZVS Holding, a 50/50 joint venture between CSG and the Slovak government, had signed a contract with Slovakia’s defense ministry to provide up to 58 billion euros worth of medium- and large-caliber ammunition over the next seven years. The deal is not a firm purchase order but a framework agreement, meaning it sets the terms under which orders could be placed.

Slovakia, which is undergoing budget cuts in order to save 2.7 billion euros, assured the public that the deal wasn’t just for them. Slovak Defense Minister Robert Kaliňák claimed eight countries wanted to join: Croatia, Greece, Romania, Italy, Poland, the Czech Republic, Belgium, and the Netherlands. “We assume that specific contracts will be concluded within two to three months, and deliveries will start next year,” Kaliňák said in an interview with Slovak newspaper Pravda in December 2025.

It turned out the announcement may have been more hype than substance. None of the countries Kaliňák said would join the deal actually confirmed any intention to join. Slovak investigative news outlet ICJK, in cooperation with other journalists, contacted every named country, and while one indicated the proposal was still under consideration, others were outright dismissive of Kaliňák’s claims. “This is not currently relevant for the Netherlands,” the country told ICJK. CSG’s home country of the Czech Republic went a step further, blocking any consideration of the deal after determining it was akin to a no-bid contract, ICJK reported.

The participation of other countries is crucial for Slovakia to get special 1% financing through the EU’s flagship 150 billion euro Security Action for Europe program, which is possible only if at least two members participate. The exemption allowing single-country participation expires at the end of May 2026. If Kaliňák doesn’t secure a partner by then, low-cost EU financing for the ammunition purchases may become harder.

In an email to Hunterbrook, CSG emphasized the deal is a framework agreement with a “maximum potential value, not committed orders,” and that the deal is not dependent on any single EU funding mechanism. The company added, “serious discussions are ongoing with several potential customers” but declined to name them, citing commercial confidentiality.

But the eye-popping 58 billion euro figure drew attention to a more fundamental question: Even if the contract does convert, is CSG physically able to make the shells it’s promising?

CSG told Bloomberg in an email that the figure “reflects the maximum potential volume of deliveries over the seven-year period,” estimated based on the “total value of available production capacity.” Kaliňák vouched for the company’s ability to deliver on the deal, adding that the deal is based on what can be produced in three shifts. The company recently inaugurated a new filling line at its Dubnica nad Váhom plant that it claimed would help fulfill the Slovak deal and reach its production target of a million large-caliber rounds per year.

But CSG and ZVS allegedly dodged questions from the ICJK about the exact production capacities, citing “security and competition reasons.” (In contrast, Rheinmetall, CSG’s larger competitor, has been more explicit about its current and projected production capacity and timeline. See its March 2026 Investor Presentation, page 34, and its 2025 Annual Report, page 51)

Ambiguity grew when CSG announced that “operating conditions allow for a two-shift mode” at the newly updated plant — seemingly at odds with Kaliňák’s comment that the target production is achievable through a three-shift operation. A defense ministry spokesperson responded to an ICJK question on the discrepancy by accusing the outlet of having “fundamentally incorrect information” as before, and offering a vague rebuttal: “crucial components can also be produced in three-shift operation.”

Even with three shifts, however, it’s unclear CSG could produce anything close to 58 billion euros worth of ammunition.

In fact, it’s unclear how much CSG is producing at all. Or what proportion of CSG’s claimed 4.1 billion euros in revenue from M/L ammunition sales is coming from real in-house manufacturing.

Beyond the 58 billion deal, medium- and large-caliber ammunition is central to the group’s growth thesis, with the company arguing demand will continue to climb even after the war in Ukraine ends, driven by NATO’s stockpile refill requirements. It was the group’s “largest revenue driver,” contributing 61% of total revenues in 2025, according to the company. CSG reported a nearly 7 billion euro backlog on M/L caliber ammunition sales last year (and 15 billion euros across all segments), with an additional 27 billion euros in the pipeline for the whole group — including about 1 billion euros from the recent Slovak deal.

Hunterbrook’s investigation, however, raises fundamental questions about CSG’s production capacity — and how much the company can actually cash in on this opportunity.

Demystifying CSG’s Ammunition Production Scale

To start, it’s very hard to even understand precisely what CSG is claiming regarding its capacity to produce ammunition.

In one place in the prospectus, CSG says it can make 630,000 rounds; in another, 550,000 rounds. In an email to Hunterbrook, CSG affirmed it had “more than 600,000” of capacity.

More confusing is what those numbers represent.

In some places, including page 109 of its prospectus, CSG says this total refers just to large-caliber ammunition. In its email to Hunterbrook, CSG said it covered both medium- and large-caliber ammunition, but also, in that same email, CSG’s spokesperson directed Hunterbrook to look at page 109.

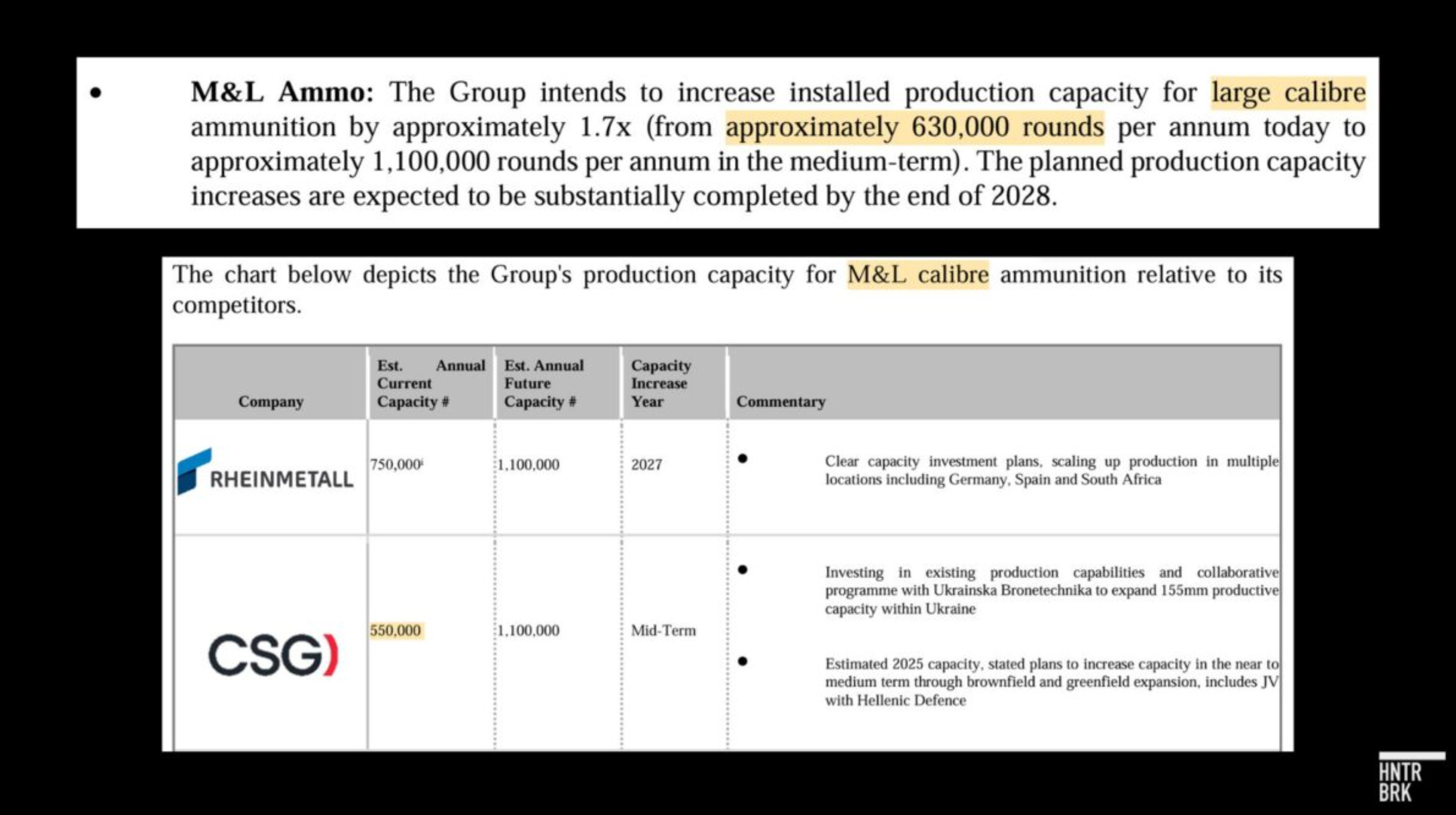

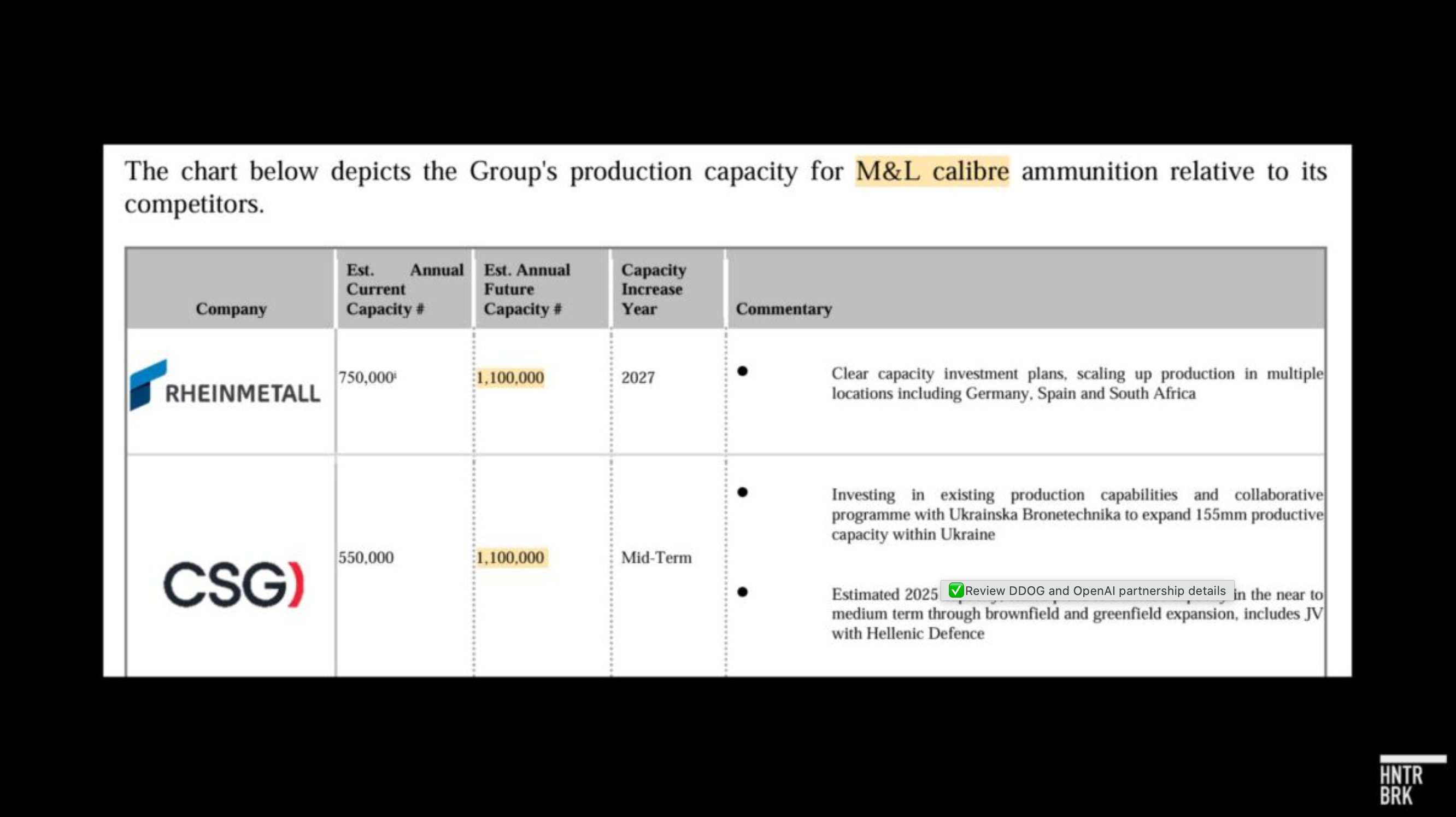

On page 109 of the prospectus, CSG also says it plans to increase its production to 1.1 million large-caliber munitions, substantially, by the end of 2028. If true, those figures would put it on a par with its much larger peer Rheinmetall, whose current production capacity and near-term goals are just slightly ahead of CSG’s.

The apparent discrepancy in CSG’s numbers may be small, but the precise definition of what these numbers represent is critical. 630,000 large-caliber rounds is a very different proposition than 550,000 medium- and large-caliber rounds combined — if you’re trying to understand CSG’s true ammunition production capacity.

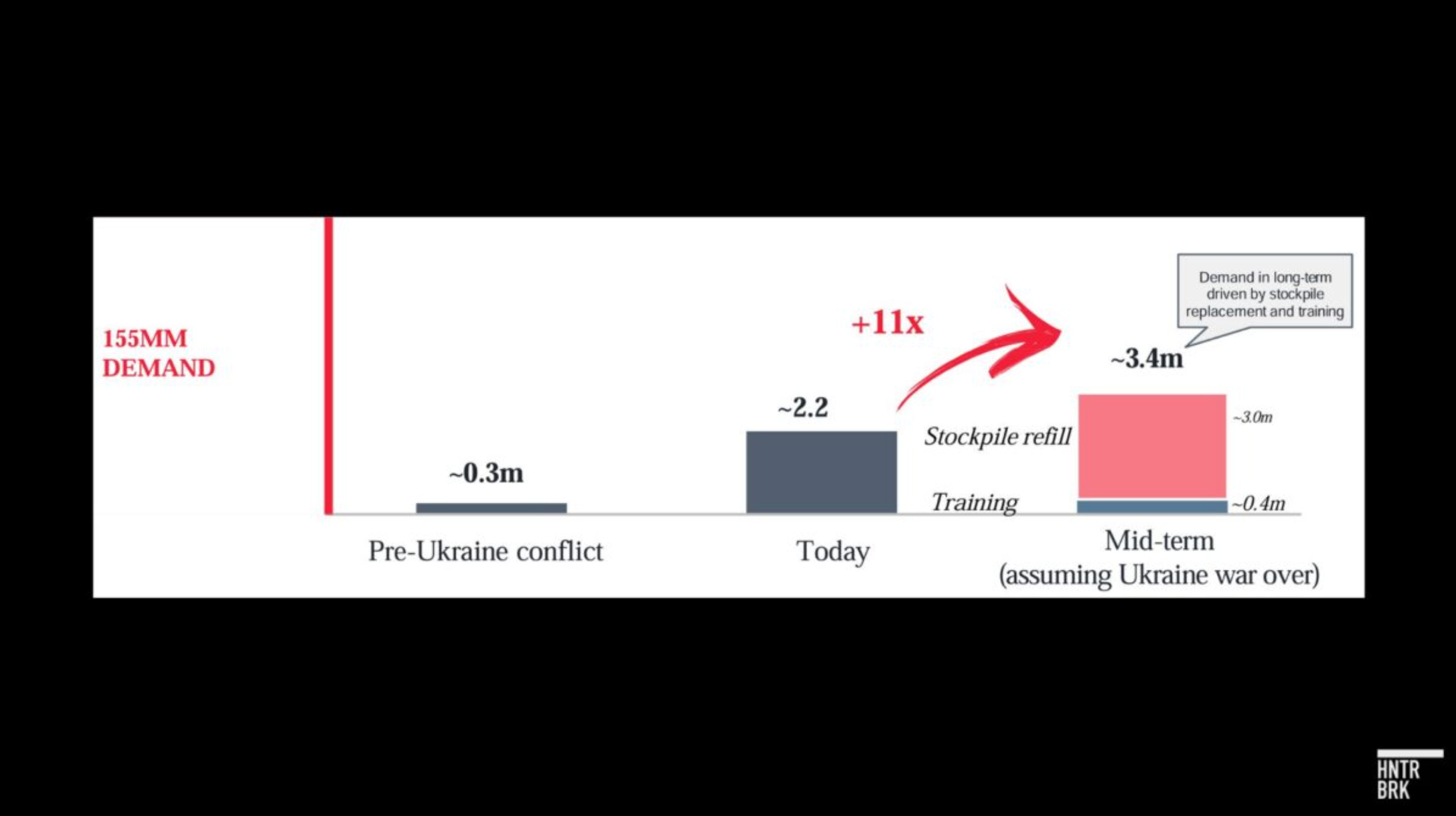

Large-caliber rounds, especially 155 mm artillery rounds, are responsible for much of the company’s narrative; they’re the workhorse of Ukraine’s fight against Russia, the NATO-standard artillery in most critical need; and a big reason Rheinmetall saw its stock price increase more than 20 times after the invasion. An investigation by a consortium of journalists in 2024 put the total Western European artillery output at just 500,000 to 600,000 rounds per year — a fraction of Ukraine’s burn rate of about 2.4 million and the EU’s stated 2 million target. (Watch this YouTube video by The Wall Street Journal on the 155 mm ammunition shortage.)

155 mm rounds appear to go for anywhere between 3,000 and 8,000 euros apiece, reflecting a significant wartime premium; medium-caliber rounds are priced in the low hundreds.2 So the lion’s share of CSG’s revenue, very plausibly, comes from the sale of large-caliber rounds.

And a reader of the prospectus could be forgiven for thinking CSG makes around half a million 155 mm rounds per year — since the company says that 80% of its M/L production is 155 mm; and its total production capacity is around 600,000.

This is an impressive-sounding claim that, if true, makes CSG’s manufacturing footprint almost comparable to Rheinmetall’s.

But that’s far from clear.

Hunterbrook took three approaches to stress-test these claims. In none of them could we find evidence that CSG is producing anything close to the number of 155 mm rounds Rheinmetall is producing in-house.

And all of the approaches raised more questions than answers as to how to explain the roughly 4.1 billion euros CSG reported in M/L ammunition revenue in 2025.

Now, a caveat: Military production can be obfuscated. And we may have missed something — say, a secret, underground propellant manufacturer. Our calculations could also be wrong, and if you have better ideas for how to back into these numbers, please write us at ideas@hntrbrk.com.

But based on what is publicly available, CSG’s in-house production numbers, alone, cannot come close to explaining its rapidly growing revenue.

Method 1: Matching CSG’s Capacity Claim With On-the-Ground Realities

The idea here is to test CSG’s production claims by actually looking at CSG’s production capacity on the ground.

The prospectus makes two key claims: CSG has capacity for roughly 630,000 large-caliber rounds a year, and 80% of its M/L ammunition production is 155 mm. Read together, an investor might naturally conclude CSG is producing roughly half a million 155 mm rounds a year in-house. Eighty percent of 630,000 is 504,000.

But there’s a critical distinction buried in the language. The 630,000 figure refers to “capacity.” The 80% figure refers to “production.” Those aren’t the same thing. If CSG is running below full capacity, actual 155 mm output could be far lower than investors might assume.

Or, CSG might be counting production of components, say shell bodies, rather than fully-assembled rounds, as part of overall production capacity. The spokesperson said in CSG’s email to Hunterbrook that the term “in-house production capacity” is meant to refer “to the Group’s ability not only to carry out final assembly of large-calibre ammunition, but also to manufacture a substantial portion of its key components within the CSG industrial network.3”

CSG appears to be aware of the ambiguity: When Hunterbrook asked the company to confirm whether it can produce around half a million rounds of 155 mm per year, CSG refused, saying it does “not disclose detailed production capacity by specific ammunition types” and that “production capacity is not a fixed or single-dimensional metric.”

The refusal is notable given that CSG’s own prospectus disclosed both figures that produce that math.

So the question is, does CSG have the manufacturing footprint to produce anything close to half a million rounds of 155 mm ammunition in-house?

CSG doesn’t clearly disclose exactly which of its factories make ammunition, much less break down the full quantity by type of ammunition. And as mentioned, information across CSG’s various public statements — press releases, websites, and company disclosures to investors — is often contradictory, sometimes even across pages in the same report.

For example, in the prospectus, the company says there are 14 ammunition factories on one page (page 95), then says there are 12 on another (page 99).

But in the sustainability section of the 2025 annual report, where the company is legally required under EU laws to describe its sector and operations, including aspects of its value chain (pages 124–126), Hunterbrook counted only seven operating entities described as involved in manufacturing ammunition.4 Of those, three don’t seem to make fully assembled artillery ammunition, but rather components for ammunition — like shell casings or explosives — or only make ammunition for small firearms.5

That seemingly leaves only four factories that actually make finished M/L ammunition: the Dubnica factory that CSG co-owns with the Slovak defense ministry; VOP Nováky, a longstanding CSG ammunition factory in Slovakia; Fábrica de Municiones de Granada (FMG), a 700-year-old ammunition factory in Spain, acquired in 2020; and ZVI a.s., a Czech ammunition factory that CSG recently purchased.6

Of those four, Dubnica appears to be the only CSG facility the company has described as capable of producing fully assembled 155 mm rounds. CSG’s three other ammunition-producing plants do not seem to mention such capability: CSG’s website mentions the VOP Nováky plant making tank and mortar rounds, rockets, and ammunition components. It also says it’s involved in the “life cycle extension of ammunition of 57-155 mm calibre” — i.e. refurbishing; an ICJK investigation in 2024 said VOP Nováky only makes 155 mm training rounds, effectively meaning rounds with no explosives.

As for FMG, an article on its website dated November 2025 describes its main production as tank ammunition. It also mentions making mortar ammunition, as well as propellants and explosives — components needed for 155 mm artillery ammunition. The article doesn’t mention making 155 mm ammunition itself. ZVI only makes medium-caliber ammunition.

CSG finished upgrades at Dubnica in late 2025 that it says will allow the factory to produce up to 280,000 rounds in 2026. In 2025, however, total output at Dubnica was likely around 100,000 rounds per year, according to ICJK.

That suggests CSG’s in-house production capacity for 155 mm rounds at Dubnica is somewhere between 100,000 and 280,000.

That’s nowhere close to the half a million rounds investors might infer from the prospectus.

To be sure, in its email to Hunterbrook, CSG denied that Dubnica is the only location where “final assembly of 155mm ammunition takes place,” but declined to identify the other facilities, citing commercial and security reasons. CSG also explained that large-caliber ammunition is a “complex system,” and therefore, it “would not be accurate to attribute production of 155mm ammunition to a single site.”

Which raises another question: Does CSG include “recommissioning” in its production numbers?

CSG explains in its prospectus that one of its methods for producing ammunition is what it calls “recommissioning”: “The Group acquires lower quality large caliber ammunition from NATO member armies (such as expired inventory) and then inspects, upgrades and reassembles inventory for return to the field,” CSG writes.

Just how much recommissioning CSG does — relative to in-house production — is the key question, one the company did not answer directly in response to Hunterbrook’s questions. So we tried to figure it out.

Method 2: Subsidiary Revenue Analysis

To answer that question, Hunterbrook looked at the revenue reported by each of the subsidiaries that we identified as making ammunition to their respective state registries in the Czech Republic, Slovakia, and Spain. The idea is straightforward: If CSG is really manufacturing most of its ammunition in-house, the factories doing the manufacturing should be reporting revenue that, in aggregate, accounts for the bulk of the group’s ammunition sales, after accounting for the margin on final sale.

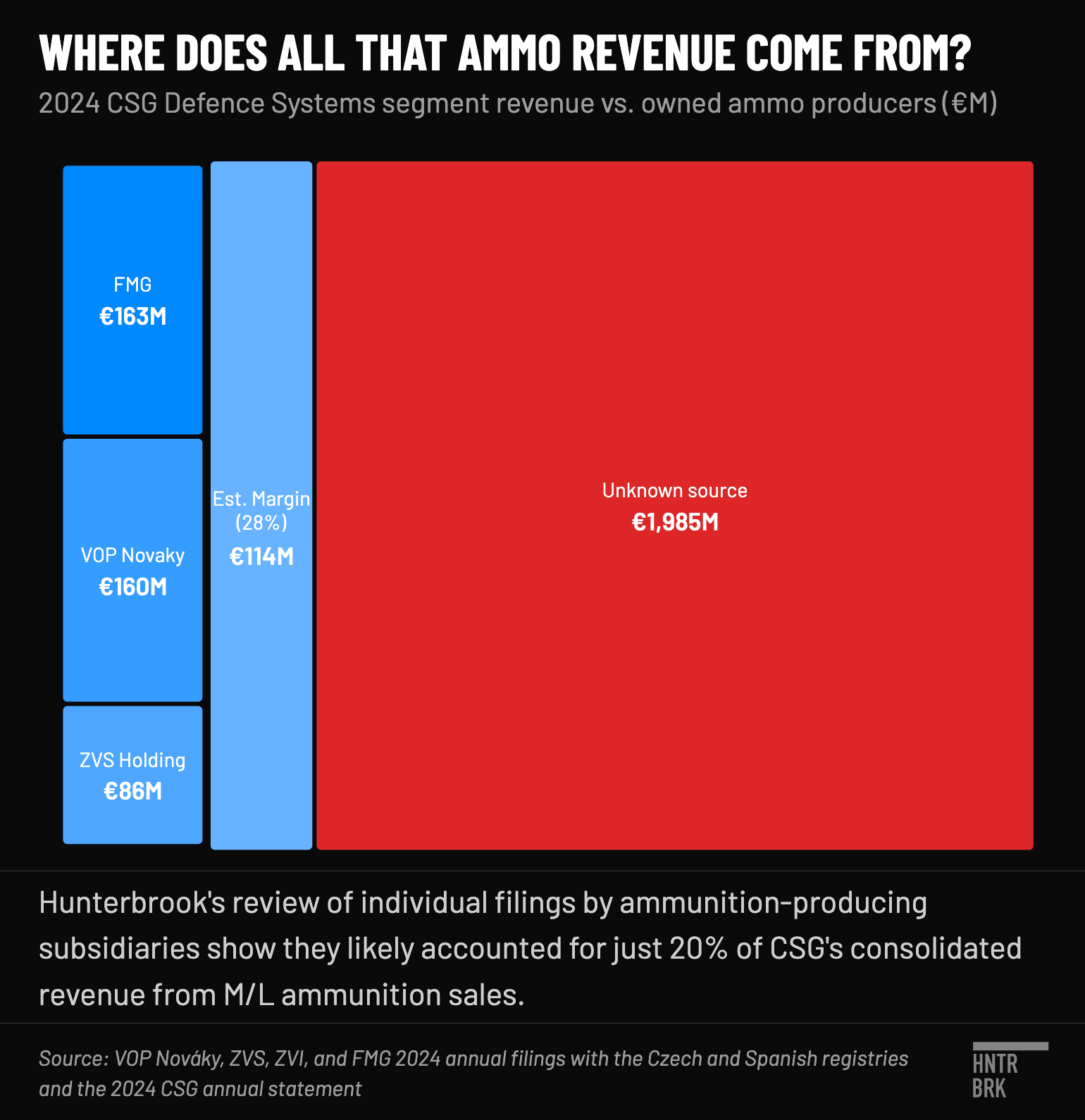

In its 2024 filing with the Czech registry — the latest available — ZVS reported 119 million euros in revenue, of which 85 million euros were likely from in-house production; the rest was labeled as revenue from goods resold or services. VOP Nováky reported 260 million euros in revenue in 2024, of which about 160 million euros were likely from in-house production. FMG reported 163 million euros in revenue. A portion of that is revenue from components of ammunition, like propellant charges, rather than finished ammunition, but FMG did not break out the revenue by these subitems.

ZVI’s filings with the Czech registry showed it was a loss-making company with 37 employees and revenue of less than half a million euros in 2024. CSG provided a pro forma table showing what the revenues would have looked like if the acquisition had occurred at the beginning of the reporting period, which shows just 15 million euros from several acquisitions clumped together, including ZVI — suggesting CSG’s expected revenue from ZVI in 2026 was a fraction of 15 million euros.7

In total, the combined revenue in 2024 reported by ZVS, VOP Nováky, ZVI, and FMG — net of revenue from components, services, or resold goods where those figures were reported — was no more than 409 million euros, according to a Hunterbrook analysis.

Now, CSG is a complex group with extensive intragroup sales: Factories don’t always sell directly to end customers. Instead, they sometimes sell to trading entities like Excalibur Army, which then resells to governments and militaries at the final market price. That means the revenue reported by the manufacturing subsidiaries may understate the consolidated revenue that in-house production ultimately generates — because the markup to the end customer is booked at the trading entity, not the factory.

To account for that, Hunterbrook applied the estimated 28% operating EBIT margin for the Defence Systems division — a generous assumption in some ways, since it ignores that some factories do sell directly to end customers and their revenue almost certainly already reflects those margins.8 After that addition, you get about 524 million euros for the estimated total revenue in 2024 from ammunition made by its factories. That’s roughly a fifth of the total M/L ammunition revenue of 2.5 billion euros reported by the company for 2024.

Hunterbrook used revenue data from 2024, because that’s the latest year for which subsidiary files were available from the Czech business registry.

Meaning, roughly 80% of CSG’s total ammunition revenue the company reported in 2024 seemingly can’t be accounted for by in-house production, and therefore likely came from third-party sources, according to Hunterbrook’s analysis.

CSG has since made meaningful progress to expand its in-house production capacity, including a new 155 mm filling line at Dubnica that was inaugurated in December 2025. Which brings us to the question: Just how much new capacity could CSG have brought online?

Method 3: Comparing CSG to Rheinmetall’s Manufacturing Footprint

This approach is premised on the assumption that if CSG can really produce around as much ammunition as Rheinmetall, then its investment in its manufacturing capacity should also roughly mirror Rheinmetall’s.

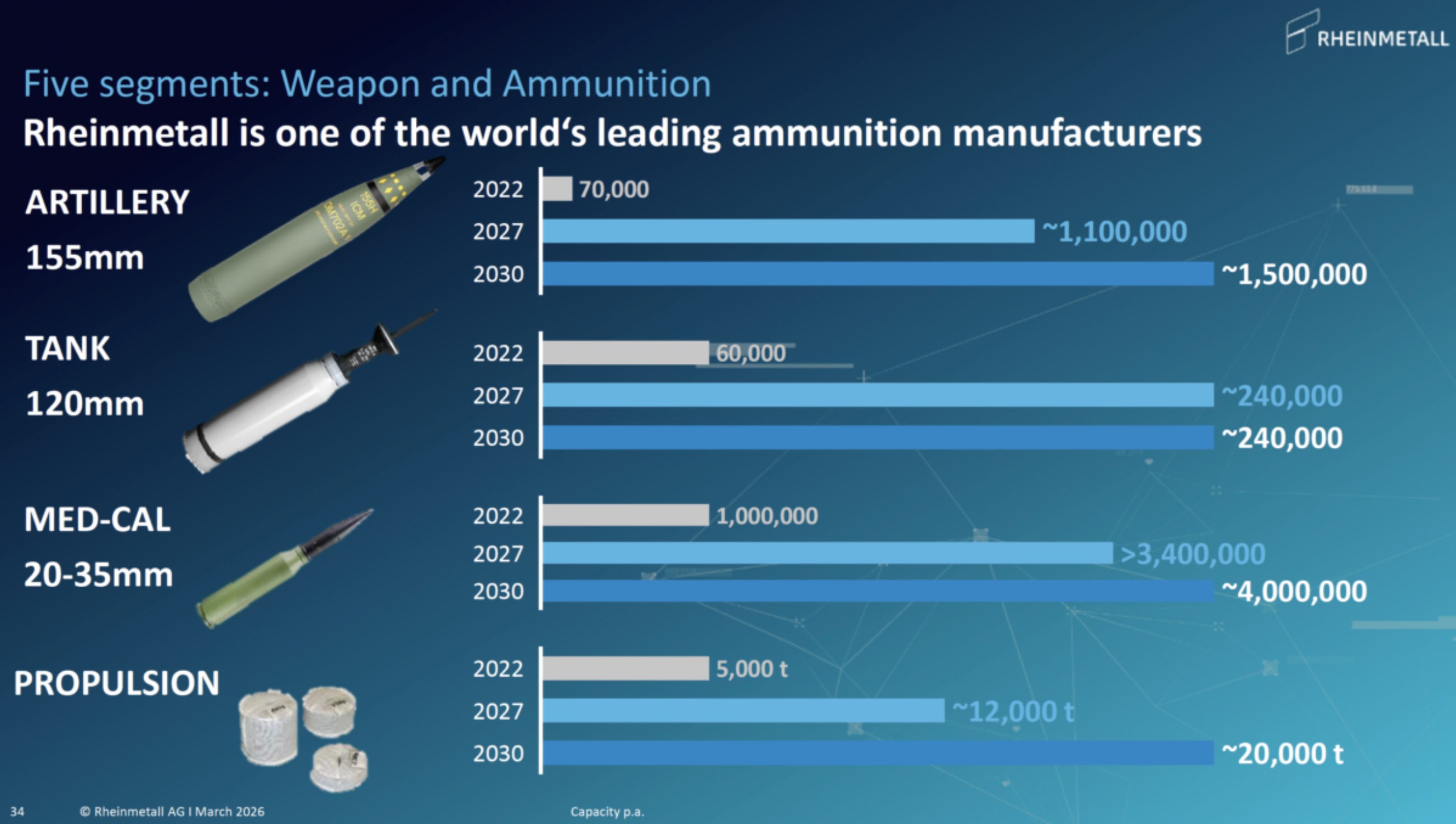

CSG appears like it actually had a bit of a head start. CSG said it could make less than 200,000 rounds a year in 2022; Rheinmetall says its numbers were about 130,000 (based on the company’s chart showing 70,000 155 mm rounds and 60,000 tank rounds).

Across the four existing CSG ammunition-producing plants Hunterbrook identified, CSG has since reported the completion of improvements costing a total of around 205 million euros: installing a new filling line and a new shell line at its ZVS plants, and improving automation at VOP Nováky. In 2024, CSG’s Defence division CEO mentioned “big plans” for significant investments in FMG, but it’s unclear what the improvements were or how much it would cost. CSG has also announced plans to invest in “extensive modernization and expansion of ZVI’s production.” But details on the plan are unclear.

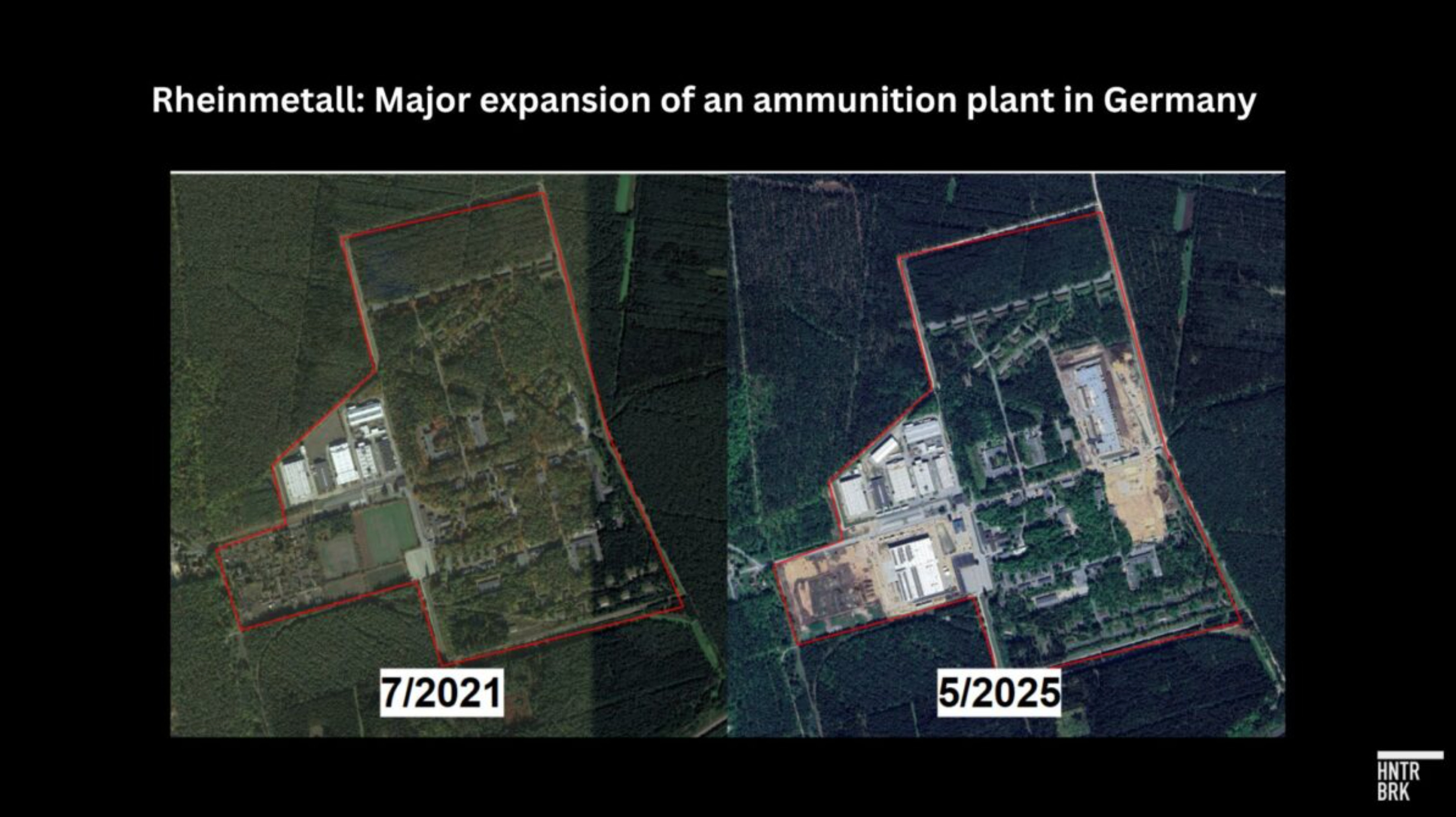

Compare that to the nearly 500 million euros Rheinmetall spent on a greenfield ammunition plant in Germany completed last year alone, which is expected to make 350,000 155 mm shells per year by 2027 after a full ramp-up.

That’s one site. Rheinmetall also runs a Spanish firm it acquired for 1.2 billion euros in 2023, which analysts say added roughly 300,000 rounds per year. Then there is an additional retrofitted Berlin auto plant where more than 200 workers have been shifted from automotive pumps to forging 155 mm casings — plus new plants under construction in Romania, projects in Lithuania and the U.K., and expanded capacity in Hungary, South Africa, and Australia.

CSG and Rheinmetall are targeting similar production ramp-ups on similar timelines: In its prospectus, CSG compares its target to “substantially” achieve 1.1 million medium- and large-caliber production by the end of 2028 with Rheinmetall’s target to reach the same goal by 2027. But again, CSG appears to be blurring important facts.

Reading the fine print, CSG seems to be comparing its own 1.1 million medium- and large-caliber ammunition target with Rheinmetall’s 1.1 million 155 mm-specific target. According to Rheinmetall’s disclosures, the company is actually targeting around a total of 4.5 million rounds, including medium- and other large-caliber ammunition.

Moreover, CSG hasn’t explained exactly where the ammunition is currently coming from, or how or when it plans to nearly double production. When asked, CSG argued: “We do not disclose detailed production capacity by specific ammunition types. This is standard practice in the defence industry, and such granular data is not publicly provided by manufacturers.”

Instead, CSG offers a chart without precise labels, scale, or timeline details to suggest roughly half of its revenue is in-house currently, a number that will presumably grow to become the vast majority of revenue by an unspecified “mid-term” time horizon.

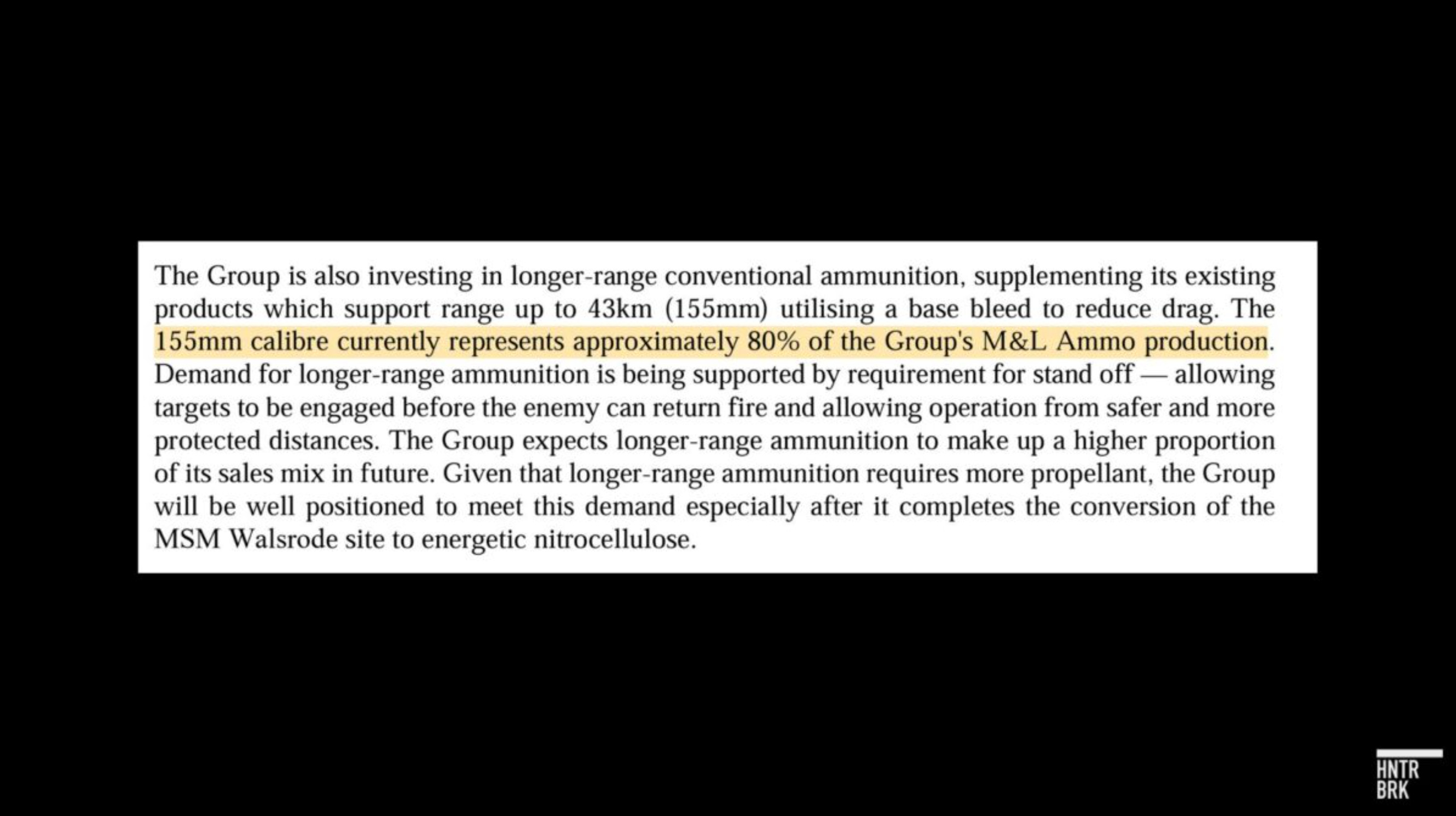

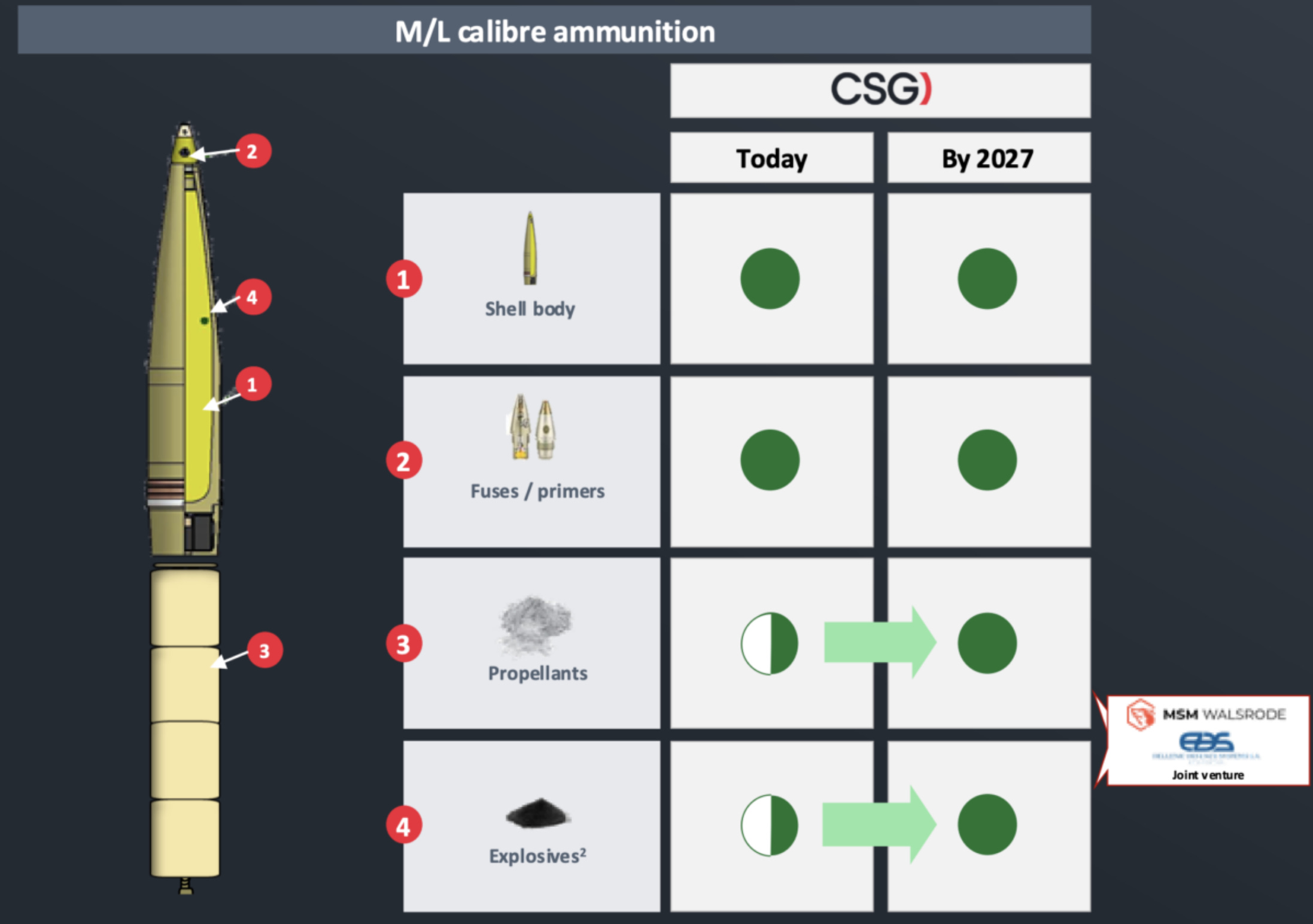

Achieving full in-house production requires vertically integrating manufacturing capacities for each of the components of a round. A complete 155 mm artillery round has four main components: the shell body, the explosive fill (typically TNT), a fuse, and a propellant charge; the propellant charge often relies on nitrocellulose as a precursor.

Of the components, TNT and propellants are the most constrained input in European ammunition manufacturing, according to industry experts. Rheinmetall’s CEO has repeatedly called propellant production “a strategic bottleneck” in the defense industry. CSG itself has acknowledged this, saying “the availability of such propellant charge systems is currently one of the main limiting factors in increasing artillery ammunition production capacity in Europe.”

Both companies have publicly committed to addressing the propellant and explosives bottlenecks by bringing the capabilities in house. CSG is guiding to flat margins this year, but increased margins in the midterm as the “benefits of vertical integration and production capacity-ramp up” kick in.

In March, CSG announced plans to invest 300 million euros in a joint venture with European propellant manufacturer Eurenco to build a new propellant plant in Slovakia. It also purchased a nitrocellulose plant in Walsrode, Germany, last year, as part of a 141 million euro acquisition9 and invested 50 million euros in a joint venture in Greece to restart TNT production.10

But again, the scale of CSG’s investment pales in comparison to its competitor, Rheinmetall. Rheinmetall announced in November that it is planning to invest 535 million euros in building a new nitrocellulose plant in Romania — nearly four times what CSG spent on Walsrode. Rheinmetall already has four other nitrocellulose sites globally. Its German plant is supposed to produce the full value chain, according to a 2024 press release — from projectile and fuse to explosive charge and propellant charge.

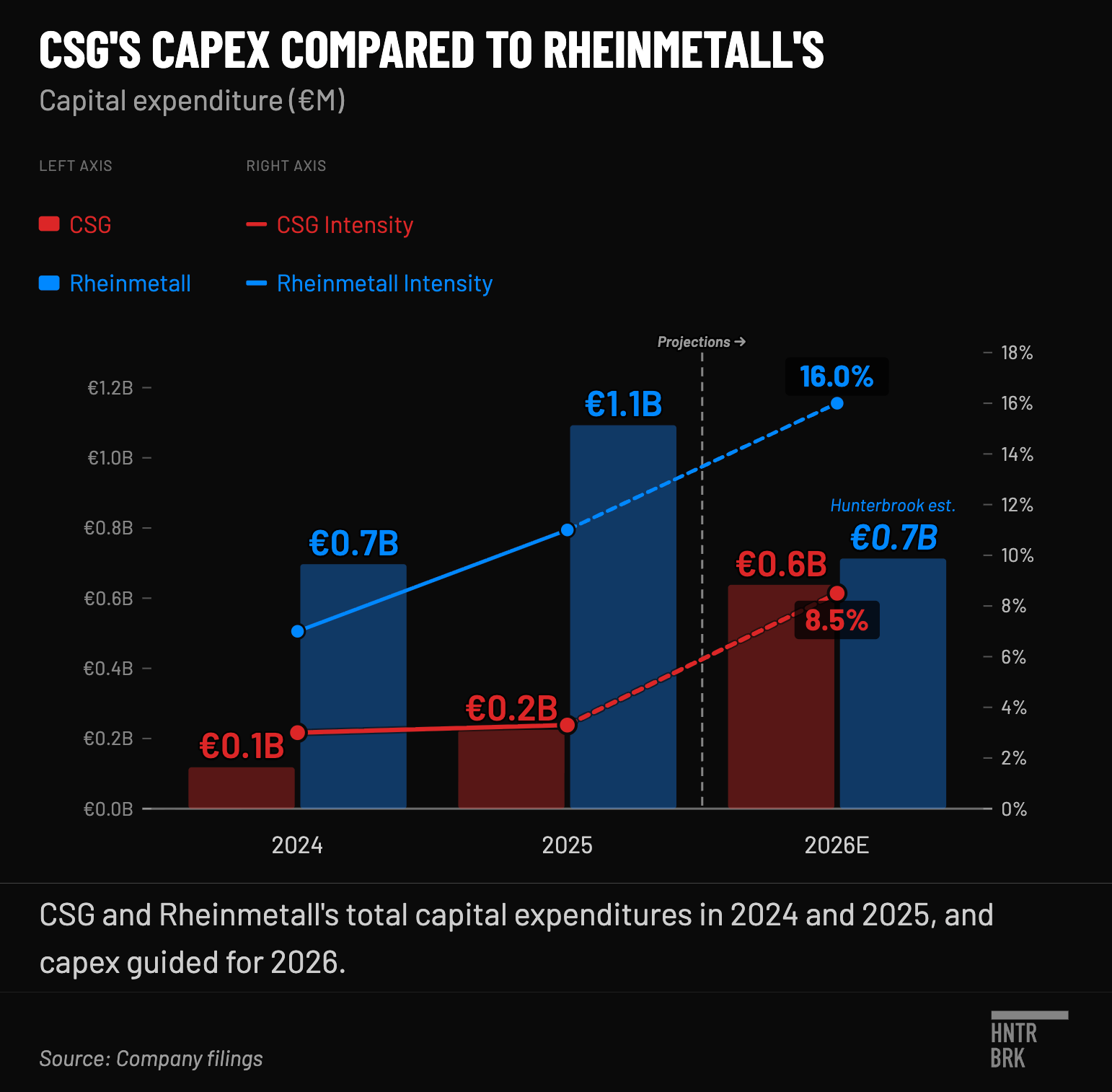

CSG and Rheinmetall’s total capital expenditures in 2024 and 2025 also reflect that gap, with Rheinmetall’s capex at nearly four times CSG’s in 2025. CSG appears to be gearing up to play catch-up, guiding to nearly triple the 2025 capex intensity in the next year.

To be clear, capex comparisons are imperfect. Rheinmetall’s higher spending might reflect predominantly other segments, as well as variables like the relatively high cost of Western European labor compared to Eastern European labor (as CSG pointed out in its comment to Hunterbrook). In other words, CSG could theoretically be getting more output per euro of investment, and it certainly could have benefited from the head start of inheriting Soviet-era factories.

But the gap — between CSG’s 205 million euros in total upgrades across four plants, plus a nitrocellulose acquisition and two joint ventures not yet operational, and Rheinmetall’s investments of billions of euros so far to expand ammunition production — implies it would be hard for CSG to catch up.

And while CSG does plan to increase capex massively, it would be with cash that CSG may not have.

In 2025, the company reported just 61 million euros in operating cash flow, despite 1.6 billion euros in operating EBIT — a 3.8% conversion rate. The entire cash from operating profit was wiped out by its working capital totaling 1.6 billion euros, up to 24% of revenue from 13% the year before. The company said it “deliberately” increased the working capital to fulfill “record order backlogs amid tight supply chain constraints and strong order inflows.”

That means, unless CSG can manage to materially reduce its working capital, funding a 638 million euro capex will almost certainly require outside capital or massive upfront payments; CSG’s debt already stood at 3 billion euros as of the end of 2025 — nearly double from the prior year. CSG said it expects working capital will stabilize in 2026, even as it highlights a 36% increase in backlog. For comparison, Rheinmetall reported a 66% cash conversion rate in 2025, and guided to at least 40% in 2026.

So, we’re back to our original question. How do we explain the gap between our estimated production revenue for CSG and CSG’s claimed 4.1 billion euros in M/L ammunition sales? Markups beyond the 27% EBITDA of the segment or non-production-related revenue like servicing can only explain a portion of that. The rest is likely coming from recommissioning.

The Big Business: “Buy a Warhead for CZK50… Sell It Abroad for CZK150“

“You buy one warhead for CZK50 and immediately sell it abroad for CZK150 or more,” Jaroslav Strnad explained to news outlet Respekt in 2018. It’s a good pitch!

Recommissioning can indeed be a profitable business; after all, it’s CSG’s founding trade — sourcing from depleted Eastern European stockpiles, refurbishing, and reselling at a markup.

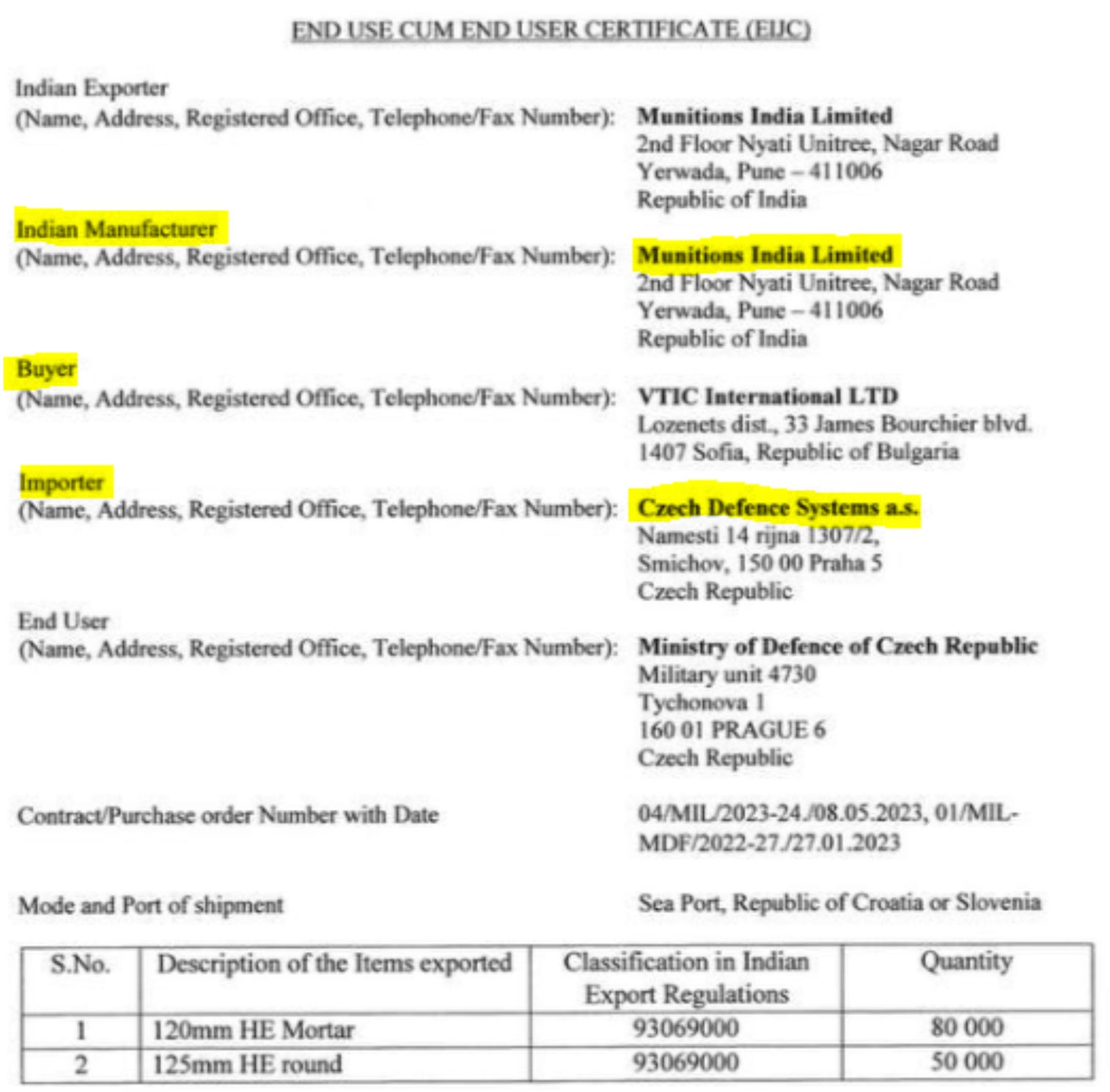

Spain’s transportation minister Óscar Puente posted a document on X showing one example of CSG operating as a middleman for the importation of ammunition from India.

The problem is, there is a finite supply of ammunition to be resold. CSG described the recommissioning method in its prospectus as a “nimble and entrepreneurial approach” that allowed the company to meet urgent demand from the Ukraine war. But it also admitted there is “limited visibility on the remaining stocks of large-caliber ammunition for recommissioning available in the market in the medium-term.”

Countries like the U.S., South Korea, and India, which in the past have supplied 155 mm ammunition to NATO, are facing constraints: The U.S. is woefully behind its replenishment targets, with production ramp-up at less than half its target as of last year. South Korea cannot spare any more 155 mm shells without “risking shortages” given the North Korea threat, the Center for Strategic & International Studies wrote in 2024. India is scaling up production, but the Indian defense ministry was reportedly considering a ban on 155 mm shell exports due to escalating tension with Pakistan as of last year.

A 2024 Reuters investigation cited “a senior Czech official” putting the available global stock of large-caliber ammunition at 2 million rounds — which a research study from that year suggested would not last more than a couple of years.

And sourcing inputs from the outside is inherently risky. In May 2024, CSG CEO Michal Strnad acknowledged publicly that roughly half the components his company was purchasing from suppliers in Africa and Asia were not of sufficient quality to ship directly to Ukraine. “Every week the price is going up and there are big issues with the components,” he told the Financial Times.

An alarming complaint about quality reportedly arrived in the form of a letter from the Ukrainian to the Czech government, the German business newspaper Handelsblatt reported in 2024. “It’s every artilleryman’s nightmare: The shell doesn’t explode kilometers away in the enemy positions, but shortly after leaving the gun barrel. This is exactly what happened to soldiers in Ukraine — with artillery shells that were partly supplied as part of the Czech munitions initiative,” the article reads. The purportedly malfunctioning shells — including some apparently from Excalibur Army — “resulted in injuries to soldiers and damage to artillery systems, ” the Handelsblatt article reported, noting the cause was traced to outdated World War II–era designed detonators; five out of every 10,000 shells fired exploded prematurely.

That’s one premature detonation for every 2,000 rounds fired. For a battery firing hundreds of rounds per day in active combat, that could mean a premature detonation every few days.

Jana Černochová, who was then the Czech minister of defense, challenged the Handelsblatt article, saying any quality issues were rare. “We know that we don’t just buy new ammunition, we also buy older ones that may have potential problems,” she said.

CSG subsidiary Excalibur Army reportedly also acknowledged “minor issues” with shells.

A source close to the Ukrainian Army told Hunterbrook that the attitude among Ukrainian artillery units was that unreliable shells were still better than no shells.

In its email, CSG told Hunterbrook that third-party sourcing “was primarily linked to the initial phase” of the Czech ammunition initiative and that the company is now “predominantly supplying large-calibre ammunition from its own production.” The company offered no data to support that claim.

Production Bottleneck: Bottlenecked

Then there may be a more immediate problem: a potential bottleneck at FMG — casting a shadow over how much the company can actually vertically integrate its ammunition production.

Hunterbrook reviewed CSG’s annual reports and press releases and found no references to existing propellant charge production outside of FMG.11 The Eurenco propellant charge plant, announced earlier this year, won’t be operational until 2028 at the earliest, meaning there’s a two-year gap during which growth appears to be constrained by a single factory.

A single factory that NATO has blacklisted.

In July 2025 — six months before the IPO — NATO’s procurement agency, NSPA, suspended FMG from bidding for new contracts, according to Amsterdam-based watchdog Follow the Money and a consortium of reporters that included the French outlet La Lettre. The suspension had since been extended indefinitely as of March, according to Follow the Money. In an email response to Hunterbrook’s question on NSPA’s ban on FMG, a NATO official said, “The NATO Support and Procurement Agency (NSPA) will not comment on ongoing proceedings concerning the suspension of contractors suspected in fraudulent and corrupt activities related to NATO contracts.”

The company told Follow the Money that the suspension was “unfounded” based on an internal audit. CSG also said in a statement that it was immaterial, given the fact that the “NSPA represents one of many FMG customers” and that FMG can still sell to NATO member states, even if blocked from selling directly to NATO. When asked about the suspension by Hunterbrook, CSG said: “To the best of our knowledge the situation regarding FMG is not related to any wrongdoing by the company, but to an ongoing internal investigation within NSPA concerning one of its officials.”

CSG also characterized the FMG suspension as “a temporary and procedural measure” with “no material impact on the group’s business performance,” and argued that its integrated manufacturing model — in which entities like FMG supply components internally — is “a core strength of our industrial model, not a concentration risk.”

But while NSPA itself may not be a major direct customer for FMG, the suspension at least raises the question of how NATO will treat products sold by other CSG subsidiaries that incorporate FMG’s propellant charges. After all, FMG’s 2024 accounts show 85% of its revenue went to intragroup customers. If NATO’s position is that sales from those entities are also suspended due to the incorporation of FMG products, the effect of the suspension on CSG as a group could be more pronounced.

The Price of Urgency

A separate question for CSG is how much the current revenue reflects the premium the company charges on wartime shortage, and how much longer those conditions will last.

One of the key pipelines for CSG’s delivery to Ukraine, the Czech ammunition initiative, is facing funding shortfalls. Launched in 2024 to pool funding from various Western countries to procure ammunition from around the world through intermediaries like CSG, the initiative had delivered 4.4 million large-caliber rounds to Ukraine as of February, Czech President Petr Pavel told Czech news outlet Odkryto.cz. However, the new Czech Prime Minister Andrej Babiš — notably a far-right populist who has been labeled pro-Russia — has publicly said that despite his commitment to keeping the Czech initiative alive, he will no longer finance it. He also committed to scrutinizing procurement deals and said he “was uncomfortable with individuals earning excessive profits from the war,” according to the publication Liga.

Other key members of the initiative like Germany, the Netherlands, and Denmark are also drawing back support. As of February, the initiative had raised only 1.4 billion euros out of the 5 billion euros targeted for 2026 — according to a senior NATO official who spoke to Reuters.

The initiative has faced numerous criticisms around cost, quality, and delay. Investigative journalists have accused the Czech intermediaries of charging margins at least four times higher than what Ukrainian arms brokers charge for comparable procurement. Critics also questioned why the initiative excludes other major defense suppliers like Rheinmetall and Norway’s Nammo.

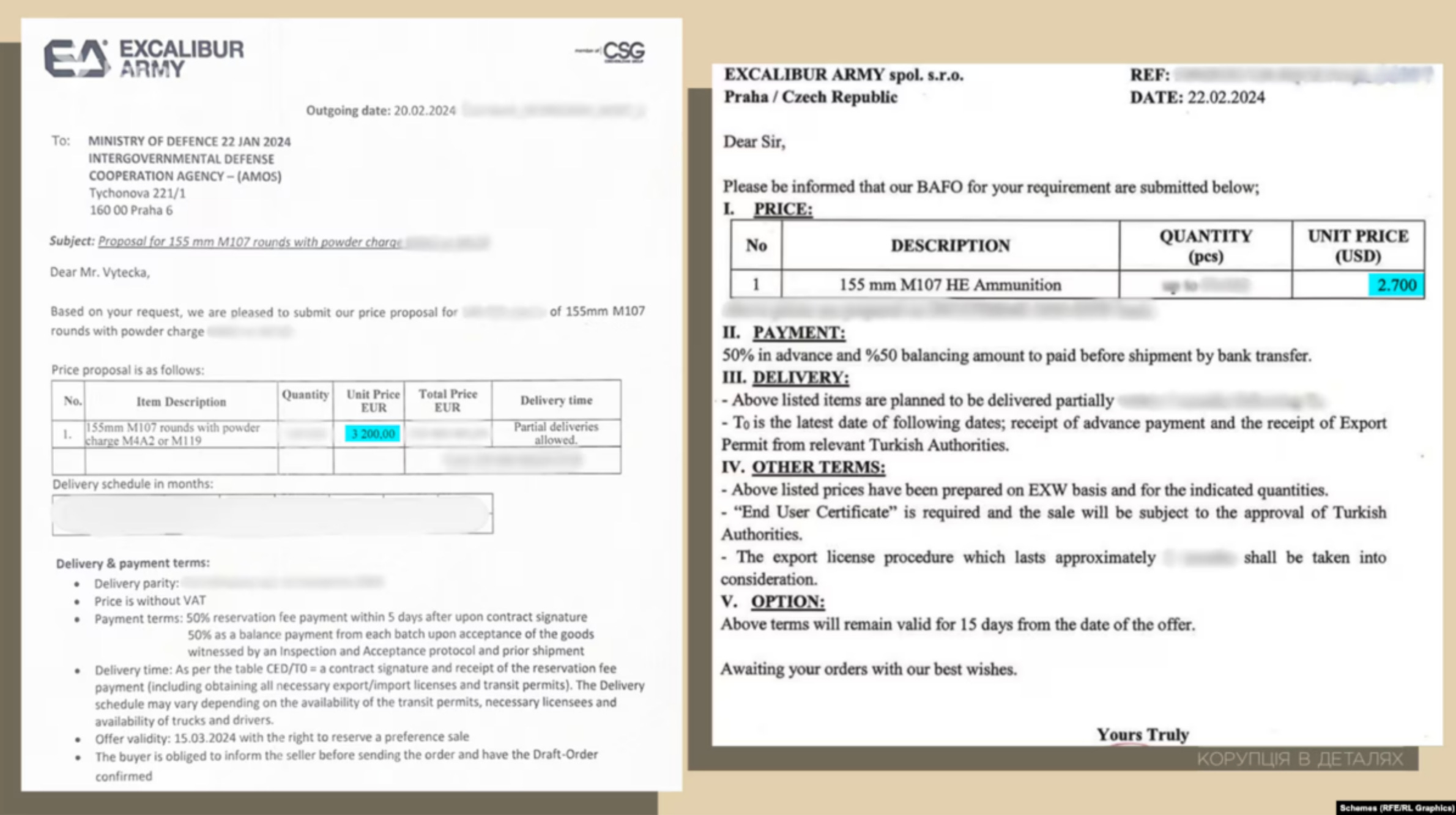

Documents obtained by the Radio Free Europe/Radio Liberty investigative unit Schemes, for example, show that in February 2024, CSG subsidiary Excalibur Army offered 155 mm artillery shells to the Czech government at 3,200 euros per unit. According to the investigation, “Around the same time, a Turkish manufacturer offered to sell seemingly similar M107 shells to Excalibur Army for 2,500 euros each” — a potential markup of roughly 30%.

CSG has publicly denied profiteering, calling the accusations “attacks based on half-truths and information taken out of the overall context.”

But the accusations are hardly new or limited to ammunition. In January 2023, the Kyiv Independent reported on a deal in which a broker earned 2 million euros — roughly 30% of the 6.8 million euro contract value — on a sale of 12,500 grenades destined for Ukraine from CSG’s export agency, Excalibur International, to a Dutch intermediary during the hectic days of the early invasion. Multiple European arms dealers told the Kyiv Independent the normal commission is between 5% and 10%.

Moreover, while competitors like Rheinmetall have a large backlog of long-term government contracts, CSG often charges customers the “spot” price for munitions, according to defense investors who spoke with Hunterbrook. In the near-term, this is a boon to margins, as CSG can essentially pick its price — like New York City bodegas selling umbrellas in the rain.

The problem with this business model is that it relies heavily on a continued shortage caused by perpetual conflict.

CSG’s underlying business, meanwhile, offers little margin of safety. Medium- and large-caliber ammunition delivered nearly two-thirds of CSG’s 2025 revenue, and the company’s flat-margin guidance for 2026 depends on that subsegment holding up. Land Systems, a subsegment responsible for 16% of revenue last year, is “expected to expand moderately.” The company expects “low to moderate margin improvement” in the Ammo+, responsible for 21% of revenue last year but saw its adjusted operating EBIT fall 58% year on year on a like-for-like basis on the back of what the company described as weaker commercial ammunition demand, rising input costs, and tariff headwinds.

So, this is the business reality. CSG appears to resemble the Cold War inventory-liquidation business it once was, with a manufacturing side business that seems much smaller than implied. The premium it charges is a wartime premium. The inventory it refurbishes may be running out. Its in-house manufacturer of a critical ammunition component is under indefinite NATO suspension. Its centerpiece growth contract depends on the participation of countries that say they hadn’t joined. And the cash it would need to close the capex gap with Rheinmetall might be cash it can’t generate.

Which brings us back to the IPO and the question that remains: How did CSG sell this story to investors in the first place?

The Operator

Part of the answer, again, may begin with what CSG left out.

Within weeks of the IPO, investigative journalists across Central Europe had identified serious omissions from the prospectus — including a put option exercised by a minority shareholder, Seznam Zprávy reported.

Hunterbrook dug deeper. The findings pointed to a company that appears to be concealing not just individual facts, but deeper aspects of its business — a sprawling network of intercompany transactions that obscure the way money flows and who really controls what.

And it seems to follow a pattern: Major milestones — from its first factory acquisitions to its largest government contracts — have often been accompanied by allegations of political favoritism, questionable business tactics, or conflicts of interest.

Undisclosed “Minority” Shareholders

CSG’s prospectus acknowledges, in generic legal language, that some subsidiaries have minority shareholders whose interests may differ from the company’s. It does not name all of them.

It also does not mention that one of them had already triggered a mechanism to force CSG to buy his stake — three days before the IPO. That shareholder is Petr Kratochvíl, according to a March 19 report from Seznam Zprávy.

Kratochvíl is not a passive investor. He ran Excalibur Army — CSG’s founding entity and most important subsidiary — for nearly 20 years, from 2005 until 2024. Until recently, he was also the chairman of the board of CSG’s Land System, the holding company that sits between CSG Group and Excalibur Army, company filings with the Czech registry show. He built “key parts” of the business alongside the Strnads, he said in an interview, and stood beside them through legal troubles, including a personal prosecution for purchasing anti-personnel mines. (He was later acquitted.)

Kratochvíl wants to sell his 10% stake in CSG Land Systems, he told Seznam Zprávy. He also has an 8.9% stake in MSM Group — another important subsidiary controlling CSG’s ammunition businesses.

On January 20 — the week of the IPO — Kratochvíl exercised a put option forcing CSG to buy his CSG Land Systems stake. His price: 1.4 billion euros, Seznam Zprávy said, citing an interview with Kratochvíl. CSG’s counteroffer: one-tenth of that.

Regardless of whose valuation is more accurate, the dispute is meaningful. While CSG Land Systems itself appears to be primarily a holding company, one of the assets it holds is Excalibur Army. In 2024, Excalibur Army reported 2.6 billion euros in revenue — two-thirds of the entire CSG group’s revenue for the year. Excalibur Army also held nearly 600 million euros in cash at that time.

Moreover, Kratochvil doesn’t just own 10% of the entity sitting atop CSG’s most important subsidiary. He also has “extraordinary rights.” His Class B shares carry four votes each, giving him veto power over changes to capital structure, articles of association, and corporate reorganizations, Kratochvíl told Seznam Zpravy in an interview.12 He also claims to have the right to a guaranteed buyback at market price.

In practical terms: Kratochvíl asserts he can block operational decisions at the entity that appears to control a subsidiary responsible for 578 million euros in cash and two-thirds of CSG’s revenue as of 2024.

The prospectus does not even name Kratochvíl. But if Kratochvíl’s valuation of his stake prevails, that’s a 1.4 billion euro liability that CSG may not have the cash on its balance sheet to pay.

In a March 2026 interview with Seznam Zprávy, Kratochvíl said he was promised there would be no IPO.

CSG told Hunterbrook in an email that the put option exists but that the auditors found “no liability (not even a contingent liability) that would need to be presented” in the annual report. Asked to confirm whether Kratochvíl exercised the put option days before the IPO, CSG replied that outside counsel confirmed Kratochvíl “did not effectively exercise his right regarding the minority stake before the IPO.” According to Seznam Zpravy, Kratochvíl delivered the notification twice on January 20: physically, via a courier to CSG headquarters, as well as digitally.

The omission of the details of Kratochvíl’s exercise of the put option in the prospectus doesn’t appear to be an anomaly. As Hunterbrook dug deeper, other omissions surfaced, revealing a pattern: a series of related-party transactions that seem to move cash to company insiders’ orbit — and sometimes, to their political partners — and a web of affiliated entities and shell companies that seem to play a questionable role in CSG’s acquisition practices.

Hidden Liabilities: Money Leaking to Strnad’s Orbit

Take, for example, the 275 million euros that Strnad’s personal vehicle likely owes CSG for which no evidence has been collected.

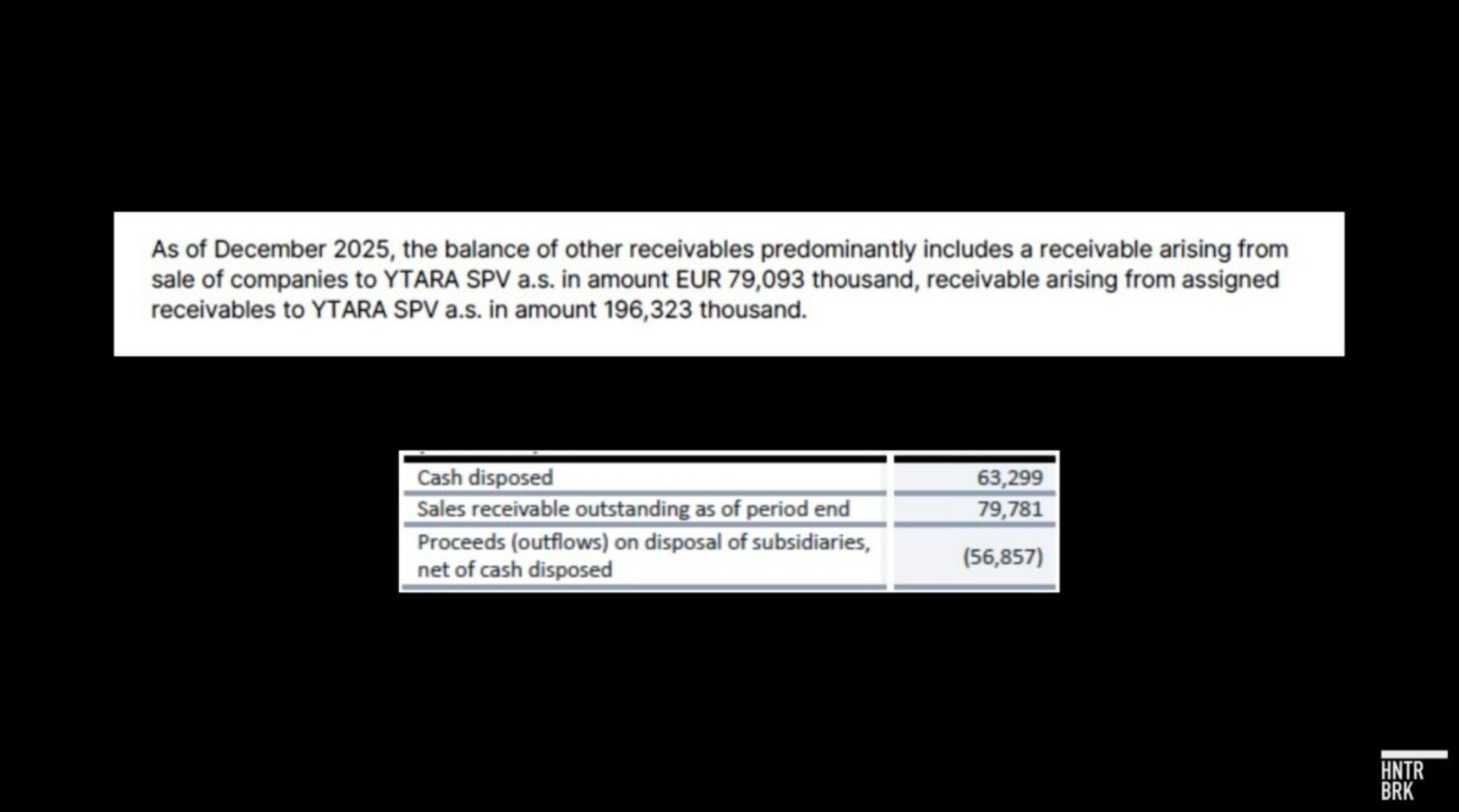

Ahead of the IPO, CSG transferred two dozen subsidiaries to Ytara SPV, an entity personally owned by Michal Strnad.13 The prospectus mentioned that non-core assets would be carved out but didn’t name Ytara as the recipient. The 2025 annual report clarifies that: 275 million euros worth of related-party receivables owed by Ytara from a disposal of subsidiaries.

Along with the disposal, 63.3 million euros in cash held by those entities left the group. CSG retrieved just a fraction of that, leaving CSG with negative cash proceeds of 56.9 million euros, the 2025 annual report further reveals.

Ytara SPV has since moved above CSG FIN in the corporate chain, according to CSG’s 2025 annual statement — meaning Strnad now controls the listed entity through a vehicle that’s absorbing assets from it.

Ytara’s articles of association as of December 4, 2025, filed with the Czech registry, give it broad authority, including to provide financial, trade, consulting, IT, and real estate assistance — notable capabilities for a holding company sitting between Strnad and the rest of the group that can facilitate upward cash movement without public disclosure.

In an email to Hunterbrook, CSG described the pre-IPO restructuring as “standard,” explaining the carved-out entities — which included “a Czech manufacturer of railway braking systems” and “an Italian producer of luxury sporting firearms” — were non-core. The company said “all related party transactions (including the 275 million euroreceivable from carved-out business) will be fully settled in cash.” Asked why CSG did not disclose that Ytara was owned by Strnad in the prospectus, the company said the information is publicly available in the Czech Commercial Register and reiterated that “all relevant related-party transactions were properly disclosed” in the prospectus.

“Disposing” of subsidiaries by moving them to the CEO’s personal vehicle isn’t the only way the company’s assets seem to flow to company insiders. As of 2024, Excalibur Army, perhaps CSG’s richest subsidiary, reported CZK 118 million (~4.7 million euros) in “other short-term receivables,” which consisted principally of receivables from Jaroslav Strnad, the company’s founder and current CEO’s father — a detail not disclosed as a related-party transaction at the group level. Excalibur Army also wrote off CZK 327 million (~13 million euros) in “time-barred receivables” — debts so old the company gave up collecting — raising the question of whether the same fate awaits the company’s claim on the senior Strnad.

For its part, CSG dismissed the 13 million euro write-off of time-barred receivables at Excalibur Army as an accounting necessity, saying it “does not represent the incurred losses but rather only theoretic risk.” The company did not address the 4.7 million euro receivable from Jaroslav Strnad.

Excalibur Army’s 2024 filing also lists a waste disposal company as a contract counterparty, with contracts dating back to 2015 on services including office rental and sewage operation.14 That company’s own filing shows 90% of the company was moved out of CSG into Jaroslav Strnad’s personal company, CE Industries, in 2019. CSG did not disclose this as a related-party transaction in its prospectus.

In another example of funds moving into Strnad’s orbit, the cash trail could be extended even further — to political partners. After leaving CSG in 2022, former Vice-Chairman Miroslav Dorňák acquired, at an undisclosed price, a real estate company to which CSG had previously transferred CSG’s real estate assets, also for an undisclosed price. The company then bought the building into which CSG moved its headquarters, according to multiple Czech press reports and registry filings.15 Essentially, CSG now pays rent to its former vice-chairman’s company.

In an email to Hunterbrook, CSG called the lease “a standard landlord–tenant relationship” and said it does “not comment on the business activities of third parties.”

A Czech registry filing shows Dorňák also owns a Czech crowdfunding platform called FinGood, which shares the same address as CSG’s headquarters.16 According to a March 2026 investigation by Seznam Zprávy, FinGood paid millions to Slovak Defense Minister Kaliňák’s legal consultancy firm, Kallan Legal, citing a former CEO and co-owner of Kallan and the current FinGood CEO who confirmed the payments. Seznam Zprávy alleged that CSG, including Michal Strnad personally, was involved in the management of FinGood, citing FinGood employees and internal emails obtained by the outlet.

Kaliňák, as noted earlier, is behind the recent 58 billion euro ammunition deal with CSG.

The Shadows Behind the Empire

CSG’s post-IPO disclosures may be lacking. But they’re less surprising when set against the company’s history — a three-decade record of political patronage, questionable acquisitions, and ties to figures that would give any compliance officer pause.

The company’s origin story is inseparable from Czech state connections. CSG was founded by the CEO’s father, Jaroslav Strnad, in the mid-1990s as a scrap dealer, collecting Societ-era military assets liquidated after the Cold War, refurbishing them, and reselling them at a markup. Jaroslav Strnad’s father-in-law served as deputy head of the material and technical support office at the Czech defense ministry — a role that Czech media reported helped steer Strnad toward his surplus military equipment deals.

Numerous accounts of CSG’s dealings highlight its ties to Miloš Zeman, who served as the president of the Czech Republic from 2013 to 2023. CSG’s domestic growth accelerated after Zeman took office in 2013.

Ahead of Zeman’s 2018 re-election, Jaroslav Strnad became Zeman’s largest campaign donor. Two Strnad-linked firms, DAKO-CZ and Composite Components, together accounted for two-thirds of all campaign contributions, according to OCCRP. Seznam Zprávy reported that his son, Michal Strnad, used a car pawn company to channel hidden cash to Zeman’s campaign: Internal documents recorded a CZK 950,000 transfer as directed by Strnad personally, routed through an intermediary entity called Car Service Group CZ.

Milestones in CSG’s growth during Zeman’s tenure, including major acquisitions and contracts, were often flagged by journalists and regulators as irregular. For example, an investigation by the Ukrainian outlet Gordon found the sale of an armored vehicle repair and production factory to the then-named Excalibur Army in 2013 “puzzling,” noting the state had spent substantial sums of money reconstructing it; a source told Euro that Strnad bought the plant “for a really good price.” Other coverage found CSG had received major orders from the government without a competitive tender for one truck contract in 2017.

Some investigations even led to formal arrests, only for the cases to be dismissed later. In 2015, defense ministry and army personnel were charged with transferring surplus Czech military property — specifically tank engines and spare parts — to Excalibur at below-market prices. The case later ended in acquittal, with Česká Justice reporting a “complete failure of the investigative bodies.” Notably, two of the acquitted defense ministry officials ended up working for Strnad.

Other cases are ongoing.

Marián Goga, former president and 10% owner of MSM Group — the parent company controlling CSG’s ammunition businesses, is currently facing criminal charges in Slovakia for “bribery and money laundering.17”

Prosecutors alleged Goga, in his former capacity as the head of CSG subsidiary MSM Martin, steered a public tender for recovery tanks through a bribery scheme in which MSM Martin paid 15 months of warehouse rent in a single day to an intermediary, who then transferred two below-market apartments to the son of the state strategic reserves chief. The intermediary reportedly committed suicide after the transfers became public.

MSM Martin, which is a codefendant, could face serious consequences if found guilty, CSG disclosed in the prospectus. Penalties could include “the forfeiture of assets,” a “financial penalty,” and “a prohibition on receiving EU funds” — in light of which MSM Martin “wound down all business activities and is currently a dormant entity with no significant assets.” Ahead of the IPO, CSG reorganized its structure to remove MSM Martin and Goga’s shares in MSM Group. It’s unclear how Goga was compensated.

CSG told Hunterbrook in an email that Goga “was indeed a former shareholder and executive director of MSM Martin” and was a shareholder of MSM Group “until January 2026, i.e. prior to the IPO.” But the company also confirmed that Goga “currently serves on the supervisory board of MSM Group” — a fact the prospectus omitted. CSG said Goga “has played a positive role in the development of the business and continues to support the company in this supervisory capacity,” and that the criminal proceedings “remain ongoing” with “no material developments.”

The pattern of strange deals extends beyond Europe. CSG’s announced contracts in Southeast Asia — a region the company has cited as a growth market — often flow to a single country, Indonesia, and substantially through a single intermediary. Since 2015, CSG subsidiaries have announced roughly $3.7 billion to $4 billion in Southeast Asian defense contracts, including an over 500 million euro KHAN ballistic missile package signed in November 2022, a $300 million Patriot II armored vehicle deal announced 13 days after the January 2026 IPO, and a $2.5 billion air-defense megapackage disclosed in April 2026.

Some of these deals are, themselves, reportedly funded by the Czech Export Bank — a state-owned institution backed by Czech taxpayers. The structure is circular: A Czech state bank lends to Jakarta so Jakarta can pay a Czech private company, and the resulting revenue inflates the backlog that helped underpin CSG’s 25 billion euro IPO valuation.

Then there is the question of where CSG’s original capital came from. Foreign Policy reported in 2018 that one of Jaroslav Strnad’s key investors was Alexei Belyaev, described as connected to Vladimir Yakunin, the sanctioned former head of Russian Railways and Putin associate. Corporate filings confirm that Belyaev and his partner Michal Lazar were co-investors in DAKO-CZ, a CSG subsidiary. Belyaev joined DAKO-CZ’s supervisory board in 2016.

A WikiLeaks-published U.S. Embassy cable identified Lazar as suspected of organized crime connections; the cable noted that Slovak police appeared “clearly uncomfortable” discussing him. “Strnad’s partner is widely reported to have a business association with senior Russian intelligence officers,” The American Spectator wrote.

Belyaev and Lazar’s company, Optifin Invest, reportedly became a major co-investor in CSG entities. A Czech security analyst told Ukrainian news outlet Gordon in 2020 that this structure was designed so that “Belyaev was the one who was coordinating the whole strategy from the very beginning” of CSG’s expansion.

Journalist Jaroslav Spurný told Gordon, citing internal sources, that “substantial amounts involving Russian financing” flowed through Creditas bank — which shared a Prague office building with CSG and had connections to First Czech-Russian Bank, described by Czech intelligence as an FSB, or Russian intelligence, instrument. CSG had a separate revolving loan from Creditas worth up to CZK 330 million, according to Czech news organization Euro. A former Czech intelligence chief told Gordon that CSG is “in bad financial state and these debts are all owed to the Russians.” CSG has denied the Russian financing allegations, and the Belyaev/Lazar involvement formally ended with a 2021 DAKO-CZ stake sale. CSG told Hunterbrook it “immediately ceased all activities in Russia” in 2022.

But the security concerns over CSG’s ties to Russia were apparently serious enough that a CSG subsidiary had issues receiving a security clearance from the Czech National Security Office — effectively barring CSG from supplying the Czech military. Defense Minister Karla Šlechtová confirmed: “If someone does not have the requisite security clearance, they do not meet the formal criteria to receive an order, and thus cannot receive it. This is exactly what happened with the Czechoslovak Group.”

The company did not appeal the decision in court — a choice a former head of Czech intelligence noted suggested CSG had “real problems” it did not want aired publicly, according to Gordon. Strnad “transferred all of his companies to his 25-year-old son Michal.” CSG denied any connection between the clearance issue and the transfer.

Jaroslav Strnad admitted as much himself, though he put it a bit more mildly: “I understand that my name is connected to a number of people and events that could negatively impact the company and its reputation,” he told Respekt in 2018.

These concerns resurfaced in 2024 — this time in the U.S. — when multiple Republican senators including JD Vance raised objections to CFIUS about CSG’s acquisition of Vista Outdoor’s ammunition unit, The Kinetic Group.

“We cannot afford for America’s supply of weapons to fall into the wrong hands,” Vance wrote in a January 2024 letter to U.S. Treasury Secretary Janet Yellen, requesting a security review of the sale. “Until it can be proven that this transaction will not jeopardize our national security, I respectfully urge you to deny the sale of Vista Outdoor’s Sporting Products business to the Czechoslovak Group.”

Vance’s letter raised concerns about ties to Putin’s inner circle, including the company’s sponsorship of a show in Moscow aimed at facilitating Russian access to European military technology. CFIUS ultimately approved the deal.

But CSG’s choice of personnel reinforces the pattern. In February 2024, CSG appointed Jan Hamáček as its director of external relations. Hamáček had previously served as Czech minister of the interior — and was investigated by the Czech National Center for Organized Crime after Seznam Zprávy reported that he had planned to travel to Moscow to exchange Czech silence on the 2014 Vrbětice ammunition depot explosions — which killed two Czech citizens and were attributed to GRU agents — for, among other things, a Biden-Putin summit in Prague.

Police ultimately dropped the case because Hamáček did not end up taking the trip to Moscow. But a company that hires an official investigated for involvement in a Russian intelligence operation to run its government relations is making a statement about its priorities — whether it intends to or not.

It’s an especially odd statement, of course, from a company whose riches — however ephemeral they may be — are a direct result of Russia’s invasion of Ukraine.

Read the full version of the investigation, including all of the footnotes, on our website at hntrbrk.com/csg.

Authors

Jenny Ahn joined Hunterbrook after serving many years as a senior analyst in the US government. She is a seasoned geopolitical expert with a particular focus on the Asia-Pacific and has diverse overseas experience. She has an M.A. in International Affairs from Yale and a B.S. in International Relations from Stanford. Jenny is based in Virginia.

Till Daldrup is an investigative journalist who joined Hunterbrook from The Wall Street Journal, where he focused on open-source investigations and content verification. In 2023, he was part of a team of reporters who won a Gerald Loeb Award for an investigation that revealed how Russia is stealing grain from occupied parts of Ukraine. He has an M.A. in Journalism from New York University and a B.S. in Social Sciences from University of Cologne. He’s also an alum of the Cologne School of Journalism (Kölner Journalistenschule).

Blake Spendley joined Hunterbrook from the Center for Naval Analyses (CNA), where he led investigations as a Research Specialist for the Marine Corps and US Navy. He built and owns the leading open-source intelligence (OSINT) account on X/Twitter, called @OSINTTechnical (over 1 million followers), which also distributes Hunterbrook Media reporting. His OSINT research has been published in Bloomberg, the Wall Street Journal, and The Economist, among other top business outlets. He has a B.A. in Political Science from USC.

EDITOR

Sam Koppelman is a New York Times best-selling author who has written books with former United States Attorney General Eric Holder and former United States Acting Solicitor General Neal Katyal. He helped build Fenway Strategies into one of the preeminent strategic communications firms in the country—with side quests speechwriting for Michael Bloomberg, running the surrogate remarks operation on the Biden-Harris campaign, and co-founding Mayday, which is now one of the leading information providers on how to access reproductive health care in states with bans. Sam has published in the New York Times, Washington Post, Boston Globe, Time Magazine, and other outlets — and occasionally volunteers on a fire speech for a good cause. He has a BA in Government from Harvard, where he was named a John Harvard Scholar and wrote op-eds like “Shut Down Harvard Football,” which he tells us were great for his social life.

Graphic