What Lennar Owes

The homebuilder spends billions to reserve land it used to own. $LEN counts these fees as an asset, but the bill is coming due. Is Lennar cutting corners on home quality to save vanishing margins?

By: Sam Koppelman, Jenny Ahn, Matthew Termine, Alex Sternlicht, Michelle Cera

Editor: Jim Impoco

Hunterbrook Media’s investment affiliate, Hunterbrook Capital, has no positions related to this article at the time of publication. Positions may change at any time. See full disclosures on our website.

Something doesn’t add up at Lennar ($LEN), America’s second-largest homebuilder.

The numbers are bad: Margins have cratered, cash flow has dwindled, and the stock has crashed.

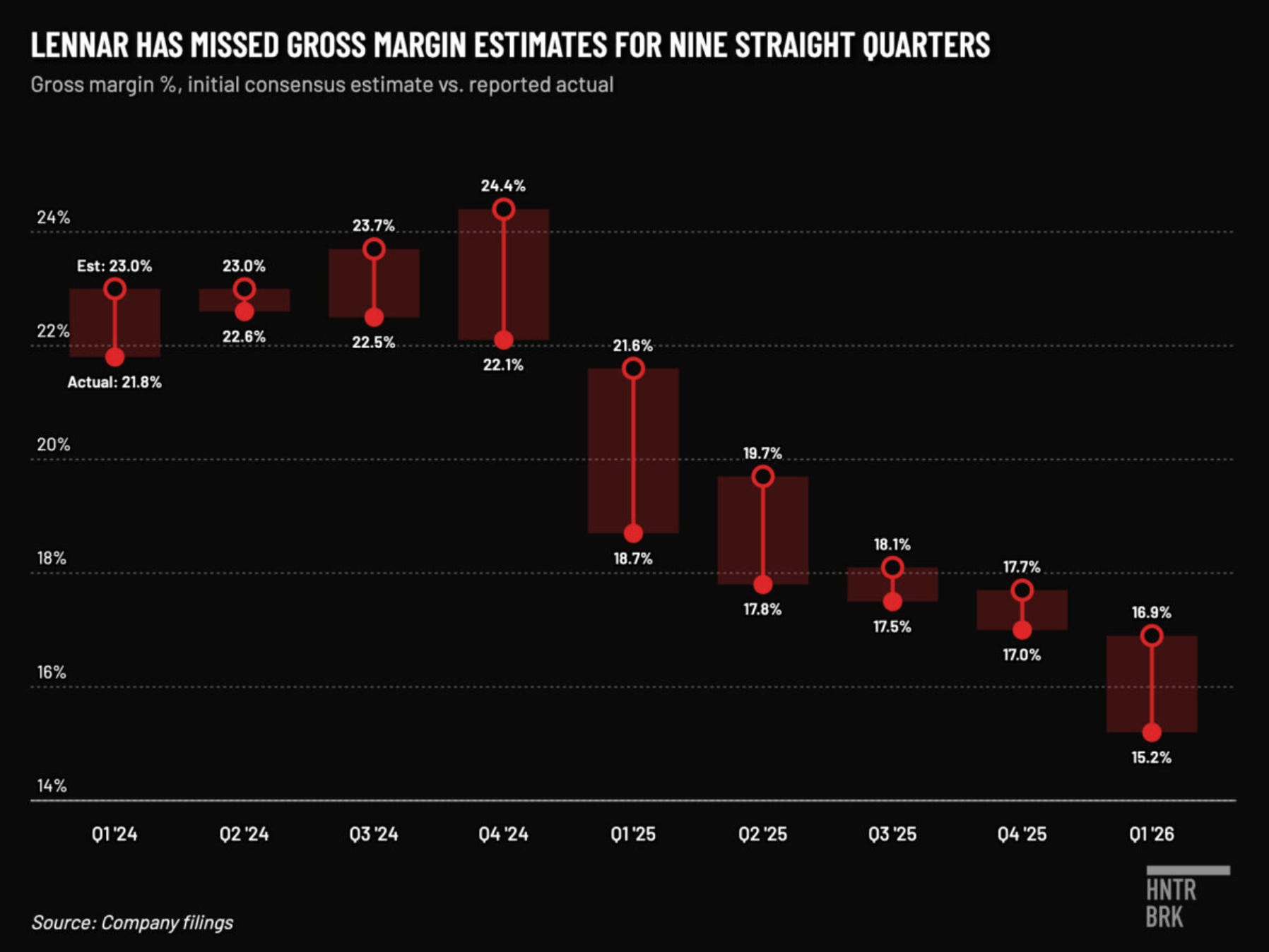

But it isn’t just that the numbers are bad — it’s that they are surprisingly bad. For 10 straight quarters, Lennar’s stock fell the day after reporting earnings.1 Wall Street keeps modeling the company’s financials, and keeps getting it wrong.

So what is everybody missing?

Lennar itself raised this question in a statement released around noon yesterday that appeared random to observers of the name — framed as a response to “several analysts and investors” asking the company about its strategy. The contents of the press release were anodyne, but the stock fell to multiyear lows within hours.

“If you’re explaining, you’re losing,” wrote analysts at Evercore in a research note about $LEN.

What Lennar did not mention: Hunterbrook had repeatedly reached out to the company since last week with specific, detailed questions about its accounting and financials. Lennar — which in its statement claimed to be “deeply committed to engaging with investors, analysts, and all stakeholders — ghosted that outreach.

Hunterbrook wrote Lennar again after the statement on Monday. Lennar’s response: Nada. The only answers to Hunterbrook’s questions Lennar provided seemed to be selectively disclosed to analysts at banks, rather than the public. (The corporate equivalent of responding to rumors on your Close Friends story.)

Lennar’s narrative: Its numbers have been disappointing because of soft demand and aggressive discounting amid a widespread housing downturn. Lennar famously slashed home prices further than any peer, a bet on volume over margins that management framed as a deliberate strategy. The company reiterated that margin impact is largely a reflection of the volume-based strategy defended in yesterday’s statement.

But if Lennar’s strategy is working, why the carnage?

Specifically, why has Lennar consistently tripped over Wall Street’s gross margin projections every quarter since 2023? Is it really just the discounting?

To solve this mystery of the vanishing margins and immense cash burn, Hunterbrook Media analyzed proprietary national real estate data, hidden variables across SEC filings, and obscure documents from Lennar counterparties — including the pitch decks that Lennar’s financing partner, Angelo Gordon, presented to a California county pension fund.2 We also spoke with multiple independent accounting experts, investment analysts, a land banker, and investors who have combed through Lennar’s financials.

The evidence pointed Hunterbrook toward an explanation so buried in the books it seems that many of those covering Lennar missed it.

The homebuilder last year completed an ambitious transformation: moving 98% of its pre-construction land off its books and into third-party “land banks.” Executives projected this “land-light” strategy would cost just 1 percentage point of gross margin.

But Hunterbrook’s analysis indicates Lennar’s pivot to land banking has locked the company into paying Wall Street firms more than $2 billion a year in annual fees just to maintain options on land it used to own, according to Hunterbrook’s estimates. That figure now rivals the company’s entire net income.

These fees are generally paid monthly or accrued over time until Lennar takes delivery of the properties. Either way, most fees seemingly aren’t immediately showing up as expenses. Instead, Lennar appears to be capitalizing some of these disbursements — recording billions in accumulated spending as though it is an asset.

“It’s delaying the inevitable,” said JP Krahel, chair of Loyola University Maryland’s accounting department. “Seems a little nuts.”

The costs have already begun to creep into margins, though they appear to be masked by aggressive cuts to construction expenses. But the worst is likely still ahead for Lennar. The land bank portfolio has grown every year since 2020, and the average lot likely sits in the bank for roughly two years before Lennar takes delivery.3

That means the income statement today seemingly reflects only the earlier, smaller vintages of land bank deals.

The later vintages — carrying years of accumulated fees — haven’t hit yet. And Lennar’s sales pace suggests some of the land is sitting in the banks significantly longer than originally planned, silently accruing fees until Lennar takes delivery.

In the meantime, Lennar’s leadership appears to be heading for the exits. The co-CEO, general counsel, head of IR, and several other executives, including ones tied closely to land-banking, have recently departed.

“A number of long-term Lennar associates have chosen to retire … and let the next generation shine,” said CEO Stuart Miller, who has been dropping guarded hints about how expensive the land deals have been. The asset-light transformation, he told analysts on the most recent call, is “getting more interesting by the day.”

“Interesting” is likely not the word Lennar homeowners would use to describe what has happened to their homes during the company’s push to save money wherever it can. In 2025, Hunterbrook published an investigation into quality issues from Lennar and other homebuilders — ranging from severe mold infestations to cracked foundations to violations of building codes, according to interviews with 22 Lennar homeowners.

“It’s like they give you the impression that they’re rapidly building because they have such a high demand,” a Lennar homeowner who asked to be referred to only by her last name, Marks, told Hunterbrook. She said Lennar sold her a “lemon” home full of defects in 2024. “Then once you buy and move in, you realize nobody’s moving into those other homes.”

Those empty homes may be signs of a broken business model.

The industry affectionately called Lennar’s volume-based growth engine the “Lennar Machine.” But the machine has become a treadmill that Lennar no longer controls: The company appears to be churning out more and more homes from the option pipeline to stop the fees from accruing while the land sits in the bank. But in order to sell these homes in a weak housing market, Lennar is slashing effective prices, inclusive of incentives, destroying margins already buckling under the weight of the fees.

It’s a lose-lose for both Lennar and for the people like Marks surrounded by empty lots, watching their home values — and the stock price of the company that sold them the dream — plummet.

How’d Lennar get here?

The Big Bet

Lennar no longer owns the land it plans to build on — not until the moment it’s ready to start construction.

Over the past seven years, the company has executed on an extreme version of a big bet made by many major homebuilders — selling or transferring nearly all of the land it once owned to land developers or financial firms. In place of the land itself, Lennar contracted with these firms for options to purchase land. With remarkable speed, Lennar pulled off this “land light” strategy, going from owning roughly 75% of its land in the fourth quarter of 2018 to just 2% in the fourth quarter of 2025, with the rest controlled through options.

Optioning land allows homebuilders to free up massive amounts of capital that would otherwise be tied up with owned land. By keeping these properties in what is called a “land bank,” builders can secure a pipeline of land to buy when they need it, just in time for home construction. They don’t have to own all that land while they develop it or wait until the market is right.

Experts told Hunterbrook that the idea was to make Lennar’s balance sheet look more like that of NVR ($NVR), a smaller rival that Wall Street rewards with a higher multiple for keeping its books light. In March 2025, Miller told investors the land-light strategy would only carry a cost of roughly 100 basis points, or 1 percentage point, of margin — a small price to pay for a Wall Street makeover and attendant higher valuation.

But that’s not what happened.

Unlike NVR, which options land from local developers in a network that took decades to build, Lennar wanted a faster, more institutional setup. It turned to private equity firms like TPG’s Angelo Gordon and spun off its legacy land into a real estate investment trust (REIT) named Millrose Properties ($MRP). Miller called the company’s transition “a strategic national process,” though he later admitted, “We’ve put these things together pretty quickly.”

The main issue is that institutional land banks aren’t cheap. First, Lennar pays those firms deposits — about 5% to 20% of the land’s value — pretty standard for builders who option land from developers.

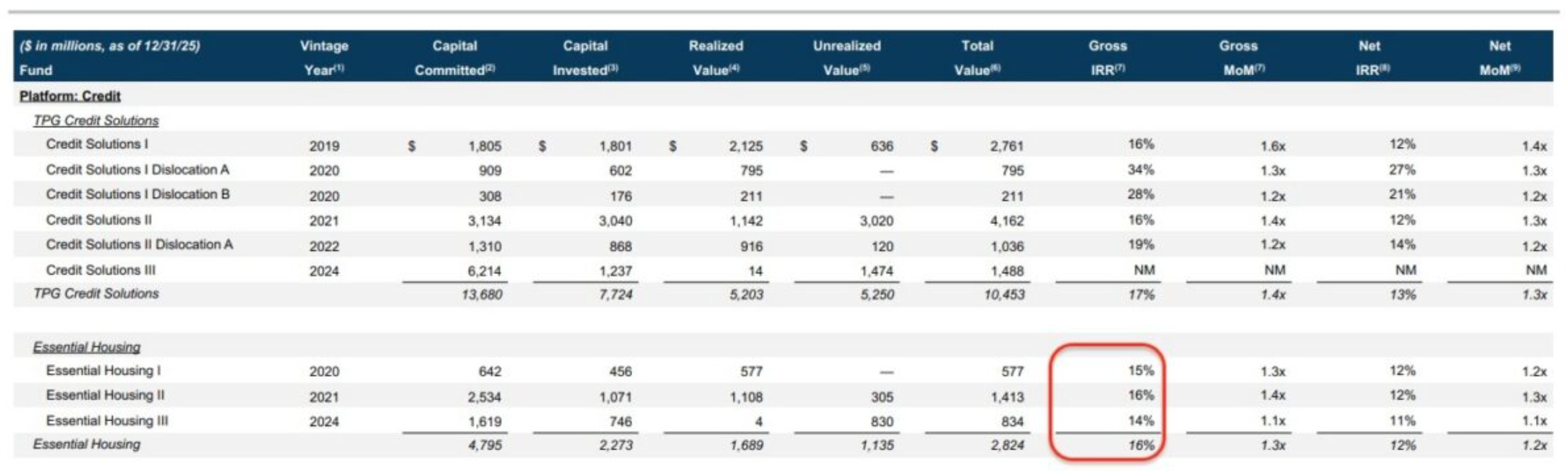

Second, what’s notable about the institutional land banks that Lennar borrows from is that they also charge option fees, which essentially amount to interest payments. To Millrose, Lennar pays an average of 8.5% annually. The number is likely higher for other counterparties like Angelo Gordon, which reported a 15% internal rate of return on its first Lennar land bank, according to a document obtained by Hunterbrook.

Contrast this with the NVR model Lennar seems to be emulating. NVR largely enters into land purchase contracts with developers for finished lots and pays a one-time deposit at roughly 10% of the land’s purchase price, which goes toward the principal. And the company doesn’t appear to pay recurring option fees. Which means, essentially, NVR’s cost to option land beyond interest is simply the impairment write-downs of the initial deposit if the builder decides not to purchase the land. In all of 2025, NVR paid $75.9 million total in impairments, nowhere near the amount Lennar may owe in fees.

Hunterbrook estimates those option fees will cost Lennar billions annually upon maturity, rivaling the company’s entire net income.4 The 1-percentage-point margin drag management promised appears to be way off.

Delaying the Inevitable

There seem to be two ways Lennar pays option fees. 1) With Millrose, Lennar pays in regular monthly installments — 8.5% on the value of the finished land. 2) With Angelo Gordon, the deals may be structured more like a PIK loan5 — with the option fees rolling into the purchase price when Lennar finally takes delivery of the lot, or when Lennar abandons the project, according to Angelo Gordon’s pitch decks, master agreement, and a video of Angelo Gordon’s presentation to a California county pension fund in 2024.6

It’s not clear precisely how these deals work, as the details surrounding them are largely kept private. But Hunterbrook’s reporting suggests this structure enables Lennar to pull off an accounting two-step.

During the period in which Lennar is paying out options fees, the company does not appear to expense them. Instead, Lennar seems to be parking these costs on the balance sheet under “deposits and pre-acquisition costs” until they purchase the lot — or take an impairment on it if they decide to walk — at which point these expenses eventually flow through to Lennar’s COGS.

This approach — which may be perfectly legal! — enables Lennar to present better earnings today, at the expense of worse COGS tomorrow.

Why do we think this?

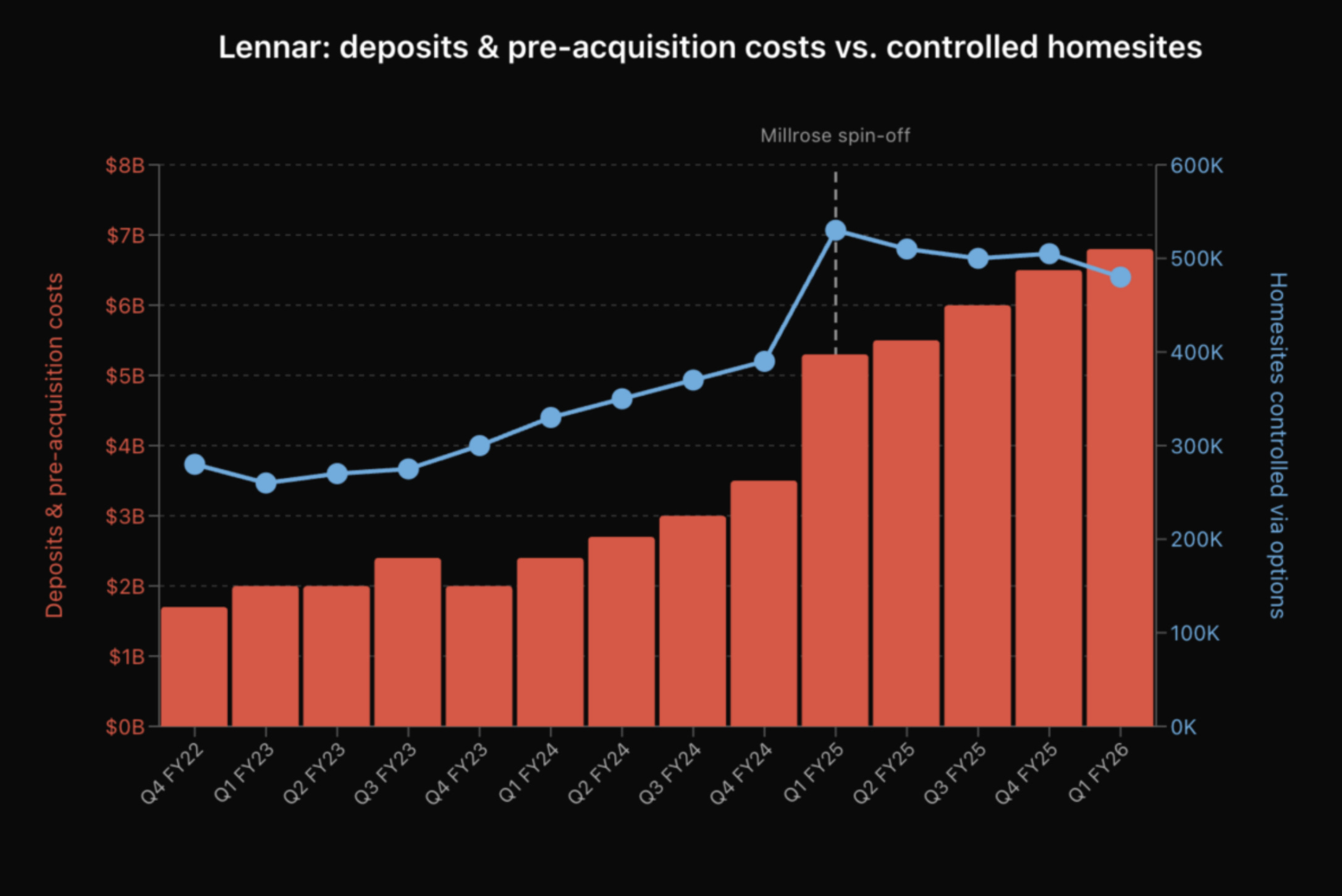

One seemingly reasonable assumption is that if the deposit and pre-acquisition costs line really reflects money Lennar puts down to genuinely purchase land, then deposits would rise and fall roughly in step with the number of homesites Lennar controls. More land, more deposits and pre-acquisition costs. Less land, fewer deposits and pre-acquisition costs.

That’s how it works at NVR, the company Lennar reportedly models itself after. Its deposits track homesites almost perfectly. Over the course of 2025, NVR’s controlled homesites ranged from 155,000 to 169,250. Its deposit line moved roughly in lockstep: from $727 million to $851 million, holding steady at roughly $4,700 to $5,000 per homesite. No mystery.

At Lennar, the two numbers have decoupled.

Between February 2025 and February 2026 — the four quarters following the Millrose spinoff — Lennar’s controlled homesites fell by roughly 47,000, from 533,000 to 486,000. At Lennar’s average deposit and pre-acquisition costs — of roughly $12,900 per homesite as of November 2025 — that reduction theoretically should have pulled the deposit line down by approximately $600 million.

Instead, the deposit line grew by $1.6 billion — from $5.2 billion to $6.8 billion.

That’s a $2.2 billion gap between what the deposit line theoretically “should” have done and what it actually did. Even accounting for normal churn — Lennar continuously options new land to replace lots it takes down — a gap of that magnitude points to something other than new deposits driving the growth, likely a combination of capitalized option fees, infrastructure spending, and other pre-acquisition costs. (After all, the number of homesites are down!)

Now, there may be reasonable explanations for the gap.

Lennar develops the lots while they sit in the bank. Laying roads and utilities. Grading. Permitting and entitlements. These costs could add up quickly, depending on how raw the land was when Lennar optioned it.

That’s what Evercore offered as a possible explanation: infrastructure costs. In Texas, for instance, Municipal Utility Districts (MUDs) require builders to fund infrastructure upfront and later reimburse them through bond issuances; analysts at Evercore ISI, in the note published the same day as Lennar’s statement, estimated MUD spending alone accounts for over $300 million of the deposit line’s recent growth. (Lennar’s MUDs raise their own series of questions.)

But even Evercore’s own analysis said the “concerns around capitalized” options fees are “not without merit,” noting that Lennar’s non-Millrose land bank exposure is two to three times the size of its Millrose exposure and that the margin headwind could be well above the company’s 100-basis-point estimate. Evercore called on Lennar to provide more disclosure about what’s in the line — a request the company has so far declined to fulfill, though its next SEC filing, a 10-Q, which appears to be imminent, may offer answers.

And experts who spoke with Hunterbrook believe the most plausible primary source for the unexplained billions of dollars in this line item over the years is the capitalized option fees Lennar has been paying out to its land banking partners. Lennar’s management also confirmed to at least one investor — and seemingly the sell-side — that the deposit line includes option maintenance fees.

Krahel and other accountants interviewed by Hunterbrook questioned Lennar’s approach. “I don’t capitalize an electric bill because the second I stop paying it, the lights go out,” said Krahel, the chair of the accounting department at Loyola University Maryland.

He offered a second analogy: a pawn shop. If you pay $50 a month for a shop to hold your watch, those payments don’t reduce the ultimate price you pay. “Those monthly payments don’t offset the value of the gold watch when I come buy it back,” he said. “That’s rent expense. That’s really what this is.”

The issue, Krahel explained, is that the option fees Lennar is capitalizing aren’t actually an asset. They’re not paying down principal and reflecting the value of new land ownership. They’re just expenses, like interest. The money leaves Lennar and goes to other firms. Period. He described the accounting rules governing these kinds of transactions as “fundamental principles,” but it’s unclear whether Lennar is following them.

“Generally speaking, you cannot capitalize an expenditure if you’re spending it on something you don’t control,” Krahel explained. But if Lennar indeed does “control” the properties on which it is paying management fees, Krahel argued, then that land shouldn’t be off its books. “They’re trying to eat their cake and have it too,” Krahel said. “If they control it, it should be on their balance sheet.”

To be clear: Lennar’s accounting may be permissible. Under GAAP, payments to obtain an option on real property can be capitalized, and Lennar could argue that because the fees become part of the eventual lot purchase price, they are properly recorded as pre-acquisition costs. Reasonable accountants disagree on where the line falls — and Lennar said in its statement that its disclosures and accounting treatment “have been carefully vetted.”

But the financial consequences are the same regardless of how the fees are classified.

Whether Lennar records them as an asset today or an expense today, the cash has already left the building. And when the lots are finally taken down, the accumulated cost should hits the income statement either way. The accounting treatment determines when investors see the damage — not whether the damage exists. In the meantime, reported earnings look relatively intact, the balance sheet line keeps growing, and investors are left evaluating a company that appears to earn $2.1 billion a year but is quietly spending what appears to be a comparable amount to maintain its land pipeline.

Then, when Lennar takes down a lot from a land bank, the accumulated fees don’t get paid back. They become a cost, flowing straight into cost of goods sold and cutting directly into gross margins. And if Lennar abandons a lot, it takes an impairment instead.

“You’re feeding everybody on the pathway to the takedown moment thinking everything’s better than they are,” Krahel said. “And then — hello, surprise — here are expenses that were sitting on the balance sheet instead of having flowed through the income statement.”

The Inevitable: Cost Recognition

That “surprise” is no longer theoretical. Hunterbrook’s reporting indicates that it has started to bleed onto Lennar’s income statement as the first wave of optioned lots have been taken down — even if these fees were once marked as an asset.

It’s not immediately clear where these fees show up in Lennar’s earnings, because the company does not itemize them in its cost of goods sold (COGS).

But you can roughly back into the option fees as part of those COGS — and margin hit — through a few different, if imperfect, proxies.

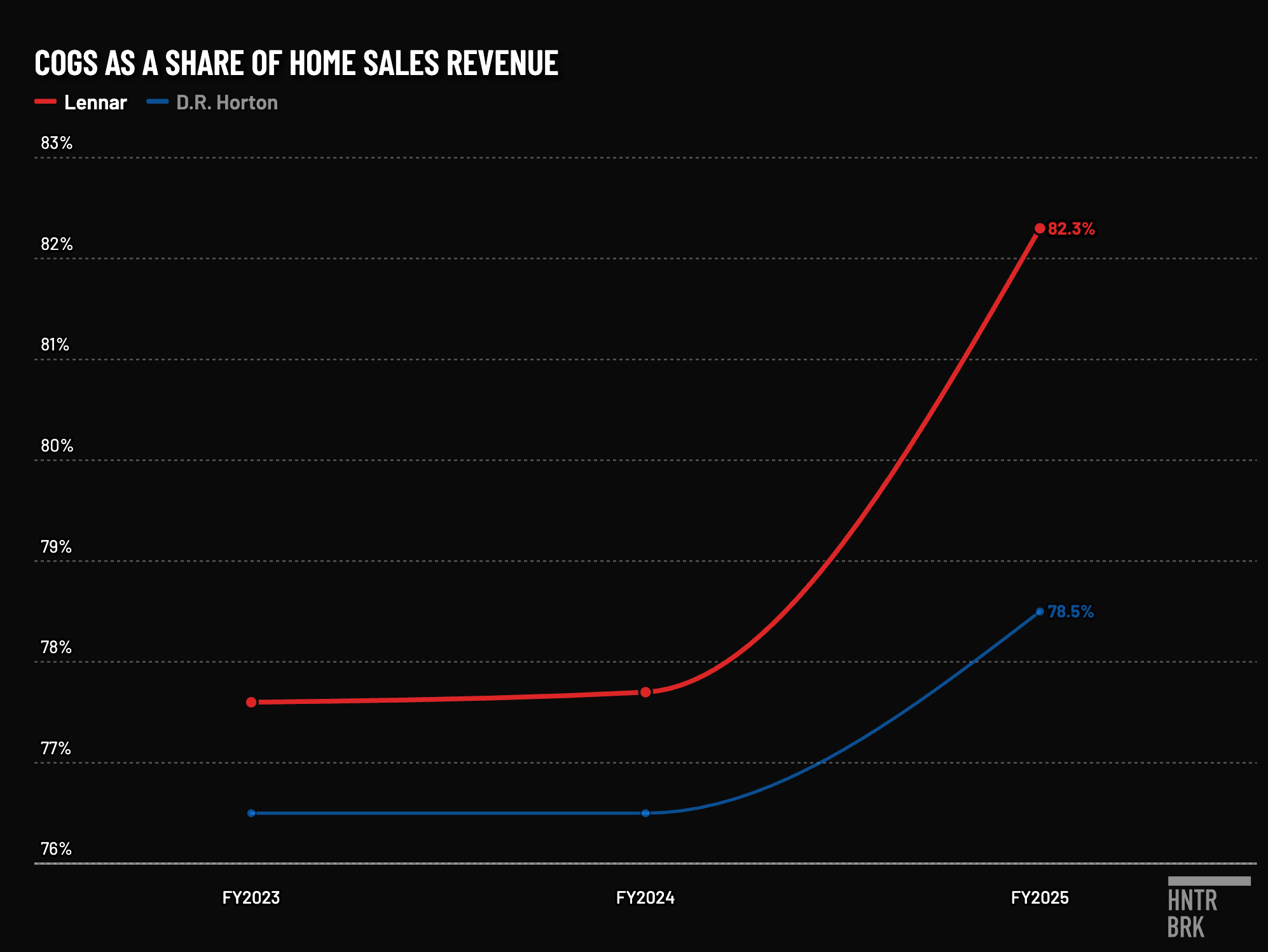

One is through a comparison with D.R. Horton.

D.R. Horton, which targets very similar buyers at around the same price points, had comparable cost structures as Lennar from from 2020 to 2022. And both companies significantly cut down on their construction costs, which, in theory, should have reduced their COGS.

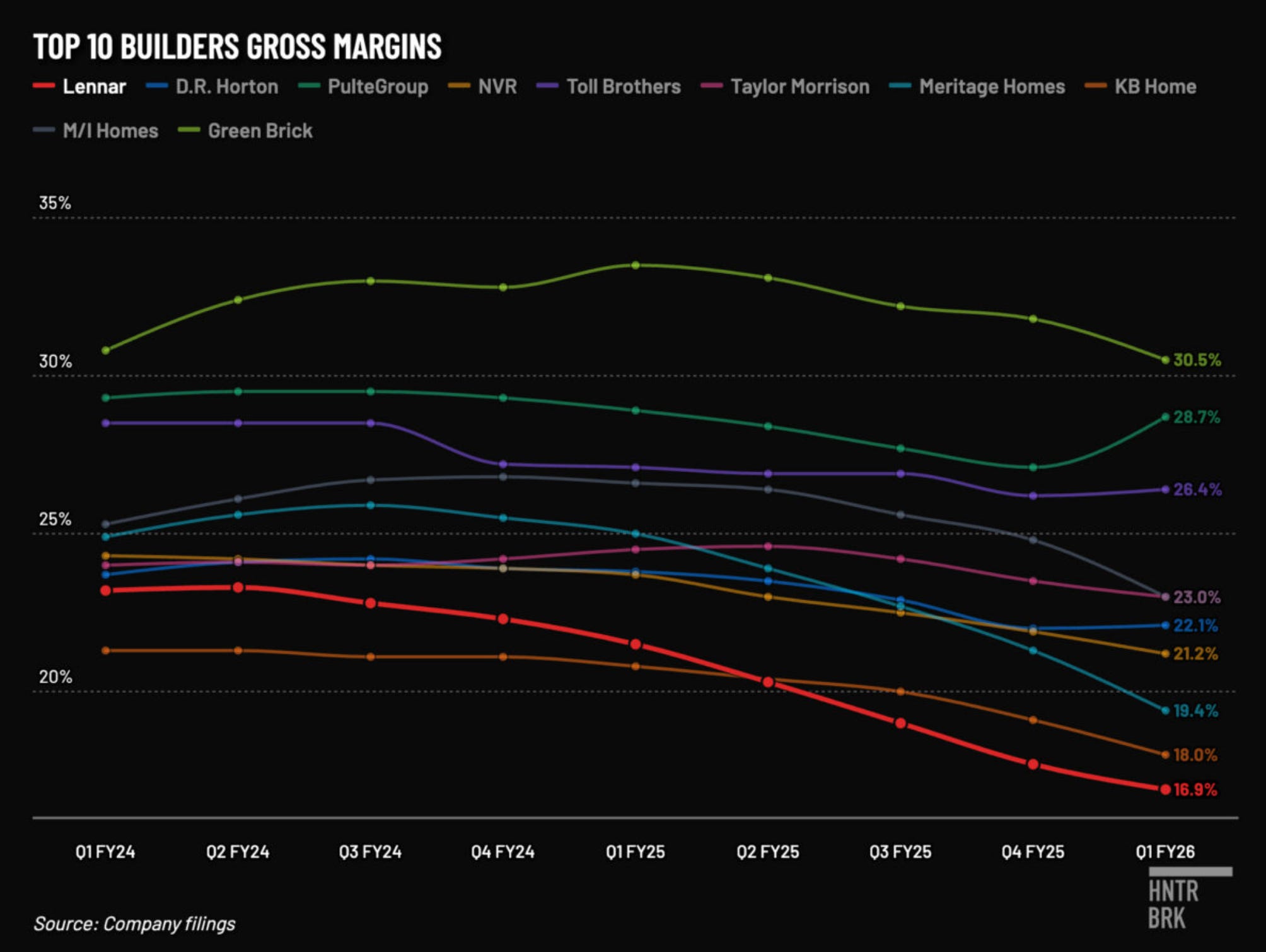

But starting in 2023, Lennar’s COGS as a share of revenue began pulling away, culminating in a roughly 2.8 percentage point gap in FY2025 — approximately $800 million to $1 billion in extra costs. That’s almost certainly a reflection of Lennar’s rising land costs, not construction costs (land and construction costs are the two most important homebuilding costs), because Lennar’s construction costs haven’t only been falling; they’ve been doing so at nearly twice the rate of D.R. Horton.7

This is, perhaps, an explanation for why Lennar appears to be among the only major homebuilders that actually almost lost money in the last 12 months.

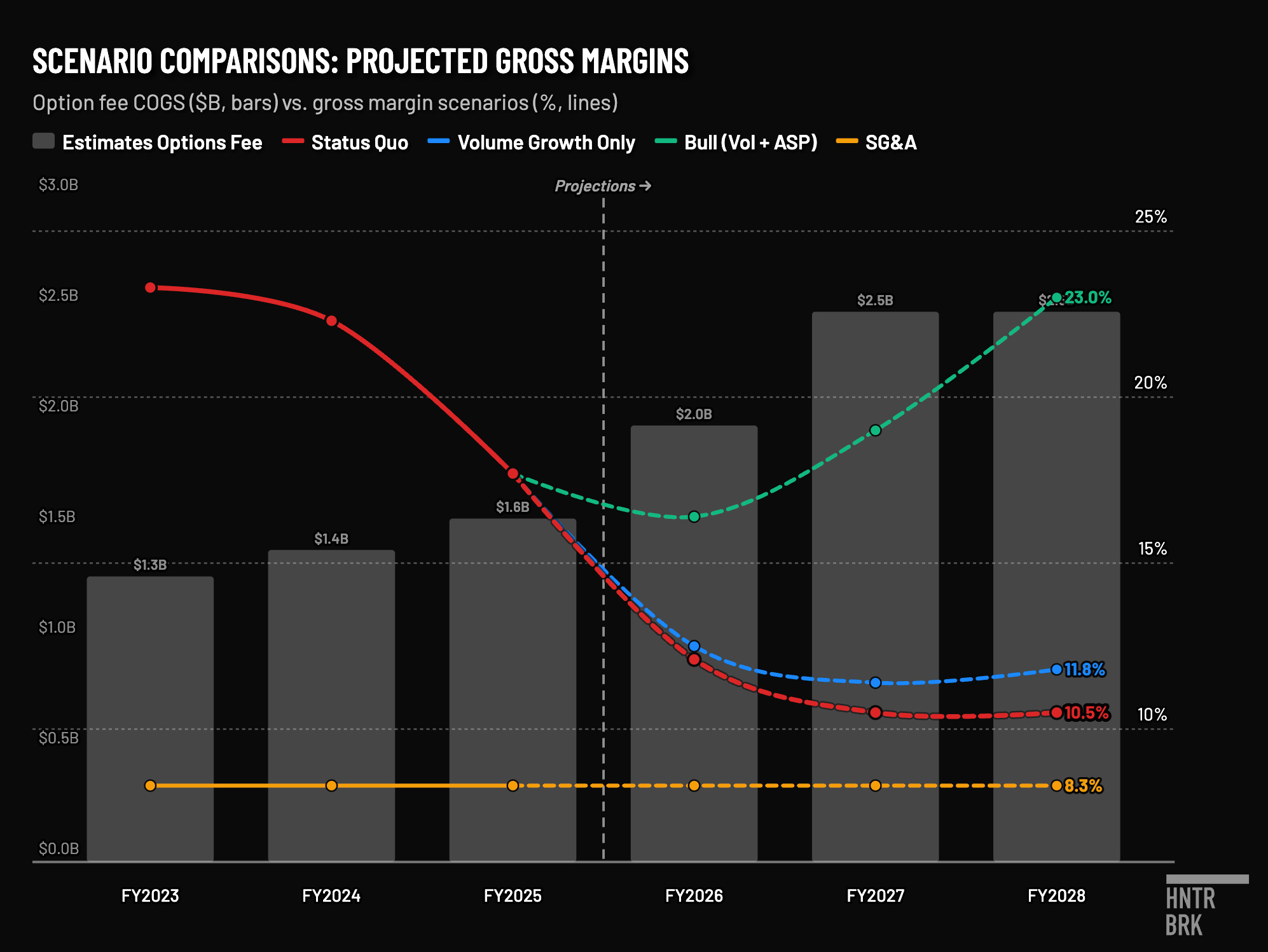

And this may only be the beginning, because much of the fees Lennar has accumulated likely haven’t reached the income statement yet. The land-bank portfolio has grown every year since FY2020, with vintages growing over time — from 119,283 controlled homesites to 496,250 by FY2025. That means, assuming Lennar’s optioned land sits roughly two years in the bank before takedown, the income statement today reflects just the carrying costs on the earlier, smaller vintages. Meaning, the large tranches optioned in recent years — including over 100,000 homesites Lennar added to its portfolio last year alone — are still accruing fees in the background.

Based on this vintage approach, Hunterbrook estimates that last year, Lennar paid about $1.5 billion in option fees, or an average of roughly $20,000 per home sold.8 In an extremely simplified calculation, Hunterbrook assumed that the option rate on all the lots was 8.5%, the rate Millrose charges — almost certainly an underestimate given the higher market rates that Lennar likely paid to third-party lenders before Millrose was created in 2025. (This model also assumes Lennar has been taking down all homesites according to schedule; it doesn’t take into account a potential reality where Lennar’s takedowns have actually skewed toward the end of the term or renegotiated past the original term — events which would add to the accrued option fees.9)

If our analysis is right, as the portfolio matures and Lennar begins taking down lots with the full weight of accumulated carry costs, option costs as share of revenue will continue to climb. By FY2028, option costs on its portfolio could be roughly $2.5 billion or more, Hunterbrook estimates, potentially bringing down margins to a level barely enough to clear Lennar’s overhead. (Note: These truly are just estimates. The company provides very little information on this, so we backed into it. If you have a better way to calculate it, let us know at ideas@hntrbrk.com.)

The upshot is Lennar may end up taking a much bigger gross margin hit than the company telegraphed when it pivoted to the land-banking model — and Lennar’s margins are already much worse than peers.

In 2025, Lennar previewed just 100 basis points of margin as the cost of optioning land. That may have been true if you were just looking at the 2024 estimated takedown numbers, reflecting a little over half of Lennar’s current portfolio. Option fees net of the cost of owning land — using its corporate debt rate of around 5% as a proxy — would have gotten you close to that 100 bps spread. But by the time Lennar’s current portfolio matures, that spread will have increased to 300 bps, we estimate.

And while a few hundred basis points doesn’t sound like much — a small price to pay for the perks of a land-light strategy, an easily absorbable margin cost if you can keep your sales prices and volume pace healthy — that doesn’t tell the whole story.

The fundamental problem with Lennar’s new model is that slowing down has gotten much more expensive. When Lennar owned its land, the cost of delaying construction was roughly 5% interest. Now it’s at least 8.5% — and the land bank contracts don’t wait. Lennar seemingly had to renegotiate as much as $2.4 billion worth of options last year, and was “compelled to takedown” an additional $663 million from option land in 2025 — even as it sat on roughly 5,000 completed homes it couldn’t sell, a 72% increase from the year before.10 To move those homes, Lennar has needed to slash prices, squeezing margins already buckling under the option costs.

Stijn Van Nieuwerburgh — a real estate and finance professor at Columbia Business School — described the model to Hunterbrook as involving layered, and partly hidden, leverage. On the balance sheet, he argued, a “land-light” strategy can look less risky, but the economic exposure can end up resembling the older model that homebuilders such as Lennar are trying to move away from.

“It’s leverage on top of leverage,” Van Nieuwerburgh said. “In an upcycle, leverage helps you; in a downcycle, it can be devastating.”

“The optionality is supposed to reduce risk. But if the contracts embed enough financing and enough effective commitments, it can end up doing less risk reduction than advertised.”

But Lennar can renegotiate or walk, right? Isn’t that the point of the “land-light” model?

At least according to the terms Hunterbrook reviewed, there doesn’t seem to be a lot of wiggle room built into Lennar’s arrangement — although “flexibility” was supposed to be a key feature of the land-light structure.

Lennar’s portfolio with Millrose is based on a “cross-termination pooling” structure that keeps Lennar from being able to walk away from a bad community in one geography without triggering forfeitures across an entire pool of communities. Meaning, Lennar likely has to sit on optioned lots for a long time in markets where it makes little sense to start building — say in Florida, where home prices have dropped as much as 16% in some parts.

Angelo Gordon deals don’t look much more flexible for Lennar either.

According to Angelo Gordon’s pitch decks, the project cycle is limited to a 40-month period where Lennar has to takedown a certain number of lots each month on a rigid schedule. If Lennar falls behind that schedule, Angelo Gordon has the right to immediately terminate, keep the deposit, and sell the fully improved lots to a competing builder.

“There’s really no flexibility,” Angelo Gordon managing director Bryan Rush assured SBCERA, San Bernardino County employee’s pension fund, in 2024. SBCERA later approved a $150 million investment in Angelo Gordon’s land bank.

Angelo Gordon’s leash?

Angelo Gordon considers Lennar’s 19.9% upfront deposit — nearly twice the 10% Millrose charges — “first loss,” meaning Lennar’s deposit would take the first hit if deals go south. It’s another way Angelo Gordon seems to protect its downside, while leaving Lennar with the risks of forfeiting the entire deposit if projects stall, according to Angelo Gordon’s pitch to the pension fund.

And, presumably, those protections really matter for California. Because that state has seen what can happen when it doesn’t have them.

In January 2007, the massive state pension fund CalPERS invested roughly $970 million for a 62% financial interest in a Lennar land venture near Los Angeles.

Seventeen months later, the joint venture filed Chapter 11 bankruptcy. CalPERS lost its investment: $922 million, one of the worst single losses in the pension fund’s history.

Today, Angelo Gordon is channeling money from another California public pension fund, SBCERA, to fund the Lennar land acquisition.

But this time, in the event of a crisis, it seems like the role of bagholder would be reversed. It is Lennar, not the pension fund, that posted the first-loss deposit.

Asked how she would feel if Lennar had to take billions worth of impairments on its land bank investments, Marks — the resident who claims she was sold a “lemon” by Lennar — was blunt.

“Good,” she said, “lose money, like the rest of us homeowners.”

Authors

Jenny Ahn joined Hunterbrook after serving many years as a senior analyst in the US government. She is a seasoned geopolitical expert with a particular focus on the Asia-Pacific and has diverse overseas experience. She has an M.A. in International Affairs from Yale and a B.S. in International Relations from Stanford. Jenny is based in Virginia.

Matthew Termine is a lawyer with nearly five years of experience leading the legal team at a mortgage technology company. In 2017, Matt was credited by the Wall Street Journal, among others, for identifying suspicious mortgage loan transactions that led to several successful criminal prosecutions, including that of a prominent political operative and the chief executive officer of a federally chartered bank. He is a graduate of Trinity College and Fordham University School of Law.

Sam Koppelman is a New York Times best-selling author who has written books with former United States Attorney General Eric Holder and former United States Acting Solicitor General Neal Katyal. Sam has published in the New York Times, Washington Post, Boston Globe, Time Magazine, and other outlets — and occasionally volunteers on a fire speech for a good cause. He has a B.A. in Government from Harvard, where he was named a John Harvard Scholar and wrote op-eds like “Shut Down Harvard Football,” which he tells us were great for his social life.

Alexandra Sternlicht is an award-winning journalist and Columbia Business School MBA candidate. She previously reported on technology at Fortune, where her investigations were cited by the U.S. Supreme Court, lawmakers and major media outlets. She’s also worked at Forbes and The New York Times. Alexandra is an alum of Columbia Journalism School’s Knight-Bagehot Fellowship and graduated magna cum laude from the University of Pennsylvania.

Michelle Cera trained as a sociologist specializing in digital ethnography and pedagogy. She completed her PhD in Sociology at New York University, building on her Bachelor of Arts degree with Highest Honors from the University of California, Berkeley. She has also served as a Workshop Coordinator at NYU’s Anthropology and Sociology Departments, fostering interdisciplinary collaboration and innovative research methodologies.

Editor

Jim Impoco is the award-winning former editor-in-chief of Newsweek who returned the publication to print in 2014. Before that, he was executive editor at Thomson Reuters Digital, Sunday Business Editor at The New York Times, and Assistant Managing Editor at Fortune. Jim, who started his journalism career as a Tokyo-based reporter for The Associated Press and U.S. News & World Report, has a master’s in Chinese and Japanese History from the University of California at Berkeley.

Graphic

Dan DeLorenzo is a creative director with 25 years reporting news through visuals. Since first joining a newsroom graphics department in 2001, he has built teams at Bloomberg News, Bridgewater Associates, and the United Nations, and published groundbreaking visual journalism at The Wall Street Journal, Associated Press, The New York Times, and Business Insider. A passion for the craft has landed him at the helm of newsroom teams, on the ground in humanitarian emergencies, and at the epicenter of the world’s largest hedge fund. He runs DGFX Studio, a creative agency serving top organizations in media, finance, and civil society with data visualization, cartography, and strategic visual intelligence. He moonlights as a professional sailor working toward a USCG captain’s license and is a certified Pilates instructor.

Hunterbrook Media publishes investigative and global reporting — with no ads or paywalls. When articles do not include Material Non-Public Information (MNPI), or “insider info,” they may be provided to our affiliate Hunterbrook Capital, an investment firm which may take financial positions based on our reporting. Subscribe here. Learn more here.

Please contact ideas@hntrbrk.com to share ideas, talent@hntrbrk.com for work opportunities, and press@hntrbrk.com for media inquiries.

LEGAL DISCLAIMER

© 2026 by Hunterbrook Media LLC. When using this website, you acknowledge and accept that such usage is solely at your own discretion and risk. Hunterbrook Media LLC, along with any associated entities, shall not be held responsible for any direct or indirect damages resulting from the use of information provided in any Hunterbrook publications. It is crucial for you to conduct your own research and seek advice from qualified financial, legal, and tax professionals before making any investment decisions based on information obtained from Hunterbrook Media LLC. The content provided by Hunterbrook Media LLC does not constitute an offer to sell, nor a solicitation of an offer to purchase any securities. Furthermore, no securities shall be offered or sold in any jurisdiction where such activities would be contrary to the local securities laws.

Hunterbrook Media LLC is not a registered investment advisor in the United States or any other jurisdiction. We strive to ensure the accuracy and reliability of the information provided, drawing on sources believed to be trustworthy. Nevertheless, this information is provided “as is” without any guarantee of accuracy, timeliness, completeness, or usefulness for any particular purpose. Hunterbrook Media LLC does not guarantee the results obtained from the use of this information. All information presented are opinions based on our analyses and are subject to change without notice, and there is no commitment from Hunterbrook Media LLC to revise or update any information or opinions contained in any report or publication contained on this website. The above content, including all information and opinions presented, is intended solely for educational and information purposes only. Hunterbrook Media LLC authorizes the redistribution of these materials, in whole or in part, provided that such redistribution is for non-commercial, informational purposes only. Redistribution must include this notice and must not alter the materials. Any commercial use, alteration, or other forms of misuse of these materials are strictly prohibited without the express written approval of Hunterbrook Media LLC. Unauthorized use, alteration, or misuse of these materials may result in legal action to enforce our rights, including but not limited to seeking injunctive relief, damages, and any other remedies available under the law.

This includes the quarters from the end of 2023 through 2025. After Lennar reported earnings in the first quarter of 2026, its stock initially popped, before selling off again.

The San Bernardino County Employees’ Retirement Association (SBcera), a California county pension fund, invested in Angelo Gordon’s Essential Housing Fund, which warehouses land for Lennar. As a public entity, SBcera’s investment committee meetings and materials are publicly accessible. Hunterbrook reviewed the pitch Angelo Gordon presented to SBcera, as well as its presentation at a 2024 committee meeting held to approve a $150 million investment in the fund. Source: SBcera

Hunterbrook estimated there is a two-year average holding period for Lennar’s optioned land based on Angelo Gordon and Millrose’s contractual terms. Angelo Gordon gives Lennar a maximum of 40 months to complete takedown, according to the 2024 presentation Hunterbrook reviewed, indicating a midpoint of about 20 months, or 1.6 years after Angelo Gordon purchases the land and before Lennar purchases that land from Angelo Gordon. Millrose discloses the option period is six to 60 months, indicating a midpoint of 2.5 years, producing an estimated average holding period of roughly two years across option deals. Of note, this calculation assumes that Lennar is strictly following the takedown schedule and does not take into account any delays. Source: Millrose

The simplified calculation: We assumed that all of Lennar’s optioned land has a carry cost of 8.5%, the rate that Millrose charges Lennar. This is likely a conservative assumption; Millrose charges non-Lennar builders a higher rate of more than 9%; industry sources say the average carry cost of land banking can be around 11%, and multiple sources indicated 10% to 15%. Lennar disclosed last year that it holds $6.5 billion worth of optioned land representing roughly 111,000 homesites for Lennar. That’s about one-fifth of Lennar’s total number of homesites in land banks. Lennar had 496,250 homes in the banks, according to its 2025 10-K. Assuming the value of the homesite is the same across the banks, that would mean the value of Lennar’s total number of optioned homesites would amount to about $29 billion. Applying Millrose’s 8.5% option fee points to a total annualized run rate of about $2.46 billion.

Payment-in-kind (PIK) loans allow borrowers to pay interest in the form of additional debt, rather than cash. The additional debt is added to the principal balance until maturity. It’s honestly unclear whether Angelo Gordon’s loans to Lennar actually have a PIK-like structure — or whether Lennar pays monthly. This is our best guess based on the disclosures.

Angelo Gordon’s deal structure appears designed to protect the firm’s target return on capital — regardless of whether Lennar completes the takedowns or walks. The mechanism works on several levels: If Lennar completes the takedown, AG charges a premium on the land purchase price. But if Lennar stalls, the deal structure is set up to allow AG to still get their returns: It enforces a rigid schedule of fixed monthly takedowns over a maximum 40-month term; if Lennar falls behind, AG can terminate the contract and keep Lennar’s 20% deposit as “first loss” capital. On top of that, AG charges a termination fee. In short, AG collects its return whether Lennar takes down the lots on schedule, falls behind, or walks away entirely. Source: Angelo Gordon’s presentations to California county pension fund, SBcera

Lennar told investors its construction costs fell 10% over the FY2023 to FY2025 period during its 4Q 2025 earnings call. Hunterbrook estimates D.R. Horton’s construction fell 4% to 5%: DR Horton discloses stick-and-brick cost changes on a per-square-foot basis each quarter on their earnings calls, but does not provide a clean cumulative multi-year figure. Chaining their quarterly disclosures — down 3.5% year over year in the fiscal fourth quarter of 2023, roughly flat through FY2024, and down 1% year over year in the fiscal fourth quarter of 2025 — gives an approximate cumulative reduction of 4% to 5% over the same FY2023–FY2025 period.

Based on our two-year takedown assumption, this estimated option costs reflects the fees Lennar paid on the 2022 vintage of about 310,000 optioned homes — roughly 60% of Lennar’s current portfolio — that matured in 2025. Hunterbrook applied a uniform 8.5% on the total number of homesites from this vintage year.

Based on the midpoint of the holding term of roughly two years for the Angelo Gordon and Millrose’s contracts.

In 2025, Lennar disclosed their consolidated inventory not owned — an accounting line where companies have to park things they don’t technically own, like options, but are on the hook to buy — decreased by $2.4 billion, largely because it renegotiated option contracts that had previously forced the company to book the land as inventory; when an option contract leaves a builder with virtually no choice but to buy the land, accounting rules force the company to treat it as if it already owns it, according to Lennar’s own explanation. Source: Lennar FY2025 10K