Inside Hamilton Lane’s Pandora’s Box

Bethany McLean: While the world obsesses over private credit, private equity might be in murkier territory.

By: Bethany McLean, Matthew Termine, JD Jean-Jacques

Editor: Jim Impoco

Based on Hunterbrook Media’s reporting, Hunterbrook Capital is short $HLNE and long a basket of comparable securities at the time of publication. Positions may change at any time. See full disclosures on our website.

“I literally think all the marks are wrong.”

A few weeks ago, Apollo’s John Zito found himself unexpectedly in the headlines for brutally honest remarks he thought were off the record about private market valuations.

As the co-president of Apollo’s asset management arm, Zito is a titan in the private credit and private equity markets. And his grim assessment added fuel to the fire that is racing through an industry whose marks are being more heavily scrutinized amid a “SaaSpocalypse” triggered by AI disruption.

The funny thing about the discourse, as Zito pointed out, is that so far, it has mostly focused on private credit, rather than private equity. This ignores a basic rule of finance: In any capital structure, debt is the safety net, and equity is the high-wire act.

Which is to say: If people are scared of the debt, they should be terrified of the equity. “I can’t compute, but I’m the dumb guy,” Zito said. “I don’t understand.”

Zito isn’t dumb.

And if the cracks he identified are indeed signs of a larger structural failure — as JPMorgan’s Jamie Dimon and former Goldman Sachs CEO Lloyd Blankfein have also signaled — one place they might manifest is private markets colossus Hamilton Lane ($HLNE).

This week, the private equity firm — which sells to retail investors — recorded its largest net outflow in recent history with investors pulling an estimated $172 million from the fund in March alone. Redemptions like these could create a feedback loop, through which the true value of Hamilton Lane’s assets, independent of its current mark, could be revealed.

A Gatekeeper to Private Equity

Headquartered in Conshohocken, Pennsylvania, Hamilton Lane is a roughly $4 billion market cap investment powerhouse that has spent three decades evolving from a niche research shop into a gatekeeper for the private markets. As of last year, it managed or advised on $1 trillion of assets, and it positions itself as the bridge between institutional-grade private equity and a new, hungry class of retail investors.

In the last five years, Hamilton Lane has made its business, which mostly comes from the assets it manages, increasingly dependent on buying assets known as “secondaries.” This is particularly true of the almost $6 billion Hamilton Lane Private Assets Fund, or PAF. In other words, Hamilton Lane has increasingly bought stakes in private equity portfolios from sellers who want to unload them.

This has looked like a fantastic business in part because of a specific accounting quirk first scrutinized by The Wall Street Journal: Hamilton Lane buys the assets at what it considers a discount and can then promptly mark these assets back up to the previous valuation, even if there were no buyers at that old price. We’ll refer to these as “day-one markups.”

Last year, Hamilton Lane brewed another accounting potion, changing the way the firm is compensated. It used to be paid incentive fees when gains were realized — meaning when the underlying assets were actually sold. Now, it can collect its fees regularly based simply on increasing its own marks on its investments, including those day-one markups. The change allowed Hamilton Lane to pull forward fees that may have taken years to accrue. Thanks to the new fee structure, Hamilton Lane took in $58 million of incentive fees from the Private Assets Fund in the year that ended in March 2025.

In a statement to Hunterbrook addressing the issue, the company said that “because semi-liquid funds typically reinvest proceeds rather than distribute them, traditional carry calculations based on distributions are less appropriate, making NAV-based carry a better fit.”

The firm made another change at the same time, one that has gone largely unremarked: It began excluding stock-based compensation from its fee-related earnings calculation, just like competitors like Blackstone ($BX), Apollo ($APO), and Carlyle ($CG) do. The combined effect of the two changes — adding performance fees based on unrealized gains as a revenue stream and stripping out stock-based compensation from expenses — moved Hamilton Lane’s reported fee-related earnings margin (which is an important component in how Wall Street values firms like Hamilton Lane) from roughly 32% to approximately 59% for the nine months ending in December 2025.1

The decision to exclude stock-based compensation isn’t all that unusual — but the timing is worth noting. About six months before Hamilton Lane changed its calculation of the metric, co-CEOs Erik Hirsch and Juan Delgado-Moreira each received 544,000 restricted shares — a grant valued at roughly $71 million apiece, with vesting tied to stock price targets.

While previous reporting by both The Wall Street Journal and the Financial Times identified the existence of the day-one markups and the firm’s new fee structure, our reporting goes a step further to reveal the true depth of the distortion. An analysis conducted by Hunterbrook shows that about a third of the total gains in valuations across PAF’s portfolio were largely generated by these accounting uplifts, rather than any actual appreciation of the companies owned.2 (In a statement to Huntebrook, Hamilton Lane said that more than 70% of secondary returns in the fund are not a result of the day-one markups, roughly confirming our estimate that one third of the returns is attributable.)

And the change to the way Hamilton Lane collects fees explains more than all of its recent fee-related earnings growth. In other words, without the change to collecting fees along the way, rather than growing fee-related earnings by 37%, earnings actually would have gone down over the last nine months of 2025.3

In good times, Hamilton Lane’s accounting alchemy can seem infinitely repeatable: Raise money, buy assets, mark up assets to charge performance fees, report high returns, use those high returns to raise more money from retail investors, use that money to buy more assets, and on and on.

But when investors begin to look behind the curtain, they may notice that some of their returns exist only in the realm of illusion — and that they are paying Hamilton Lane fees for those fantastical returns.

If the enchanted flywheel breaks, and Hamilton Lane can’t keep raising billions of dollars to buy (and then immediately mark up) new assets, the magic can start moving in reverse: Redemptions lead to forced asset sales lead to markdowns lead to pressure on reported returns lead to stalled fundraising, etc.

The only question, for now, is whether investors open that Pandora’s Box.

This is, oddly enough, an analogy Hamilton Lane has wholeheartedly embraced, albeit in a slightly different context.

In a recent 2026 market overview presentation that is an exercise in mixed metaphors and potentially unintended messages, Hamilton Lane’s former CEO, Mario Giannini, who still serves as executive co-chairman and on the investment committees of its various funds, dressed up as Gandalf from The Lord of the Rings. “What do you think Pandora imagined the moment she opened that box?” he asked. “A box that shouldn’t be opened is opened anyway and out pours … what exactly? Depends on who you ask.” He said investors should think of Hamilton Lane as the “Gandalf of the private markets Middle Earth,” sent to “guide and inspire” them on their journey.

The problem for Hamilton Lane itself is that in this business, eventually, reality has a way of being a Morgoth. Just like with private credit funds, investors are starting to worry about private equity, too — and could begin to demand their money back from PAF. Hamilton Lane’s stock is already down 50% from its peak amid this fear. And there are reasons to believe that it could fall much, much further.

Asked repeatedly about these issues, Hamilton Lane did not initially respond over a period of days; then, once receipt was confirmed, the company made legal threats to a Hunterbrook reporter, and, finally, provided answers to our questions. “The way we calculate fees is in fact the industry standard, and you can find examples of numerous other funds, including ones with strong secondary exposure,” said a spokesperson. Indeed, other funds, like Blackstone, Apollo, and Carlyle, collect performance fees that aren’t dependent on selling underlying investments.

The statement continued: “While the discounts in secondaries are intended to be additive to performance, in accordance with U.S. accounting standards, our analysis shows that the vast majority of long-term performance comes from underlying growth of the companies.”

Deference to Marks

Hirsch and Delgado-Moreira took over Hamilton Lane in 2024, more than three decades after Hamilton Lane’s founding by Leslie Brun, who came to the U.S. from Haiti as a young boy.

The original idea was to provide research for institutions that wanted to invest in private equity. Brun, who is now the cofounder, chairman, and CEO of Ariel Alternatives, departed in 2005 and seemingly has little to do with Hamilton Lane. Over the years, the business shifted away from just advising other investors, and toward managing capital directly. By the time Hamilton Lane went public in 2017, it managed $40 billion in assets, primarily by making investments in other funds or investing directly alongside those funds.

Just after the IPO, Hamilton Lane found itself enmeshed in the Abraaj scandal, where a Dubai-based private equity firm that at its peak managed almost $14 billion unraveled due to alleged fraud. Hamilton Lane had committed clients’ money to an Abraaj fund — despite warnings about valuation problems, according to The Economist.

On September 20, 2017, an anonymous whistleblower emailed Hamilton Lane executives, warning that Abraaj was overvaluing its holdings and that deals in its pipeline were dead. The email urged Hamilton Lane to do proper diligence before committing to Abraaj’s new Fund 6. Instead, Hamilton Lane employee Tarang Katira, who ran fund investments across Europe, the Middle East, and Africa, forwarded the whistleblower’s email directly to Abraaj founder Arif Naqvi, according to Bloomberg and The National reporting at the time.

Katira wrote to Naqvi that he was sending it so Naqvi would be aware the email was “out there and clearly targeting LPs.” Despite the warning, Hamilton Lane went on to commit $100 million to Abraaj Fund 6 — a commitment that reportedly encouraged other investors to put in roughly $900 million more. (Fund 6 never closed after the scandal broke, so those specific commitments did not result in losses; Hamilton Lane’s total Abraaj exposure across funds was approximately $382 million.)

The firm eventually shook off the Abraaj taint. But the episode illuminated something about how Hamilton Lane relates to other firms’ marks: with deference. The business it has built since is, in a sense, one where that deference is no longer a bug — where accepting the fund manager’s number has become the business model.

Hamilton Lane has doubled down on two strategies, in particular, that have helped catapulted the firm into the stratosphere.

The first was the launch, in 2019, of what are called evergreen funds. Traditional private equity funds raise money at the start of their life cycle. The money is usually locked up for about a decade. An evergreen fund, on the other hand, raises money by selling shares continuously. Existing investors are allowed to withdraw specified amounts at specified times. Hamilton Lane says that “upwards of 25%–30%” of its capital comes from institutions, but this liquidity-on-demand promise helped open the floodgates to retail investors.

In its recent presentation, Hamilton Lane’s Beth Nardi said that its evergreen funds are “really shaking things up.” The reason is that they are so easy for retail investors to use. “Prior to evergreens, investing in the private markets was, let’s be honest, a hassle,” added Brian Gildea, who runs the firm’s evergreen business.

Since 2020, the industry-wide evergreen business has more than tripled, to roughly $700 billion in global assets as of 2024. Bigger firms, like Blackstone, Apollo, and the ever-controversial Blue Owl ($OWL), are in the game, too, because everyone wants to get their hands on retail investors’ money — not to mention collect permanent fees, instead of having to launch new funds in order to keep the fees coming in.

Today, Hamilton Lane manages $17 billion of assets in various evergreen products, up from almost nothing in 2020 — and up 70% in just 2025. None of its competitors are as exposed to the retail business. Goldman Sach’s analysis shows that Hamilton Lane derives 34% of its management and incentive fees from retail and evergreen vehicles, versus 24% at Blackstone, 23% at Blue Owl, and single digits at Carlyle and Brookfield ($BAM).

The second big move was plowing all that retail money into the secondary market. This business has come into existence not because private equity is doing so well, but rather because it is struggling. Private equity firms are having a tough time cashing out in the usual ways, like selling a company or taking it public, and so a massive backlog of unsold companies has formed. According to McKinsey’s most recent Global Private Markets Report, over 16,000 buyout-backed companies have been held for more than four years — 52% of total buyout inventory, the highest share on record.

Investors are understandably antsy. So the way for existing investors to get out is selling their stakes to a new buyer, usually at a discount to their marks. In 2025, secondary transaction volume hit all-time highs, up 48% year-over-year. Hamilton Lane has been a huge buyer — at PAF, secondary stakes appear to account for almost half the fund’s value.

Where others see a crisis of liquidity, Hamilton Lane sees a heroic opportunity. The firm presents itself as the savior of the private equity ecosystem. After outlining the problems, Hamilton Lane’s co-head of secondary investments, Tom Kerr, who was dressed up as a knight, said, “Secondaries to the rescue!” He added, “Grab your shield, join the charge, let secondaries lead you to solid ground.”

The ground might be a tad shakier for buyers, however. Despite its medieval theme, Hamilton Lane’s video doesn’t mention the accounting sorcery laced through the company’s results. The day-one markups happen consistently — for example, last December, PAF acquired a stake in an A.Capital Partners vehicle for $50 million, and marked it up to $68.5 million within the same month. That same month, on December 31, a stake in a Hellman & Friedman fund was acquired for $20.3 million and marked up to $23.9 million the same day.

It’s not surprising that day-one markups account for about a third of PAF’s reported returns, according to an analysis conducted by Hunterbrook.

“The fair values of such investments as reflected in a fund’s NAV do not necessarily reflect the prices that would actually be obtained if such investments were sold.”

The practice of marking up assets on day one is allowed under accounting rules called a “practical expedient”: essentially a shortcut to make complex accounting easier. Hamilton Lane is not the only private equity player that takes advantage of this accounting practice: from StepStone ($STEP) to Apollo, funds utilize day-one markups of secondary interests. For example, the Apollo S3 Private Markets Fund, also an evergreen fund offered to retail investors, marks up stakes immediately.

At least three investor advocates have asked the Financial Accounting Standards Board to reconsider guidance that permits the practice. In one recent request, Mark J. Higgins of Enlightened Investor argues that markets have evolved since the existing guidance was issued. Indeed, while Hamilton Lane touts the depth of its relationships as a reason it can buy stakes at a discount, the secondaries business has become incredibly competitive. Investment banks like Evercore brag about their business advising buyers and sellers of secondary stakes.

If lots of people are fighting to buy something, it’s hard to believe anyone’s getting a steal. And if secondary transactions are occurring at ever-higher frequency and volume, why is there a need for expediency? Isn’t the price at which the secondary transactions occur a more accurate measure of value than the underlying fund’s NAV?

Some industry insiders defend the practice. At a recent SEC panel, Blake Nesbitt, the chief investment officer of the asset management firm Cliffwater, said the valuation process is not ideal — and leaves room for error — but noted that buyers don’t have the ability to delve into all of the underlying investments and figure out what each one is worth. For that reason, accepting a fund’s valuation can simplify an otherwise arduous task.

Others, including a former Hamilton Lane employee who spoke with Hunterbrook, argue that the actual sellers — investors in private equity funds — are willing to accept less than their stake might otherwise be worth in order to get liquidity. In its comment to Hunterbrook, Hamilton Lane says, “The simple fact is that investors in private equity funds will often sell their fund interests in the secondary market at a discount to their current value in exchange for liquidity prior to the end of a fund’s term. These transactions are negotiated between a willing seller and a willing buyer and are based on a record date valuation that is often months or quarters in advance of the transaction closing.” Which may be true, but does not account for the expanding depth of the secondary market itself and what that may mean for these “liquidity” discounts.

In Hamilton Lane’s market presentation, Gildea, co-head of evergreen portfolios, took a slightly different tack, saying it’s “clear” that the criticism that evergreen funds’ returns are not sustainable because of their use of secondaries to boost returns cannot be true, because to date, evergreen funds have outperformed. Well, yes, but every magic trick fools the audience until it doesn’t. If funds are outperforming based on marks that haven’t been tested, are they really outperforming?

Then there is the growing constipation in private equity: the industry’s increasing inability to exit the companies it owns. It’s hard to escape the logic that the gigantic backlog of unsold PE-backed companies reflects a growing disconnect between private equity marks and what buyers are willing to pay.

Add to all that the SaaSpocalypse. Software represents approximately 25% of total PE deal value over the past five years, and publicly traded software companies have plunged due to worries about the disruption from AI. Just as the buyout debt is being repriced by a skeptical market, the equity is facing a valuation reckoning that the industry’s internal marks have yet to acknowledge.

A March note from research firm KBW quantified Hamilton Lane’s exposure. After a trip with the company’s CFO and investor relations team, analyst Alex Bond reported that software represents 23% of total fee-paying assets under management and 30% of PAF.

Publicly, both private equity and private credit firms say their investments are doing fine. And one genuine advantage of private equity math, compared to private credit math, is that funds can be worth a great deal even if most investments are losers, so long as there’s one big winner that compensates for the wreckage. Power law and all that.

But it’s a little hard to believe that investors would be offloading stakes to Hamilton Lane at such steep discounts if the funds truly held such trophy assets.

And privately, you hear some doubts about the quality of these private market portfolios more generally. “Most of the businesses that were bought from 2018 to 2022 are lower quality than those companies,” Apollo’s Zito said in that supposedly off-the-record conversation, comparing private software businesses unfavorably to their public market counterparts. (Apollo shared in an earnings call that the company has 0% exposure to software in its private equity business.) “So I am concerned about many of [those] take-privates,” Zito noted.

Hamilton Lane’s own disclosures acknowledge the uncertainty: “Because there is significant uncertainty in the valuation of, or in the stability of the value of, illiquid investments, the fair values of such investments as reflected in a fund’s NAV do not necessarily reflect the prices that would actually be obtained if such investments were sold.”

A “Very Dangerous” Combination

While it’s true that other funds are also taking fees on unrealized gains, even industry veterans are taken aback by the combination of the evergreen fee structure and the reliance on day-one mark ups. Nesbitt, the Cliffwater CIO, called it “very dangerous,” noting that this structure effectively prioritizes the general partner’s fees over the investor’s reality. He called the arrangement “unheard of” in the history of private markets.

What isn’t widely understood is what a huge impact the accounting magic has had on Hamilton Lane’s earnings.

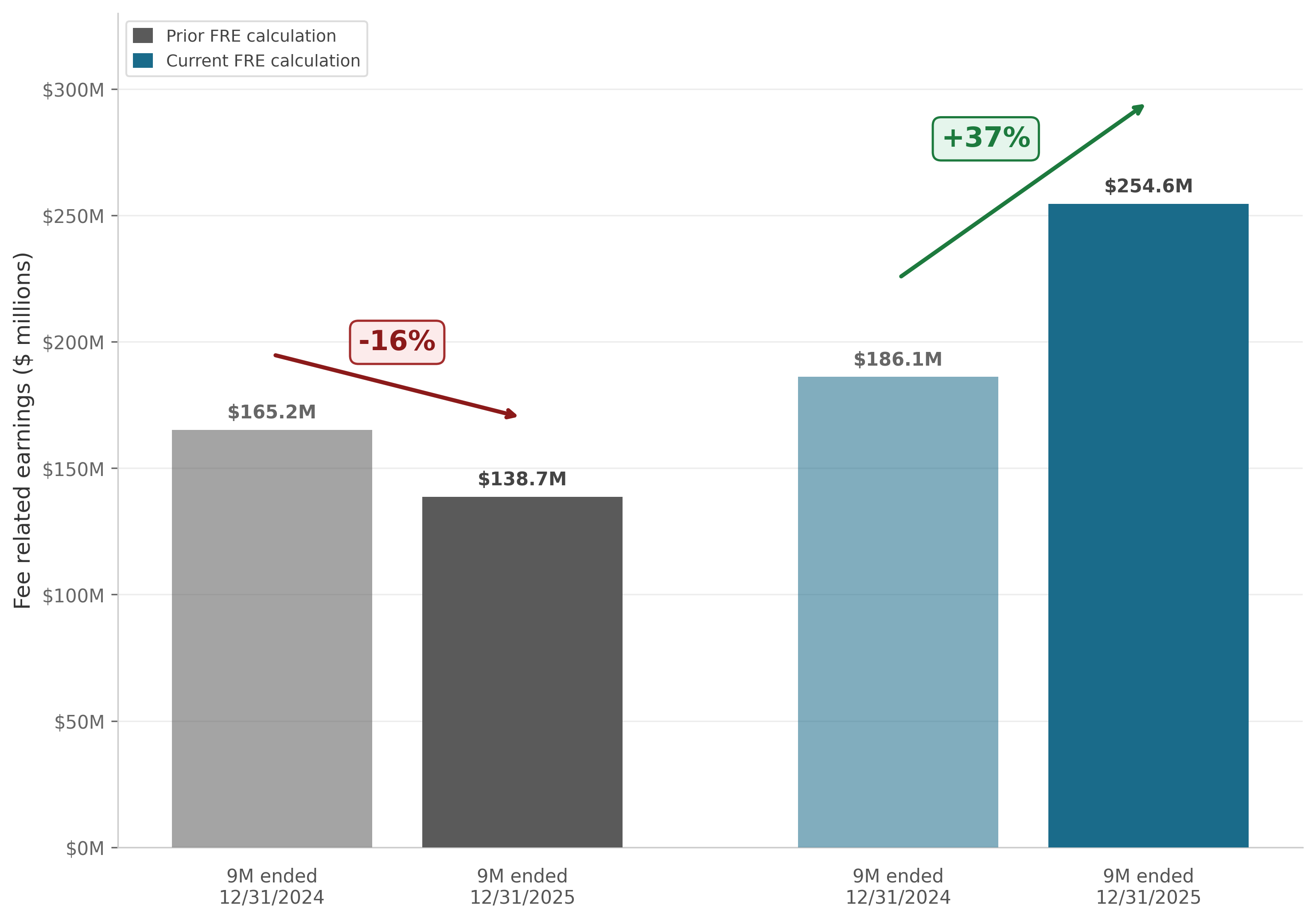

Overall, in the latest earnings call, Hamilton Lane reported $507 million in fee-related revenue for the nine months ending December 2025, with fee-related earnings up 37% year-over-year. But buried inside those stellar numbers is a newly created metric doing most of the heavy lifting.

Hamilton Lane’s total fee-related revenue is now the sum of standard management fees and something called “fee-related performance revenues,” or FRPR. In early 2025, Hamilton Lane said it “modified” its definition of fee-related earnings to exclude equity-based compensation and include FRPR. FRPR, says the firm, is “not dependent on realization events of the fund’s underlying investments.” Translation: These are fees Hamilton Lane collects based on markups that exist only on a spreadsheet, and which will only keep flowing if NAV keeps going up.

By simultaneously including this new metric and excluding stock-based compensation, the firm’s fee-related earnings grew by 37% year over year. Without it, growth would have actually been negative 16%.

In other words, more than 100% of the firm’s fee-related earnings growth came from technical adjustments, not any change to the fundamental value of the businesses it owns.

Troublingly, analysts, many of whom tell investors to buy Hamilton Lane’s stock, have priced Hamilton Lane as if this “new” revenue stream will grow smoothly for years. Goldman Sachs’ model, for instance, contemplates that after a blip in 2026 caused by a spike in redemptions, PAF’s value will appreciate at a steady 2.5% quarterly clip from March 2027 onward — roughly 10.4% compounded annually. You’ll be hard-pressed to find a 30-year window in private equity history in which quarterly marks were positive in every single quarter.

Hamilton Lane says “It’s important to note that we have a well-diversified business, providing solutions and services for a wide range of investors across the globe. If your calculation here was to simply remove FRPR, that would provide an inaccurate picture.” And in Hamilton Lane’s defense, many of its most aggressive practices have become the industry standard. But whether this means the practices are reasonable — or the private equity industry, on the whole, is more exposed in the event of redemptions than is widely understood — is the key question.

And Hamilton Lane’s practices are already starting to show some cracks. Funds that rely on day-one markups benefit from new money to buy more discounted assets, which creates more day-one markups, which keeps the reported performance high. But as the fund swells, the impact of new money — and, consequently, new day-one markups — is diluted, perhaps explaining why PAF’s performance has begun to sag.

Annual returns have compressed from 20.8% in fiscal 2022, when the fund managed $330 million, to 12.6% in fiscal 2025, when it managed $3.6 billion — a 10-fold increase in assets accompanied by a near-halving of returns. The since-inception figure of roughly 16% — which Hamilton Lane cited in its comment to Hunterbrook — is heavily weighted by those strong early years.

And, critically, Hamilton Lane hasn’t faced the pressure of forced liquidations. As of last year, money was still pouring into PAF: The fund reported about $146 million per month in average gross inflows during the first half of fiscal 2026, with $878 million in subscriptions against just $79 million in redemptions over that six-month period — an 11-to-1 ratio that is, by any standard, healthy. PAF today is not BREIT in December 2022. But that strength is also its primary vulnerability.

The entire model — the day-one markups, the FRPR, the reported IRR, the premium multiple the stock still commands — depends on a relentless stream of new money. Hamilton Lane’s next earnings report, scheduled for May 21, will give investors the first clean look at whether the ratio is holding. The math changes fast once it slows.

And the first sign that it may be slowing was revealed as this article was going to print. Public data from Hamilton Lane’s Global Private Assets Fund, or GPA — another flagship evergreen vehicle with $6.6 billion in assets — suggests that in March, the fund experienced an estimated net outflow of $172 million, its largest across the data Hunterbrook was able to review.4 It was only the second month of net outflows in the 18-month window for which data is publicly available — and it was nearly nine times larger than the first, a $19 million blip in September.

GPA is a different fund than PAF, but the dynamic is the same: The model depends on inflows exceeding redemptions. March suggests that equation may be starting to shift.

The Exit Doors

If there aren’t enough inflows to absorb the redemptions, then Hamilton Lane does have options—but none of them are good. They could use cash on hand to repay investors. They could add debt. They could tell investors they can’t have their money back, as multiple funds have done recently. Or they could start selling assets, thereby potentially triggering that vicious circle.

As Hamilton Lane itself warns in its fine print: “In a declining market, our evergreen vehicles may experience declines in value, and the pace of redemptions and consequent reduction in our assets under management could accelerate. Such declines in value may be both provoked and exacerbated by forced selling of assets, as further described below. Actions taken to meet substantial redemption requests could result in a material adverse effect on the fund’s investments, ability to make new investments or ability to achieve its investment objectives.”

And if Hamilton Lane starts seeing redemptions, it might take a long time to restore its brand.

“I don’t think memories are going to be short,” Dawn Fitzpatrick, the chief investment officer of Soros Fund Management, said in a recent interview about some of the practices she sees across the industry. “There’s going to be a culling of the alternative asset managers.”

Whether Pandora’s Box can be closed before the culling begins remains perhaps the industry’s most expensive question.

AUTHORS

Bethany McLean is the investigative journalist who exposed the notorious Enron fraud while a reporter at Fortune. She is a contributing editor at Vanity Fair who authored The Smartest Guys in the Room and several other books. She began her career as an investment banking analyst at Goldman Sachs before moving into journalism.

JD Jean-Jacques joined Hunterbrook from Goldman Sachs, where he worked as an investment banker. He was editor-in-chief of Howard University’s newspaper, The Hilltop, and wrote for The Exonian at Phillips Exeter Academy. Among other recognitions, he was a White House Correspondents’ Association scholar and was selected as student journalist of the year by The National Association of Black Journalists. He graduated from Howard with a B.A. in history.

Matthew Termine is a lawyer with nearly five years of experience leading the legal team at a mortgage technology company. In 2017, Matt was credited by the Wall Street Journal, among others, for identifying suspicious mortgage loan transactions that led to several successful criminal prosecutions, including that of a prominent political operative and the chief executive officer of a federally chartered bank. He is a graduate of Trinity College and Fordham University School of Law.

Editors

Jim Impoco is the award-winning former editor-in-chief of Newsweek who returned the publication to print in 2014. Before that, he was executive editor at Thomson Reuters Digital, Sunday Business Editor at The New York Times, and Assistant Managing Editor at Fortune. Jim, who started his journalism career as a Tokyo-based reporter for The Associated Press and U.S. News & World Report, has a Master’s in Chinese and Japanese History from the University of California at Berkeley.

Hunterbrook Media publishes investigative and global reporting — with no ads or paywalls. When articles do not include Material Non-Public Information (MNPI), or “insider info,” they may be provided to our affiliate Hunterbrook Capital, an investment firm which may take financial positions based on our reporting. Subscribe here. Learn more here.

Please contact ideas@hntrbrk.com to share ideas, talent@hntrbrk.com for work opportunities, and press@hntrbrk.com for media inquiries.

LEGAL DISCLAIMER

© 2026 by Hunterbrook Media LLC. When using this website, you acknowledge and accept that such usage is solely at your own discretion and risk. Hunterbrook Media LLC, along with any associated entities, shall not be held responsible for any direct or indirect damages resulting from the use of information provided in any Hunterbrook publications. It is crucial for you to conduct your own research and seek advice from qualified financial, legal, and tax professionals before making any investment decisions based on information obtained from Hunterbrook Media LLC. The content provided by Hunterbrook Media LLC does not constitute an offer to sell, nor a solicitation of an offer to purchase any securities. Furthermore, no securities shall be offered or sold in any jurisdiction where such activities would be contrary to the local securities laws.

Hunterbrook Media LLC is not a registered investment advisor in the United States or any other jurisdiction. We strive to ensure the accuracy and reliability of the information provided, drawing on sources believed to be trustworthy. Nevertheless, this information is provided “as is” without any guarantee of accuracy, timeliness, completeness, or usefulness for any particular purpose. Hunterbrook Media LLC does not guarantee the results obtained from the use of this information. All information presented are opinions based on our analyses and are subject to change without notice, and there is no commitment from Hunterbrook Media LLC to revise or update any information or opinions contained in any report or publication contained on this website. The above content, including all information and opinions presented, is intended solely for educational and information purposes only. Hunterbrook Media LLC authorizes the redistribution of these materials, in whole or in part, provided that such redistribution is for non-commercial, informational purposes only. Redistribution must include this notice and must not alter the materials. Any commercial use, alteration, or other forms of misuse of these materials are strictly prohibited without the express written approval of Hunterbrook Media LLC. Unauthorized use, alteration, or misuse of these materials may result in legal action to enforce our rights, including but not limited to seeking injunctive relief, damages, and any other remedies available under the law.

Fee-related earnings are taken as a percentage of management and advisory fees.

Methodology: Same-quarter markup analysis was performed using data extracted from quarterly SEC filings (N-PORT and N-CSR reports) filed by Hamilton Lane-managed funds with the Securities and Exchange Commission. For each quarterly reporting period, individual investment positions were identified as "newly acquired" if the acquisition date recorded in the filing fell within the same calendar quarter as the filing's period-end date. For each such newly acquired position, the difference between reported fair value and cost basis (fair value minus cost) was calculated. These amounts were aggregated to determine the total gain attributable to same-quarter markups in each period. This aggregate was then compared to the total sequential quarterly gain across the fund's investment portfolio to derive the percentage of period returns attributable to same-quarter marking of new investments. Cumulative percentages reflect the sum of same-quarter markup gains divided by total cumulative sequential gains across all periods analyzed.

Beginning in the fourth quarter of fiscal 2025, Hamilton Lane modified its definition of Fee Related Earnings (FRE) to exclude equity-based compensation from expenses and include fee-related performance revenues (FRPR) in revenue. Prior period amounts were restated to reflect the new definition. We computed FRE under both the old and new definitions for the nine months ended December 31, 2025 and 2024, using figures from the company’s 10-Q for the quarterly period ended December 31, 2025. Under the new definition (as reported), FRE for the nine months ended December 31, 2025 was $254.6 million, compared to $186.1 million in the prior year period, which reflects growth of approximately 37%. To reconstruct FRE under the old definition, we added equity-based compensation back to expenses and removed FRPR from revenues. For the nine months ended December 31, 2025: $254.6 million minus $77.7 million (FRPR) minus $38.1 million (equity-based compensation) = $138.7 million. For the nine months ended December 31, 2024: $186.1 million minus $1.2 million (FRPR) minus $19.7 million (equity-based compensation) = $165.2 million. Under the old definition, FRE would have declined approximately 16% year-over-year.

Calculation of March 2026 inflows/outflows for Hamilton Lane Global Assets Fund: $6.79b AUM (3/1/2026) - $6.55b AUM (3/31/26) = $240m; 3/31/26 MTD share class performance: -1.10%; 1.10% of $6.79b of AUM (as of 3/1/2026) is $68m; the AUM decreased by $240m in March 2026, $68m of which relates to performance of the underlying assets and $172m of which relates to outflows/redemptions.