The Myth of Hercules Capital

America’s most software-exposed major private credit firm is among the most richly valued. It also happens to be marking its software debt at 100 cents on the dollar—for now.

By: Matthew Termine, Sam Koppelman, Michelle Cera

Editor: Jim Impoco

Based on Hunterbrook Media’s reporting, Hunterbrook Capital is short $HTGC and long a basket of comparable securities at the time of publication. Positions may change at any time. See full disclosures on our website.

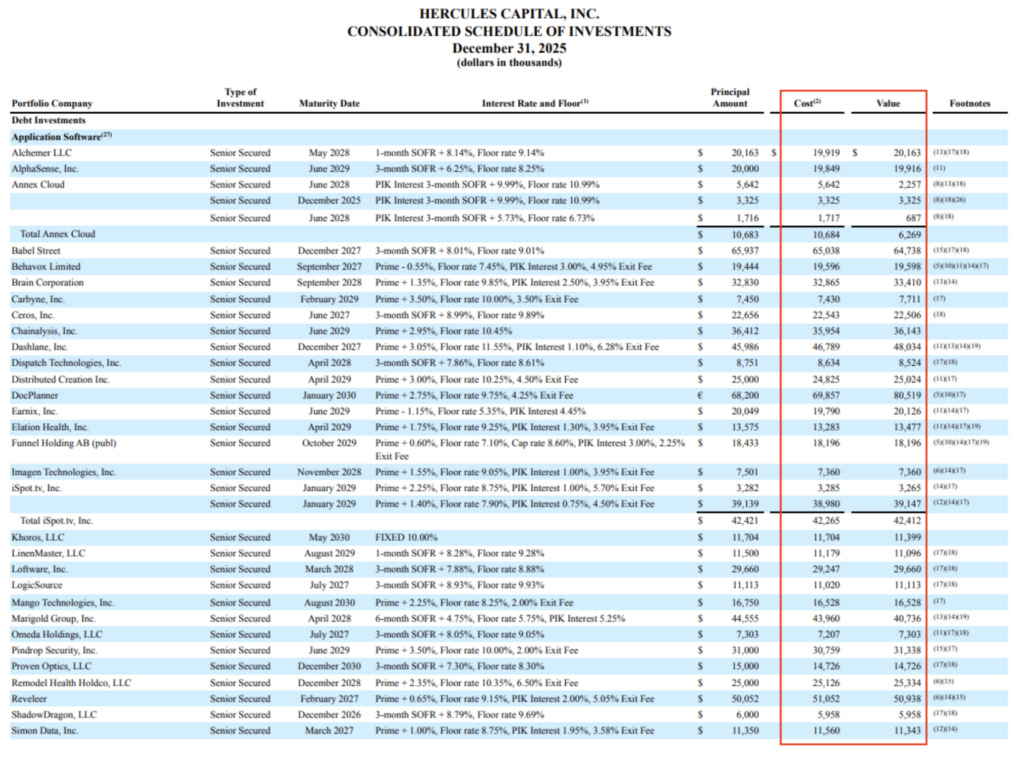

Hercules Capital ($HTGC) is among the most software-exposed business development companies (BDCs), yet it trades at some of the richest valuations. About 35% of the value of the company’s loan portfolio — roughly $1.5 billion — is in software debt, meaning that after accounting for leverage, 70 cents of every dollar of net asset value is backed by software. Despite billions worth of such debt across the industry falling into distressed territory, as of its most recent filings Hercules still marks its software book at100 cents on the dollar. And true software exposure may be higher than 35%. Hunterbrook Media found the firm categorizes companies like Houzz and AppDirect outside of software despite their products being explicitly software-based.

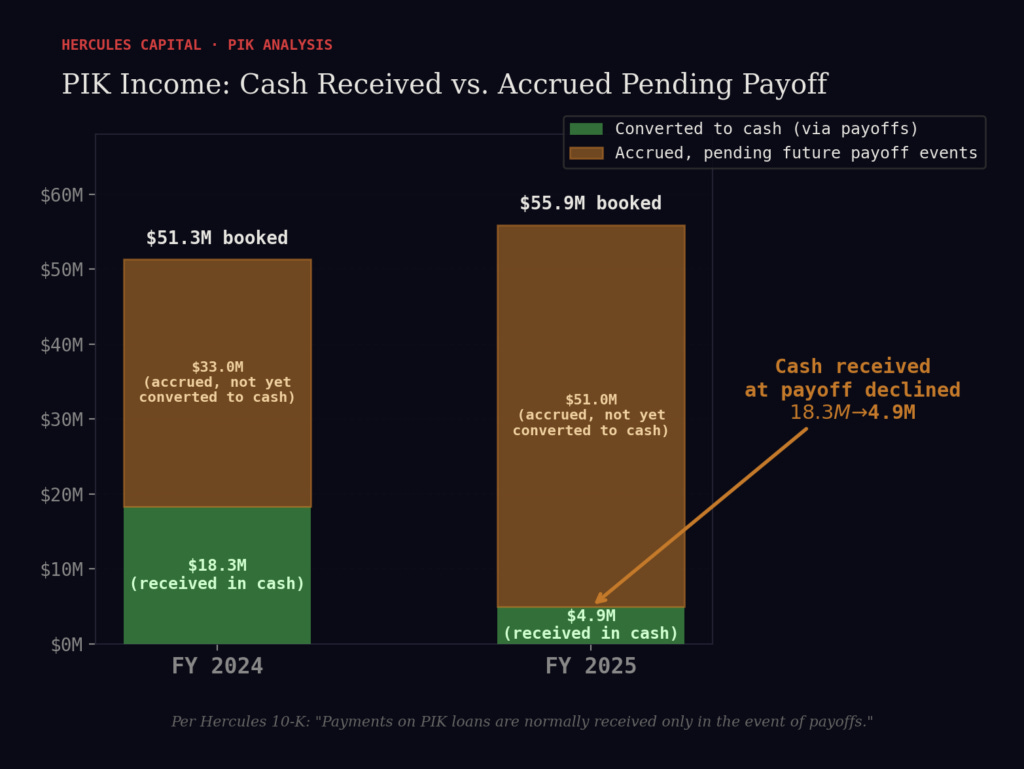

A growing share of income is phantom. Income from a type of debt called payment-in-kind (PIK) loans doubled in two years to $55.9 million in 2025, while the actual cash collected on PIK loans collapsed 73% year over year to just $4.9 million. PIK loans enable borrowers to “pay” interest by adding debt, but the lender does not actually receive interest payments along the way: The outstanding PIK receivable at Hercules has nearly tripled in recent years to $109.1 million — interest that has never been paid in cash by borrowers.

The dividend’s real cushion is thinner than it appears. Full-year NII of $1.91 per share covers the $1.60 base distribution at 119%, but Hercules also pays a $0.28 supplemental drawn from a finite reserve of past earnings. Including the supplemental, total distributions of $1.88 leave just three cents of margin. On a cash basis — stripping out PIK and other noncash items — Hercules’ own figures show the base distribution is covered at only 105.7%. If Hercules takes write-downs, even the base dividend may come under pressure.

Hercules runs a premium-dependent flywheel that could reverse catastrophically. Like Strategy (formerly MicroStrategy) with bitcoin, Hercules issues stock above NAV that funds accretive growth. The premium has already compressed from about 60% to about 25%. If it hits zero, equity issuance turns destructive, loan growth can stall, and the dividend may come under pressure — the same kind of doom loop that hit competitor TriplePoint ($TPVG).

The portfolio doesn’t cycle as fast as management claims. Despite describing 18-to-24-month turnover — assuaging fears surrounding the terminal value of its borrowers — Hunterbrook found that a significant share of funding events since 2022 went to existing borrower relationships, based on an analysis of 16 quarters of earnings-call disclosures, including some relationships that have lasted almost a decade. Hercules told Hunterbrook in an email that 63% of new fundings went to new portfolio companies.

A former Hercules finance team member described an overstretched valuations process. A team responsible for preparing valuations that fed directly into financial statements consisted of just four people in a single reporting line responsible for dozens of companies, they said, with few checks or cross-team review — a contrast to the multilayered processes the same employee now sees at another public company. Another former employee described an ad hoc deal sourcing process, in which Hercules would follow name-brand VCs into deals — a process the former employee likened to the swarm around Sam Bankman-Fried’s FTX.

The company’s headline credit metric may be an invention that flatters its track record. Hercules’ cumulative net realized loss rate of 3 basis points nets equity and warrant gains from IPO-era exits (DocuSign, Palantir, Pinterest) against loan losses. We couldn’t identify any other major BDCs using this methodology.

Hercules Capital provided Hunterbrook Media with a written response to questions. The company said that its portfolio valuations as of December 31, 2025, do not reflect 2026 volatility; that its PIK exposure is at the median of similarly sized BDCs; that its base dividend coverage is among the highest in the industry at 119%; that the majority of new fundings since 2022 went to new portfolio companies; that its valuations process is “rigorous and cross-functional” involving PwC audits, SOX compliance, and board oversight; and that its credit metric is required by GAAP. Hercules’ responses are incorporated throughout this article.

SaasPocalypse: Now

The software sector has lost an estimated trillion dollars in market value so far in 2026. It’s the largest, fastest destruction of software market cap in years. And private-credit firms — like Blue Owl Capital ($OWL) and Ares Management ($ARES) — have fallen with the borrowers of their managed funds.

“Private Credit Is Headed for a Software Shock,” read a Bloomberg headline on February 2. Three weeks later, the shock penetrated the public consciousness when Blue Owl — one of the largest private-credit managers in the world, with over $300 billion in assets under management — halted quarterly redemptions at one of its retail-focused business development corporations.

BDCs lend money to mid-sized and smaller companies, often companies that can’t easily access traditional bank financing. The BDC’s shares can be publicly traded, giving everyday investors access to private credit.

According to a Bloomberg index, $18 billion in broadly syndicated software loans have plunged into distressed territory — trading below 80 cents on the dollar — in a matter of weeks. UBS recently estimated private-credit default rates could soar to 15%. KKR’s BDC just cut its dividend earlier in the week.

But according to the books of lender Hercules Capital ($HTGC), everything is … totally fine?

The firm values its software loan portfolio, comprised of loans to smaller, often unprofitable startups, at more than 100 cents on the dollar — even in its 10-K released on February 12.

In a written response to Hunterbrook Media, Hercules stated that its figures are as of December 31, 2025, and “therefore do not reflect any potential pricing volatility that may have occurred in 2026.1”

Hercules describes itself as the largest nonbank venture lender in the United States. The firm has committed over $25 billion since launching in 2003. The founder, Manuel Henriquez, resigned as CEO in 2019 after being charged in the college admissions fraud Operation Varsity Blues.2 Hercules has been led since by Scott Bluestein, who also serves as its chief investment officer.

In total, Hercules has software debt valued at $1.5 billion on its books, according to its financial statements: roughly 35% of the value of its total loan portfolio. That means 70 cents on every dollar of its net asset value (NAV) is backed by a software loan — because Hercules, like other BDCs, uses leverage to fund its portfolio, in its case at roughly a 1:1 ratio.

According to JPMorgan’s recent assessment of the sector, this makes Hercules the most software-exposed lender of any meaningful size in America. And these numbers likely underestimate true exposure. Hunterbrook Media analyzed each loan Hercules disclosed in its most recent annual report and found that the firm assigns certain businesses that describe themselves as software companies to categories outside of software.

Take Houzz, which declares on its homepage that it offers, “Powerful software for construction and design.”

Another company that Hercules classifies as unrelated to software is AppDirect. That company describes itself as “the leading platform for selling, buying, and managing recurring technology services.” In other words: It’s a middleman for software companies, as the company lays out pretty clearly on its website.

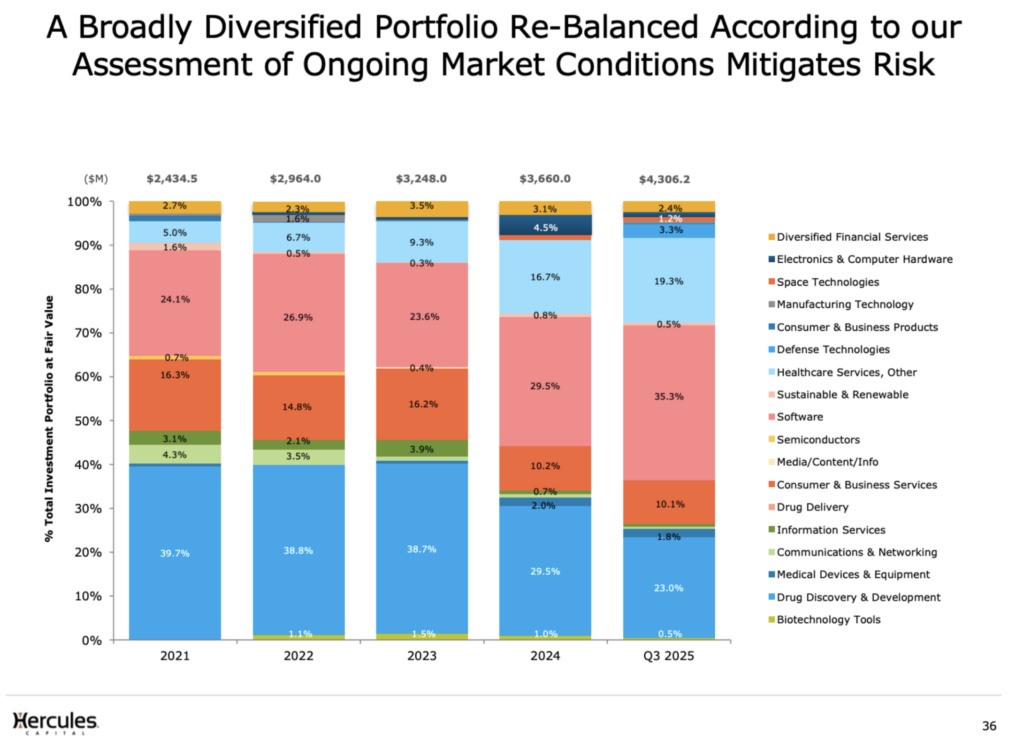

And Hercules has grown more exposed to software over time.

In the firm’s 3Q25 investor deck, on a slide about rebalancing risks based on market conditions, Hercules reveals it has gone from 24% software exposure to 35% software exposure — a nearly 50% increase — in just four years. Its next-largest category: Drug Discovery & Development.

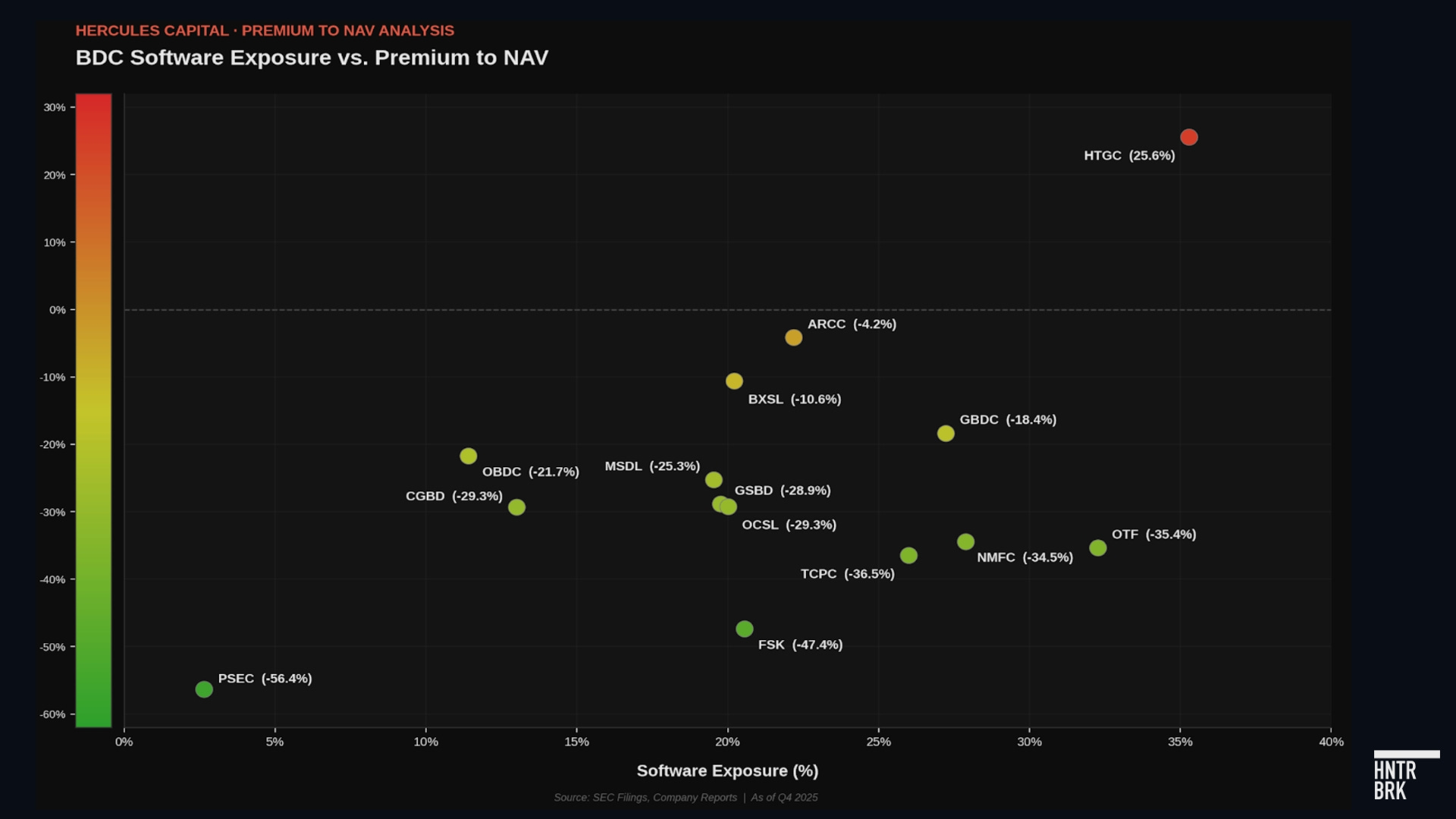

And yet Hercules trades at around a 25% premium to book value — the highest of any software-exposed BDC in the country depicted in a recent JPMorgan North American Credit Research report.

Charting premium and software exposure, Hercules sits alone in the upper-right corner: where substantial software concentration and a significant premium intersect.

A graph of premium to NAV (a proxy for valuation) relative to software exposure based on the JPM coverage universe. Note: BDCs JPM categorizes as having 0% software exposure — such as $MAIN — were excluded. Price per share data as of February 26, 2026.

Hunterbrook found every other BDC with more than 20% software concentration in its loan portfolio in the JPMorgan coverage universe trades at a discount to NAV or a far smaller premium. TriplePoint Venture Growth ($TPVG), a smaller venture lender, trades at an approximate 35% discount to NAV.

Why is one of the most exposed lenders the most expensive? And what happens if it loses its premium to NAV?

The Saylor Spiral

The inherent risk of the Hercules valuation is perhaps best explained by the Infinite Money Glitch of Michael Saylor’s Strategy (née MicroStrategy).

Here’s how it worked: Strategy traded at a massive premium to the value of its bitcoin holdings — at one point, investors were reportedly paying nearly $2.80 for every $1.00 of bitcoin on the balance sheet. That premium was the engine. Because the stock traded above the value of the underlying asset, every time Saylor issued new shares, he was effectively raising capital at a massive markup. He’d sell the expensive stock, buy more bitcoin, increase the bitcoin-per-share, and the stock would go up — which widened the premium — which let him issue more stock. Flywheel. Magic. Infinite money glitch.

Then bitcoin cracked. The premium vanished. By November 2025, Strategy fell below its net asset value. The stock, which peaked above $450, cratered 70% — the worst performer in the entire Nasdaq 100 in 2025. And here’s the doom loop: Once the premium disappears, the flywheel reverses. Issuing stock below NAV destroys value for existing shareholders. So you can’t issue stock as easily. So you can’t buy as much additional bitcoin. So the growth narrative dies. So the stock falls further. So the premium compresses more.

Hercules runs the same flywheel — just with software loans instead of bitcoin.

When Hercules trades at 1.25x NAV, every dollar of new equity it raises comes at a 25% premium to book value. That’s accretive to existing shareholders and provides cheap capital for new loans. Premium stock price → cheap equity → fund new loans → generate income → support dividend → maintain premium. Elegant.

Hercules noted to Hunterbrook that it has “conservatively raised less than $250 million of new public equity per year since FY22” and has also raised nearly $940 million in unsecured debt to fund growth since 2024. The company emphasized that as an internally managed BDC, “Hercules shareholders do not pay a management fee and Hercules management does not earn more by simply increasing Hercules’ asset base through the issuance of new shares.” Hercules said it primarily issues equity to maintain a conservative debt-to-equity ratio within regulatory limits and below levels required by its four investment-grade ratings. The company also pointed to the growth of Hercules Advisor-managed private funds as an additional source of capital for growth.

But as at Strategy, the flywheel spins in both directions.

If Hercules stock falls to NAV or below, the company can’t issue equity. And without equity issuance, Hercules can fund fewer new originations and extensions to existing portfolio companies, because BDCs are statutorily limited in how much leverage they can take on relative to the cash on their balance sheets.

This is the precise sequence that hit one of Hercules’ closest competitors. TriplePoint Venture Growth lost its premium and then cut its dividend. Hercules has maintained both its dividend and a premium to NAV — but the premium has narrowed from about 60% to about 25% in under a year.

If it hits zero, the Saylor spiral could begin.

The Marks Haven’t Caught Up

Hercules values its $1.5 billion software portfolio at around par — which is to say: The company doesn’t expect meaningful losses. But the borrowers behind those loans operate in a sector that has just experienced a systemic pullback.

And nobody knows what software companies will be worth when the debt comes due.

As JunkBondInvestor, a widely followed buy-side credit analyst, wrote this week: “What is a software company worth in five years? Not what it earns today or next quarter. Not what the sponsor paid for the business. What it’s actually worth when the AI labs are telling their investors they plan to replace Salesforce, Workday, and Adobe … Nobody can answer that question. Nobody.”

And the collateral underlying these loans — software code, brand equity, customer relationships — could ultimately be worth essentially nothing.

When Hercules’ software borrower Khoros hit a rough patch, Hercules was forced to write a $61 million loan down to $18 million. With software companies, generally, there is no factory to liquidate, no meaningful real estate to foreclose on. The collateral is code and customers. When the latter evaporates, the former can be rendered worthless.

Historically, the majority of Hercules’ portfolio companies have repaid their debt. But amid the sector decline, a borrower-by-borrower review of Hercules’ debt positions in 55 software firms as disclosed in Hercules’ most recent financials reveals a portfolio with pockets of pressure.

Sisense, a business intelligence platform, has cut its workforce in half, suffered a severe data breach, and doesn’t seem to have publicly raised external funding since early 2020.

Marigold Group’s debt is structured as a payment-in-kind (PIK) loan at a very high rate — Hercules collects zero cash interest — after the company already sold off its enterprise business.

Ceros, a no-code content platform, faces existential AI disruption. Similar names, like Wix and GoDaddy, have been killed in the public markets, each down more than 50% in the last year.

There are strong companies on the Hercules books as well.

Armis, the cybersecurity platform, is being acquired by ServiceNow for $7.75 billion in cash — a deal expected to close in the second half of 2026 that will almost certainly result in full loan repayment plus a meaningful return on the firm’s $2 million equity investment. Carbyne, a 911 emergency communications platform that Hercules helped fund, is being acquired by Axon for $625 million, with the deal expected to close in early 2026. AlphaSense, the AI-powered market intelligence platform, raised $650 million at a $4 billion valuation in 2024.

But the sourcing process for those deals was not exactly scientific, according to a former Hercules analyst who worked on deal sourcing.

“I got into the meeting with my manager and I was like, ”How do you do sourcing? Like, what’s the juice? Like, what’s your secret sauce?’ And he was like, ‘Go on the website for Google Ventures and just see what they invest in and just copy it. I don’t want anything else.’”

“That’s actually a really bad way to do your due diligence,” they added. “And that’s actually a way that a lot of these, you know, like, FTX and all these things, that’s how it happens because once these companies get one brand name on their investor list, right? Like Sequoia or something like that? Everybody else just freaking flocks to them.”

And once Hercules makes the loans, the valuation process itself may warrant scrutiny. A former member of Hercules’ finance team w described a small, overstretched team with few checks in place.

“There wasn’t a whole lot of fail-safes or backup checks,” they said. “We would have kind of one stream of resources and backups,” compared to other public companies where “there are multiple streams and cross-checking and cross-team development.”

According to this former employee, a team responsible for preparing certain valuations that fed directly into the financial statements consisted of four people arranged in a single reporting line — an analyst, a senior, a manager, and a director — handling an important subset of valuations for Hercules.

“I don’t think the team got the support that it needed,” they said. “It was a small team and it was stretched quite thin.”

Review was concentrated at the manager level. By the time work reached the director, the former employee recalled seeing few comments or corrections. The former employee, who now works in a similar role at another public company, described a starkly different environment.

“There is a strong push to do things the right way, to reinvent, to make sure that we’re double-checking, triple-checking.” Not so at Hercules.

Hercules told Hunterbrook that the valuations in its February filing are as of December 31, 2025, and don’t reflect volatility in the first quarter of 2026 — leaving open the possibility that the numbers will look different when it files for Q1. It also described its valuations process as “a rigorous and cross-functional exercise involving our deal teams responsible for portfolio origination and monitoring, credit team and finance team, who re-underwrite each position in the portfolio on a quarterly basis.”

The company noted it is subject to an integrated external audit by PwC, internal audit under SOX regulations, an annual SOX review, and has adopted Investment Company Act Rule 2a-5 for valuation governance. Hercules said its independent board of directors approves all fair value marks, and that the company uses two external valuation specialists each quarter to independently value a rotating portion of the portfolio, as “overseen by the Audit Committee.”

A Metric That May Mask the Truth

The secret sauce of Hercules’ investor pitch is an interesting statistic: a cumulative net realized loss rate of only 3 basis points across $21.6 billion in total commitments since inception.

Hunterbrook reporting suggests this metric may be an invention unique to Hercules. It nets equity and warrant gains — windfalls from IPO-era exits like DocuSign, Palantir, and Pinterest — against loan losses. It is as if a bank reported its mortgage default rate after subtracting gains from its stock portfolio. We couldn’t identify any other major BDCs using this methodology.

Ares Capital — the BDC affiliate of Ares Management, which holds a portfolio almost seven times the size of Hercules — reports its equity gains as a separate line item and leads with standard credit metrics like nonaccrual rates and interest coverage ratios.

Strip out the warrant gains and the picture changes meaningfully.

The company’s cumulative net realized loss position was negative $134.7 million through 3Q25.

And the safety net that made the metric work is nearly gone.

The warrant and equity portfolio has shrunk from 11% of total assets in 2020 to about 4% today. Going forward, debt losses hit the bottom line with virtually no equity gains to soften the blow.

The former member of the finance team called the practice of using this metric “quite odd.”

“I don’t think that they should be netting that against their equity and warrants,” they said, adding that as a public company, Hercules should be able to articulate “a good rationale as to why they are doing that” if it diverges from how peers in the industry handle the same reporting.

Hercules said it is required by the Investment Company Act of 1940 and GAAP to report net realized gains and losses on investments including equity and warrants, and that “excluding these equity gains and losses from the calculation would not be in compliance with GAAP.” The firm said it has used consistent methodology under independent accounting oversight for more than 21 years.

A Growing Share of Income Is Phantom

Then there’s the rising tide of “phantom income.”

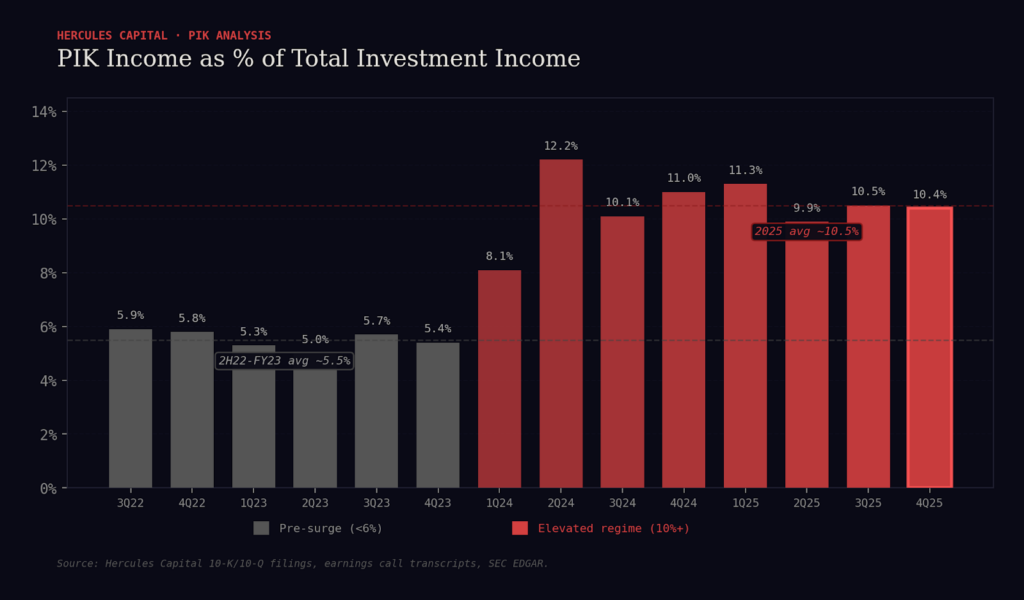

In 2025, Hercules booked $55.9 million in payment-in-kind interest income. It collected $4.9 million in cash — an amount equal to roughly 9% of the PIK income booked during the year, compared to 36% the year before.

Payment-in-kind interest, or PIK, is a mechanism that allows borrowers to defer cash interest payments by capitalizing the interest owed onto the loan’s principal balance. The lender records it as income. But the cash may never arrive. For a venture lender concentrated in software, rising PIK is a credit canary: When borrowers stop paying in cash, it often means they can’t.

Hercules’ PIK income has more than doubled in two years, from roughly $24.7 million in 2023 to $55.9 million in 2025. It now accounts for 11% of total interest and dividend income, up from approximately 5.7% just two years ago.

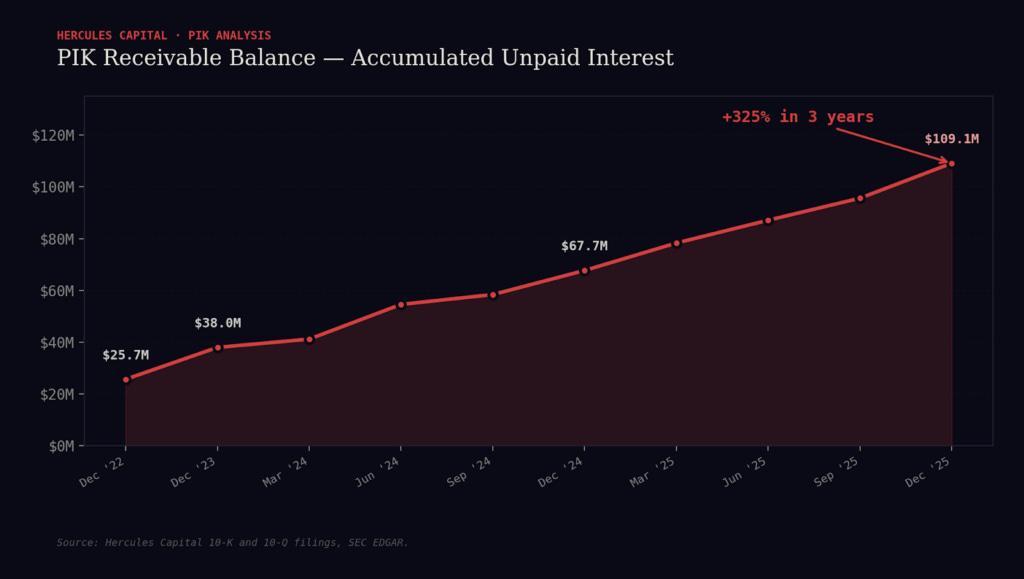

More important than the annual run rate is what’s piling up on the balance sheet: The outstanding PIK receivable — accumulated interest sitting on Hercules’ books — reached $109.1 million as of Dec. 31, 2025. That’s nearly triple the $38 million balance at the end of 2023.

And the 10-K’s own rollforward table reveals a telling detail: Hercules collected just $4.9 million in actual cash payments on PIK loans during 2025, a 73% collapse from the $18.3 million collected in 2024.

In the firm’s disclosure, “Payments on PIK loans are normally received only in the event of payoffs.”

Translation: This cash comes in only when a borrower gets acquired, IPOs, or refinances — events that are scarce in a venture downturn. Until then, the receivable just keeps growing.

This means Hercules is now owed more than $109 million in deferred interest payments subject to the same credit risk of the underlying loans, and the rate at which it’s actually collecting that cash has cratered. This phantom income inflates dividend coverage ratios used to justify the valuation.

Management attempted to contextualize the PIK exposure on a recent earnings call, noting that approximately 86% of Q4 PIK income was attributable to original deal underwriting rather than credit-related amendments, and that 91% came from loans rated highly on the company’s internal scale.

In its written response to Hunterbrook, Hercules said its PIK exposure relative to revenue was “approximately the median of similarly-sized BDCs and is below several of our direct competitors.” The company attributed approximately 86% of its 4Q25 PIK income to PIK that was “part of the original underwriting and not a result of any credit or performance-related amendment,” adding that nearly 91% of PIK income in the quarter came from loans it had rated as less risky. Hercules said lower cash collections on PIK loans in 2025 versus 2024 reflected “a higher volume of prepayments of loans with a PIK component in 2024 versus 2025,” noting that PIK payments are collected at contractual maturity or upon prepayment.

In its 10-K, Hercules noted that PIK receivable represented approximately 3% of total debt investments as of year-end, up from 2% a year earlier.

But this framing obscures the core issue: Regardless of whether PIK was baked into the original deal or added later, or whether 2024 saw higher prepayments than 2025, it remains noncash income owed by cash-burning borrowers. The fact that PIK was part of the original underwriting simply means Hercules is intentionally structuring more loans with deferred cash payments — which is itself a competitive concession that increases credit risk.

The Portfolio Can’t Cycle Out as Fast as Hercules Claims

When asked about software concentration risk, management often points to turnover — the idea that the portfolio cycles quickly enough that exposures can simply be rotated out. CEO Scott Bluestein has even described the portfolio as turning about every 18-to-24 months.

The implication: If software goes bad, Hercules can simply cycle out.

But that framing appears to count loan amendments and extensions as completed cycles and obscures the fact that most borrower relationships last far longer than 18 months.

A quarter-by-quarter read of Hercules’ own earnings-call disclosures shows why the distinction matters. On call after call, Hercules shares that the majority of its new fundings were to existing borrowers.

Hercules disputed these figures in aggregate, stating that “since 2022, 63% of all new fundings have been to new portfolio companies” according to its public financial statements.

Since 2022, the company has repeatedly told investors how many companies it funded in the quarter and how many of those were new borrower relationships. Across the last 16 quarters (1Q22 through 4Q25), we estimate Hercules funded 408 companies — but only 147 of them (about 36%) were new relationships. In 14 of those 16 quarters, new relationships were the minority of deals, meaning most capital deployment went to companies already in their portfolio.

The pattern tracks the cycle. In 2023, as venture funding tightened, only 30 out of 105 funded-company events (29%) were new relationships — and in 4Q23, just five out of 27 (19%) were new. In 2024, the skew persisted (3Q24: four new relationships out of 21 fundings). Even in 2025, when originations re-accelerated, three of the four quarters still had a majority of fundings going to existing borrowers (e.g., 3Q25: 24 funded companies, only seven new; 4Q25: 33 funded, only 12 new).

In other words, the capital deployment that investors see in quarterly disclosures is largely repeat lending inside the same borrower set, not a steady refresh.

The result is a credit ecosystem where “no default” may be able to coexist with slow-motion impairment. Maturities get pushed and cash interest is replaced with PIK payments — all while relationship concentration persists because the same borrower names keep receiving incremental capital.

This pattern — where borrowers who would have repaid instead amend, extend, and pile on PIK — is playing out across the software credit universe, not just at Hercules.

“The concentration of software loans maturing in 2026-2027, the largest sector cohort in the near-term maturity bracket, is overwhelmingly going to get resolved through amend-and-extend transactions, not through bankruptcy filings,” wrote JunkBondInvestor. “When a borrower can’t refinance at par but isn’t in operational distress, the playbook is familiar: the sponsor and the existing lender group negotiate an extension. Lenders get a fee, a spread bump, maybe some incremental covenant protection. The company gets two or three more years of runway. No default. No restructuring. Everyone claims victory.”

“But this has implications for loan investors that aren’t being processed,” he explains. “And here’s the part that should keep loan investors up at night: the amend-and-extend process is where creditors get coerced, and in this market, they will be. Sponsors know that a fragmented lender base facing a maturity wall has limited options. You can either extend on the sponsor’s terms, which often means PIK toggles, covenant stripping, and priming risk from new money tranches, or you can watch the loan trade down as the maturity approaches without a resolution. Each extension that adds PIK, strips covenants, or pushes maturities without meaningful deleveraging is a slow-motion impairment that never shows up in the default statistics. The risk isn’t default but extension at terms that are incrementally worse for lenders while the [terminal value] question remains unresolved.”

The Dividend Is Thinner Than It Looks

Hercules frames its payout as conservative. In 4Q25, the company reported net investment income (NII) of $0.48 per share, which it says provided 120% coverage of the base distribution of $0.40. That sounds like a healthy cushion — until you look at what shareholders actually receive.

The total cash distribution for Q4 was $0.47 per share: the $0.40 base plus a $0.07 supplemental. Against $0.48 of NII, that’s roughly 102% coverage — a cushion of a penny. For the full year, the math is equally tight: $1.91 of NII per share against $1.88 in distributions paid. Three cents of breathing room for the entire year. That’s tight.

Hercules disagreed with this perspective in a written response to Hunterbrook Media, calling it “incorrect” to measure dividend coverage against the combined distribution. The company noted that the supplemental distribution is paid from its undistributed earnings spillover of $149.9 million ($0.82 per share as of December 31, 2025 — not from NII). Even excluding all PIK and additional noncash transactions, Hercules said cash NII covered the base distribution at 105.7%. The company added that it “maintains near the high end of base dividend coverage across the entire BDC universe.”

Hercules provided the following figures:

Hercules’ distinction between the base and supplemental distribution is technically correct: The supplemental is paid from a spillover account, not directly from current-quarter NII. To maintain its status as a regulated investment company (RIC), Hercules, like every BDC, must distribute at least 90% of its taxable income to shareholders annually. The IRS allows RICs to maintain an undistributed earnings spillover — a reserve of prior taxable income not yet distributed — from which supplemental payments are drawn.

But this framing, while accurate as a matter of accounting, does not change the economic reality facing shareholders. The total cash leaving the building each quarter is $0.47 per share. The total NII coming in is $0.48. A penny of coverage. The distinction between “base” and “supplemental” is a labeling exercise: Shareholders receiving $1.88 per year in distributions are relying on a combination of current earnings and a finite savings account.

And the savings account, while substantial at $149.9 million ($0.82 per share), is not self-replenishing. If NII declines — whether from falling rates, rising defaults, or slowing deployment — the spillover gets drawn down rather than built up. At the current supplemental rate of $0.28 per year, the reserve covers roughly three years of supplemental payments before it is depleted, assuming no further accumulation.

More importantly, a meaningful slice of the $1.91 in NII is phantom. With PIK accounting for approximately 11% of investment income, the dividend is being supported in part by interest that has never been paid in cash. Even by Hercules’ own figures, cash NII (excluding PIK and other non-cash items) covers the base distribution at 105.7% — a tighter cushion than the headline 119% suggests, and one that leaves virtually no room for credit deterioration before the base distribution itself comes under pressure.

Hercules’ cash balance allows management to keep mailing extra checks even when quarter-to-quarter coverage is razor-thin. But it is not evidence that the portfolio’s current earnings power is expanding. It’s a savings account.

Then there’s dilution. Hercules has been steadily increasing its share count through its at-the-market equity program, selling stock at a premium to NAV and using the proceeds to, among other activities, fund new loans. In 4Q25, the company’s basic weighted-average shares were 180.8 million, up from 165.1 million in 4Q24. Shares outstanding rose to 182.7 million on December 31, 2025, from 170.6 million a year earlier.

That dilution shows up directly in per-share earnings: The full-year 2025 NII per share of $1.91 is lower than 2024’s $2.00 — even though the total NII dollars increased. The company acknowledges that NAV per share benefited from at-the-market issuance above book value, a tailwind that exists only as long as the stock trades at a premium. If the premium disappears, the accretive math flips to destructive. Hercules ended the year with 18.8 million shares still available under the program, having sold stock in 4Q25 and again in January 2026.

The result is a wobbly architecture: a dividend with a penny of coverage, inflated by noncash income, and sustained by drawing down a legacy savings account — all while ongoing share issuance dilutes a story that only works as long as the market pays a premium.

The Competitive Moat That Isn’t

The competitive landscape reinforces the problem. When asked what differentiates Hercules, CEO Bluestein said in a 2025 earnings call, “We have the best team in the business. The team is incredibly experienced. The team has been together for a long time. The team knows how to pick the right companies.”

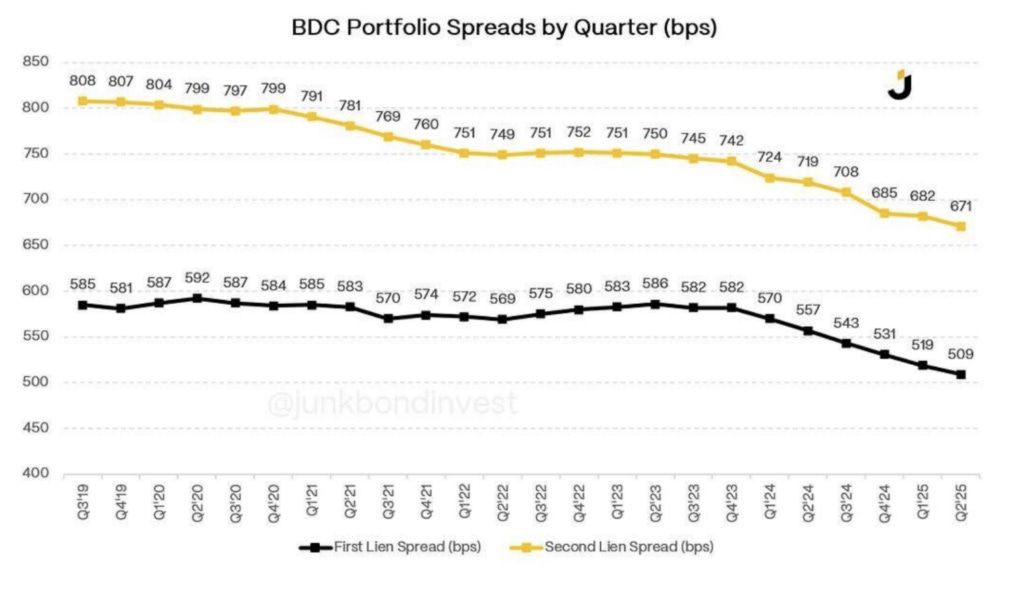

That may be true. But “we have good people” is a convenient claim for a lender to make when they have no structural moat in a largely commoditized sector. The venture lending market has swollen from a handful of specialists to dozens of publicly-traded BDCs, and SVB — reborn under First Citizens Bank — still commands roughly a third of the venture banking market. Spreads across the sector have fallen significantly, quarter after quarter, for two years running.

If Hercules were truly cornering the market on the best risk-adjusted loans, you’d think competing capital might be swarming those same deals. If it’s winning deals because other lenders don’t want them — extending credit to software companies at terms that more conservative shops walk away from — then the portfolio suffers from adverse selection.

And beyond the competitive dynamics, the former finance team member described a culture with significant “time pressure,” where decisions can end up feeling rushed under tight deadlines. They also noted a “very big culture of wealth and opulence and power and ego and status,” a description that aligns with the Hercules founder’s role in the college admissions scam.

But the story of Hercules is less about culture than it is about the numbers.

Return to the Infinite Money Glitch. When Hercules trades above book value, every dollar of new equity is accretive — cheap capital that funds new loans, generates income, supports the dividend, and sustains the premium. Strategy ran the same machine with bitcoin. TriplePoint ran it with venture loans. In each case, the cycle was elegant on the way up and devastating on the way down. When the premium vanished, equity issuance turned destructive, loan growth stalled, and the dividend followed.

Hercules has long been the exception to the rule — but the exception is narrowing. The premium has been cut in half in a matter of months. The software sector that backs 70 cents of every dollar of NAV is in its worst downturn in years. The income is increasingly phantom. The full dividend cushion is a rounding error. The warrant portfolio that once absorbed losses has shrunk to a fraction of what it was. And the markets still have not meaningfully moved — at least not yet.

Authors

Matthew Termine is a lawyer with nearly five years of experience leading the legal team at a mortgage technology company. In 2017, Matt was credited by the Wall Street Journal, among others, for identifying suspicious mortgage loan transactions that led to several successful criminal prosecutions, including that of a prominent political operative and the chief executive officer of a federally chartered bank. He is a graduate of Trinity College and Fordham University School of Law.

Michelle Cera trained as a sociologist specializing in digital ethnography and pedagogy. She completed her PhD in Sociology at New York University, building on her Bachelor of Arts degree with Highest Honors from the University of California, Berkeley. She has also served as a Workshop Coordinator at NYU’s Anthropology and Sociology Departments, fostering interdisciplinary collaboration and innovative research methodologies.

Sam is a New York Times best-selling author who has written books with former United States Attorney General Eric Holder and former United States Acting Solicitor General Neal Katyal. Sam has published in the New York Times, Washington Post, Boston Globe, Time Magazine, and other outlets — and occasionally volunteers on a fire speech for a good cause. He has a BA in Government from Harvard, where he was named a John Harvard Scholar and wrote op-eds like “Shut Down Harvard Football,” which he tells us were great for his social life.

Editor

Jim Impoco is the award-winning former editor-in-chief of Newsweek who returned the publication to print in 2014. Before that, he was executive editor at Thomson Reuters Digital, Sunday Business Editor at The New York Times, and Assistant Managing Editor at Fortune. Jim, who started his journalism career as a Tokyo-based reporter for The Associated Press and U.S. News & World Report, has a Master’s in Chinese and Japanese History from the University of California at Berkeley.

Graphic

Dan DeLorenzo is a creative director with 25 years reporting news through visuals. Since first joining a newsroom graphics department in 2001, he has built teams at Bloomberg News, Bridgewater Associates, and the United Nations, and published groundbreaking visual journalism at The Wall Street Journal, Associated Press, The New York Times, and Business Insider. A passion for the craft has landed him at the helm of newsroom teams, on the ground in humanitarian emergencies, and at the epicenter of the world’s largest hedge fund. He runs DGFX Studio, a creative agency serving top organizations in media, finance, and civil society with data visualization, cartography, and strategic visual intelligence. He moonlights as a professional sailor working toward a USCG captain’s license and is a certified Pilates instructor.

LEGAL DISCLAIMER

© 2026 by Hunterbrook Media LLC. When using this website, you acknowledge and accept that such usage is solely at your own discretion and risk. Hunterbrook Media LLC, along with any associated entities, shall not be held responsible for any direct or indirect damages resulting from the use of information provided in any Hunterbrook publications. It is crucial for you to conduct your own research and seek advice from qualified financial, legal, and tax professionals before making any investment decisions based on information obtained from Hunterbrook Media LLC. The content provided by Hunterbrook Media LLC does not constitute an offer to sell, nor a solicitation of an offer to purchase any securities. Furthermore, no securities shall be offered or sold in any jurisdiction where such activities would be contrary to the local securities laws.

Hunterbrook Media LLC is not a registered investment advisor in the United States or any other jurisdiction. We strive to ensure the accuracy and reliability of the information provided, drawing on sources believed to be trustworthy. Nevertheless, this information is provided “as is” without any guarantee of accuracy, timeliness, completeness, or usefulness for any particular purpose. Hunterbrook Media LLC does not guarantee the results obtained from the use of this information. All information presented are opinions based on our analyses and are subject to change without notice, and there is no commitment from Hunterbrook Media LLC to revise or update any information or opinions contained in any report or publication contained on this website. The above content, including all information and opinions presented, is intended solely for educational and information purposes only. Hunterbrook Media LLC authorizes the redistribution of these materials, in whole or in part, provided that such redistribution is for non-commercial, informational purposes only. Redistribution must include this notice and must not alter the materials. Any commercial use, alteration, or other forms of misuse of these materials are strictly prohibited without the express written approval of Hunterbrook Media LLC. Unauthorized use, alteration, or misuse of these materials may result in legal action to enforce our rights, including but not limited to seeking injunctive relief, damages, and any other remedies available under the law.

The company went on to note that consistent with ASC 820, because approximately 75% of its prime-based loans are at their contractual rate floor, "the fair value on those loans will be generally adjusted upward in a declining rate environment." Hercules also pointed to a weighted average loan-to-value (LTV) of approximately 14% across its debt portfolio and said that 100% of its debt investments on accrual were current as of the release of 4Q25 results. The company said it underwrites the software sector "very conservatively with ARR attachment points less than 1x on average" and that its average historical loan duration is less than 24 months.

Henriquez pleaded guilty to conspiracy to commit wire fraud and money laundering after paying more than $400,000 to rig his daughters’ entrance exams and bribe a Georgetown tennis coach. He was sentenced to six months in prison and received a severance package exceeding $10 million on his way out the door.